સુરત: ભારતની હીરા અને ટેક્સટાઇલ રાજધાની FMCG સોનાની ખાણને મળે છે

સુરત માત્ર ગુજરાતનું બીજું શહેર નથી — તે ભારતનું સૌથી ઝડપથી વિકસતું ટિયર-2 મેટ્રો છે અને દલીલપૂર્વક દેશનું સૌથી ઓછું આંકવામાં આવેલું FMCG બજાર છે. 70 લાખથી વધુ મેટ્રોપોલિટન વસ્તી, ટિયર-2 શહેરોમાં સૌથી વધુ માથાદીઠ ડિસ્પોઝેબલ આવક અને વિશ્વના સૌથી કેન્દ્રિત બે ઉદ્યોગ ક્લસ્ટરો — હીરા અને ટેક્સટાઇલ — દ્વારા આકાર પામેલા ગ્રાહક આધાર સાથે, સુરત એક વિતરણ તક રજૂ કરે છે જેને થોડી જ બ્રાન્ડ્સ સંપૂર્ણપણે મૂડીકૃત કરી શકી છે.

શહેર વિશ્વના 90% થી વધુ હીરાની પ્રક્રિયા કરે છે અને ભારતના કૃત્રિમ ટેક્સટાઇલ ઉત્પાદનનો લગભગ 40% હિસ્સો ધરાવે છે. આ ઉદ્યોગોએ એક અનન્ય સમૃદ્ધ કામદાર વર્ગ, સ્થળાંતરિત ઉદ્યોગસાહસિક નેટવર્ક અને વપરાશ પેટર્ન બનાવ્યા છે જે પુણે, જયપુર અથવા લખનઊ જેવા સમકક્ષ શહેરોથી તીવ્રપણે અલગ છે. FMCG બ્રાન્ડ્સ અને વિતરકો માટે, સુરતના ઔદ્યોગિક DNA ને સમજવું વૈકલ્પિક નથી — તે કોઈપણ અર્થપૂર્ણ વિતરણ વ્યૂહરચના માટેનો પ્રારંભ બિંદુ છે.

છતાં મોટાભાગની રાષ્ટ્રીય FMCG બ્રાન્ડ્સ હજુ પણ સુરતને તેમની ગુજરાત કામગીરીમાં ગૌણ ચોકી તરીકે ગણે છે, જે અમદાવાદથી ન્યૂનતમ સ્થાનિક કસ્ટમાઇઝેશન સાથે સંચાલિત થાય છે. પ્રગતિશીલ વિતરકો જે હેતુ-નિર્મિત FMCG વિતરણ સોફ્ટવેર અને સુરત-વિશિષ્ટ અમલીકરણમાં રોકાણ કરે છે તેઓ અપ્રમાણસર બજાર હિસ્સો કબજે કરી રહ્યા છે જ્યારે સ્પર્ધકો જેનરિક પ્લેબુક્સ ચલાવે છે.

સુરત બજાર સ્નેપશોટ (2026)

| મેટ્રિક | સુરત | ગુજરાત |

|---|---|---|

| મેટ્રો વસ્તી (2026 અંદાજ) | 70 લાખ+ | 7.5 કરોડ |

| FMCG બજાર કદ | Rs 14,000-16,000 કરોડ | Rs 85,000 કરોડ |

| સક્રિય FMCG વિતરકો | 1,800+ | 22,000+ |

| રિટેલ આઉટલેટ્સ | 85,000+ | 9.5 લાખ |

| મોડર્ન ટ્રેડ હિસ્સો | 18-20% | 14% |

| વાર્ષિક FMCG વૃદ્ધિ દર | 14-16% | 10% |

| માથાદીઠ FMCG ખર્ચ (ટિયર-2 રેન્ક) | #1 રાષ્ટ્રીય સ્તરે | - |

| મુખ્ય ઔદ્યોગિક ક્લસ્ટરો | હીરા (વરાછા), ટેક્સટાઇલ (રિંગ રોડ), IT (ડુમાસ રોડ) | - |

શા માટે સુરત ભારતનું સૌથી ઓછું આંકવામાં આવેલું FMCG બજાર છે

1. હીરા અને ટેક્સટાઇલ સંપત્તિ અનન્ય ખર્ચ શક્તિ બનાવે છે

સુરતનો હીરા પોલિશિંગ ઉદ્યોગ સીધી રીતે 8 લાખથી વધુ કામદારોને રોજગાર આપે છે, જેમની સરેરાશ માસિક આવક Rs 25,000-60,000 છે — જે ભારતમાં અન્યત્ર સમકક્ષ અર્ધ-કુશળ કામદારો કરતાં નોંધપાત્ર રીતે વધારે છે. ટેક્સટાઇલ ઉદ્યોગ પાવર લૂમ, પ્રોસેસિંગ યુનિટ્સ અને ટ્રેડિંગ હાઉસમાં અન્ય 12-15 લાખ કામદારો ઉમેરે છે. આ કેન્દ્રિત ઔદ્યોગિક સંપત્તિ FMCG ખર્ચ પેટર્નમાં અનુવાદ કરે છે જે ટિયર-2 શહેરો કરતાં મેટ્રો જેવા હોય છે: પ્રીમિયમ વ્યક્તિગત સંભાળ ઉત્પાદનો, બ્રાન્ડેડ પેકેજ્ડ ફૂડ્સ, હેલ્થ બેવરેજિસ અને આયાતી સ્નેક્સ એવા દરે વેચાય છે જે પ્રથમ વખત બજારમાં પ્રવેશતી બ્રાન્ડ્સને આશ્ચર્યચકિત કરે છે.

વિતરકો જે સેલ્સ એનાલિટિક્સ ને વિસ્તાર પ્રકાર પ્રમાણે વિભાજિત કરે છે — હીરા કામદાર પડોશ વિ ટેક્સટાઇલ માર્કેટ વિસ્તારો વિ રહેણાંક ઝોન — સતત શોધે છે કે હીરા-પટ્ટાના આઉટલેટ્સ અન્ય ટિયર-2 શહેરોમાં સમકક્ષ આઉટલેટ્સ કરતાં પ્રીમિયમ SKU વેચાણ 2-3 ગણું ઉત્પન્ન કરે છે.

2. સ્થળાંતરિત કાર્યબળ વર્ષભર માંગ ચલાવે છે

મોસમી બજારોથી વિપરીત, સુરતના ઉદ્યોગો વર્ષભર કાર્યરત રહે છે, જે મુખ્યત્વે સૌરાષ્ટ્ર, કાઠિયાવાડ, રાજસ્થાન, ઉત્તર પ્રદેશ, બિહાર અને ઓડિશાના વિશાળ સ્થળાંતરિત કાર્યબળને ટકાવી રાખે છે. આ એક અનન્ય FMCG માંગ પ્રોફાઇલ બનાવે છે: એક જ શહેરમાં મલ્ટિ-પ્રાદેશિક સ્વાદ પસંદગીઓ. સરસવનું તેલ, નારિયેળનું તેલ, મગફળીનું તેલ અને રિફાઇન્ડ તેલ બધાં નોંધપાત્ર જથ્થામાં વેચાય છે — એક સાથે. પ્રાદેશિક સ્નેક બ્રાન્ડ્સ, ચોક્કસ મસાલા મિશ્રણો અને રાજ્ય-વિશિષ્ટ વ્યક્તિગત સંભાળ ઉત્પાદનો જે અન્યત્ર નિચે હોત તે સુરતમાં અર્થપૂર્ણ જથ્થા પ્રાપ્ત કરે છે.

વિતરકો માટે, આ SKU વિવિધતાનું સંચાલન કરવા માટે મજબૂત ઓર્ડર મેનેજમેન્ટ અને ઇન્વેન્ટરી સિસ્ટમ્સ ની જરૂર છે જે સ્ટોકઆઉટ અથવા ઓવરસ્ટોક અરાજકતા વગર 2,000-4,000 સક્રિય SKU સંભાળી શકે.

3. ટિયર-2 શહેરોમાં સૌથી વધુ ડિસ્પોઝેબલ આવક

બહુવિધ ઉદ્યોગ સર્વેક્ષણો અને RBI ડેટા સતત જીવનનિર્વાહના ખર્ચ માટે ગોઠવાયા પછી માથાદીઠ ડિસ્પોઝેબલ આવક માટે સુરતને ટોચના 3 ભારતીય શહેરોમાં સ્થાન આપે છે. હાઉસિંગ ખર્ચ મુંબઈ અથવા પુણે કરતાં 40-60% ઓછા રહે છે, છતાં હીરા અને ટેક્સટાઇલ ક્ષેત્રોમાં આવક તે શહેરો સાથે સ્પર્ધા કરે છે. પરિણામ: સુરતના ગ્રાહકો FMCG, બહાર ખાવા, વ્યક્તિગત સંભાળ અને ઘરગથ્થુ ઉત્પાદનો પર ઉદારતાથી ખર્ચ કરે છે. પ્રીમિયમ FMCG શ્રેણીઓ અહીં વાર્ષિક 18-22% ના દરે વધે છે, જે રાષ્ટ્રીય સ્તરે 10-12% ની તુલનામાં છે.

4. ઝડપી શહેરીકરણ અને નવી ટાઉનશિપ વિકાસ

સુરતની મ્યુનિસિપલ સીમાઓ નોંધપાત્ર રીતે વિસ્તરી છે, અને વેસુ, પાલ, અલથાણ, ડિંડોલી અને સુરત-ડુમાસ કોરિડોર સાથેની નવી રહેણાંક ટાઉનશિપ વાર્ષિક લાખો ગ્રાહકો ઉમેરી રહી છે. દરેક નવી ટાઉનશિપ ગ્રીનફિલ્ડ વિતરણ તકને રજૂ કરે છે જ્યાં પ્રથમ ગતિ કરનારાઓ લાંબા સમય સુધી બજાર હિસ્સો કબજે કરે છે. ડિસ્ટ્રિબ્યુશન ટ્રેકિંગ ધરાવતા વિતરકો સ્પર્ધકો પહેલા ઓછી સેવા આપતા ઝોન ઓળખી શકે છે અને લક્ષિત કવરેજ તૈનાત કરી શકે છે.

સુરતના મુખ્ય વિતરણ ઝોન

વરાછા: હીરા પટ્ટો

વરાછા સુરતનું હૃદય અને ભારતની હીરા પોલિશિંગ રાજધાની છે. 5,000 થી વધુ હીરા પોલિશિંગ યુનિટ્સ 10 કિમીની ત્રિજ્યામાં કાર્યરત છે, જે ગાઢ રહેણાંક અને વ્યવસાયિક ઇકોસિસ્ટમને ટેકો આપે છે. મુખ્ય વિતરણ લાક્ષણિકતાઓ:

- વસ્તી ઘનતા: ગુજરાતમાં સૌથી વધુ — મુખ્ય વિસ્તારોમાં પ્રતિ ચોરસ કિમી 40,000 થી વધુ

- આઉટલેટ ઘનતા: પ્રતિ ચોરસ કિમી 120-150 રિટેલ આઉટલેટ્સ, મુખ્યત્વે કિરાણા

- ગ્રાહક પ્રોફાઇલ: હીરા કામદારો (Rs 25,000-60,000/મહિને), કાઠિયાવાડી અને સૌરાષ્ટ્રના સ્થળાંતરિતો

- FMCG પસંદગીઓ: પ્રીમિયમ ખાદ્ય તેલ, બ્રાન્ડેડ સ્નેક્સ, વ્યક્તિગત સંભાળ, હેલ્થ ડ્રિંક્સ

- વિતરણ પડકાર: સાંકડી ગલીઓ, ઉચ્ચ ભીડ, રોકડ-આધારિત અર્થતંત્ર

- તક: પ્રીમિયમ SKU અપનાવવાનો દર શહેરની સરેરાશ કરતાં 30-40% વધારે

વરાછા આવરી લેતા વિતરકોને રૂટ ઓપ્ટિમાઇઝેશન ની જરૂર છે જે પ્રતિ બીટ 60-80 આઉટલેટ્સ સાથે ઉચ્ચ-ઘનતા, સાંકડી-ગલીની ડિલિવરી સંભાળે છે. રોકડ-આધારિત હીરા અર્થતંત્રનો અર્થ એ છે કે ચુકવણી સંગ્રહ શિસ્ત નિર્ણાયક છે — ડિજિટલ ચુકવણી ટ્રેકિંગ સંગ્રહ અંતરને 8-12% થી 3% થી ઓછા સુધી ઘટાડે છે.

અડાજણ અને અઠવા: સુરતનો પ્રીમિયમ રહેણાંક પટ્ટો

અડાજણ અને અઠવા સુરતના સમૃદ્ધ રહેણાંક કોરનું પ્રતિનિધિત્વ કરે છે. આધુનિક એપાર્ટમેન્ટ્સ, બંગલો સોસાયટીઓ, પ્રીમિયમ રિટેલ સ્ટ્રીટ્સ અને ઉચ્ચ-સ્તરના મોડર્ન ટ્રેડ આઉટલેટ્સ આ વિસ્તારને વ્યાખ્યાયિત કરે છે. વિતરણ લાક્ષણિકતાઓ:

- ગ્રાહક પ્રોફાઇલ: બિઝનેસ પરિવારો, હીરા વેપારીઓ, ટેક્સટાઇલ વેપારીઓ, વ્યવસાયિકો

- FMCG પસંદગીઓ: ઓર્ગેનિક ઉત્પાદનો, આયાતી બ્રાન્ડ્સ, પ્રીમિયમ ડેરી, હેલ્થ ફૂડ્સ

- મોડર્ન ટ્રેડ: D-Mart, Reliance Smart, Big Bazaar વારસો, સ્થાનિક પ્રીમિયમ સ્ટોર્સ

- વિતરણ પડકાર: ઉચ્ચ સેવા અપેક્ષાઓ, કડક ડિલિવરી વિન્ડો, રિટર્ન શિસ્ત

- તક: સુરતમાં સૌથી વધુ સરેરાશ ઓર્ડર મૂલ્યો, મજબૂત મોડર્ન ટ્રેડ માર્જિન

અડાજણ અને અઠવાને નફાકારક રીતે સેવા આપવા માટે SLA ટ્રેકિંગ, મોડર્ન ટ્રેડ ડોક શેડ્યુલિંગ અને ચાર્જબેક મેનેજમેન્ટ સાથેના ડિસ્ટ્રિબ્યુટર મેનેજમેન્ટ પ્લેટફોર્મ ની જરૂર છે. અહીંના પ્રીમિયમ ગ્રાહકો ઓછા ભાવ-સંવેદનશીલ છે પરંતુ અત્યંત ગુણવત્તા-સંવેદનશીલ છે — ક્ષતિગ્રસ્ત માલ અથવા મોડી ડિલિવરી માસ-માર્કેટ ઝોન કરતાં ઝડપથી બ્રાન્ડ ઇક્વિટીને ઘટાડે છે.

કતારગામ: ટેક્સટાઇલ હબ અને માસ માર્કેટ એન્જિન

કતારગામ અને આસપાસના વિસ્તારો (અમરોલી, પાંડેસરા, ઉધના) સુરતનો ટેક્સટાઇલ ઉત્પાદન પટ્ટો બનાવે છે. 50,000 થી વધુ પાવર લૂમ્સ અને પ્રોસેસિંગ યુનિટ્સ અહીં કાર્યરત છે, જે વિશાળ કાર્યબળને રોજગાર આપે છે જે ઉચ્ચ-વોલ્યુમ FMCG વપરાશ ચલાવે છે. વિતરણ લાક્ષણિકતાઓ:

- ગ્રાહક પ્રોફાઇલ: ટેક્સટાઇલ કામદારો (Rs 12,000-30,000/મહિને), UP, બિહાર, ઓડિશાના સ્થળાંતરિત પરિવારો

- FMCG પસંદગીઓ: વેલ્યુ પેક્સ, ઇકોનોમી SKUs, પ્રાદેશિક બ્રાન્ડ્સ, બલ્ક ખરીદી

- આઉટલેટ પ્રકાર: ગાઢ કિરાણા, જથ્થાબંધ બજારો, કામદાર કેન્ટીન

- વિતરણ પડકાર: ભાવ-સંવેદનશીલ, ઉચ્ચ ક્રેડિટ માંગ, મોસમી કાર્યબળ વધઘટ

- તક: વિશાળ વોલ્યુમ — વ્યક્તિગત કિરાણા Rs 3-5 લાખ/મહિને FMCG ખસેડે છે

કતારગામને વોલ્યુમ-ફર્સ્ટ વિતરણ વ્યૂહરચનાની જરૂર છે. બીટ પ્લાન્સે ઝડપી ઓર્ડર-થી-ડિસ્પેચ ચક્ર સાથે દરરોજ 50-70 આઉટલેટ્સ આવરી લેવા જોઈએ. સ્કીમ એન્જિન્સ જે સ્લેબ ડિસ્કાઉન્ટ અને ફ્રી-ગુડ્સ ઓફર્સને ઓટોમેટ કરે છે તે આવશ્યક છે — ટેક્સટાઇલ પટ્ટાના રિટેલરો મુખ્યત્વે માર્જિન અને સ્કીમ્સ પર ચાલે છે, અને આ વોલ્યુમ પર મેન્યુઅલ સ્કીમ ગણતરી ભૂલો અને વિવાદોની ખાતરી આપે છે.

વેસુ, પાલ અને ડુમાસ રોડ: ઉભરતા પ્રીમિયમ કોરિડોર

સુરતના દક્ષિણ વિસ્તરણે નવા પ્રીમિયમ રહેણાંક અને વ્યવસાયિક કોરિડોર બનાવ્યા છે. IT કંપનીઓ, શૈક્ષણિક સંસ્થાઓ અને લાઇફસ્ટાઇલ રિટેલ પ્રીમિયમ FMCG શ્રેણીઓ માટે માંગ ચલાવી રહ્યા છે. આ વિસ્તારો હજુ પણ ઓછા-વિતરિત છે, જે પ્રારંભિક કવરેજમાં રોકાણ કરવા તૈયાર બ્રાન્ડ્સ માટે નોંધપાત્ર ફર્સ્ટ-મૂવર ફાયદો આપે છે.

રિંગ રોડ ઔદ્યોગિક કોરિડોર

સુરતનો રિંગ રોડ ટેક્સટાઇલ પ્રોસેસિંગ, પેકેજિંગ અને લોજિસ્ટિક્સ કંપનીઓને હોસ્ટ કરે છે. સંસ્થાકીય FMCG માંગ — કામદાર કેન્ટીન, કોર્પોરેટ પેન્ટ્રી, બલ્ક સપ્લાય — નોંધપાત્ર છે પરંતુ રિટેલ વિતરણથી અલગ B2B વિતરણ વર્કફ્લોની જરૂર છે. માસિક ઇન્વોઇસિંગ, બલ્ક પ્રાઇસિંગ અને 30-45 દિવસનું ક્રેડિટ મેનેજમેન્ટ માનક છે.

સુરતમાં FMCG માર્જિન: વિતરકોએ શું અપેક્ષા રાખવી જોઈએ

સુરતના વિતરક માર્જિન શ્રેણી અને ચેનલ દ્વારા નોંધપાત્ર રીતે અલગ પડે છે:

| શ્રેણી | વિતરક માર્જિન (GT) | વિતરક માર્જિન (MT) |

|---|---|---|

| ખાદ્ય તેલ | 2.5-4% | 1.5-2.5% |

| પેકેજ્ડ સ્નેક્સ | 8-12% | 5-8% |

| વ્યક્તિગત સંભાળ | 10-15% | 6-10% |

| ડેરી અને બેવરેજિસ | 6-10% | 4-7% |

| હેલ્થ ફૂડ્સ અને ઓર્ગેનિક | 15-22% | 10-15% |

| હોમ કેર અને ક્લીનિંગ | 8-12% | 5-8% |

| પ્રાદેશિક/સ્થાનિક બ્રાન્ડ્સ | 12-20% | 8-14% |

સુરત માટે મુખ્ય માર્જિન અંતર્દૃષ્ટિ: પ્રાદેશિક અને પ્રીમિયમ બ્રાન્ડ્સ રાષ્ટ્રીય માસ બ્રાન્ડ્સ કરતાં નોંધપાત્ર રીતે વધુ સારા વિતરક માર્જિન આપે છે. વિતરકો જે સંતુલિત પોર્ટફોલિયો બનાવે છે — વોલ્યુમ માટે રાષ્ટ્રીય બ્રાન્ડ્સ, માર્જિન માટે પ્રાદેશિક અને પ્રીમિયમ બ્રાન્ડ્સ — સતત સિંગલ-પોર્ટફોલિયો ઓપરેટરો કરતાં વધુ સારું પ્રદર્શન કરે છે. એનાલિટિક્સ ડેશબોર્ડ્સ જે પ્રતિ SKU પ્રતિ રૂટ માર્જિન ટ્રેક કરે છે તે આ મિક્સને સતત ઑપ્ટિમાઇઝ કરવામાં મદદ કરે છે.

FMCG વિતરક અર્થશાસ્ત્રની વ્યાપક સમજ માટે, અમારું FMCG વિતરક માર્જિન અને નફો માર્ગદર્શિકા જુઓ.

ગુજરાતી ગ્રાહક પસંદગીઓ જે વિતરણને આકાર આપે છે

શાકાહાર અને જૈન પ્રભાવ

ગુજરાતમાં ભારતની સૌથી વધુ શાકાહારી વસ્તી છે — 60% થી વધુ — અને સુરતમાં વધુ કડક આહાર જરૂરિયાતો (કોઈ ડુંગળી નહીં, કોઈ લસણ નહીં, કોઈ મૂળ શાકભાજી નહીં) સાથેનો નોંધપાત્ર જૈન સમુદાય છે. આ FMCG વિતરણને ગહન રીતે આકાર આપે છે:

- પેકેજ્ડ ખોરાકમાં સ્પષ્ટ શાકાહારી/જૈન લેબલિંગ હોવું જોઈએ

- સમર્પિત જૈન ઉત્પાદન રેખાઓ (સ્નેક્સ, મીઠાઈઓ, રેડી-ટુ-ઇટ) પ્રીમિયમ કિંમતની માંગ કરે છે

- નોન-વેજ FMCG ઉત્પાદનોની માંગ મર્યાદિત પરંતુ વધી રહી છે (સ્થળાંતરિત વસ્તી દ્વારા સંચાલિત)

- માથાદીઠ ડેરી વપરાશ ભારતમાં સૌથી વધુ છે — દૂધ, ઘી, પનીર, દહીં વિશાળ જથ્થા ખસેડે છે

વિતરકોને SKU વર્ગીકરણ અને ઇન્વેન્ટરી મેનેજમેન્ટ ની જરૂર છે જે વેરહાઉસ કામગીરી અને રિટેલર ઓર્ડરિંગ બંને માટે શાકાહારી, જૈન-ફ્રેન્ડલી અને નોન-શાકાહારી ઉત્પાદનોને સ્પષ્ટપણે અલગ કરે છે.

બ્રાન્ડ વફાદારી અને ગુજરાતી પ્રીમિયમ

એકવાર વિશ્વાસ સ્થાપિત થાય પછી ગુજરાતી ગ્રાહકો પ્રખ્યાત રીતે બ્રાન્ડ-વફાદાર છે પરંતુ નવી બ્રાન્ડ્સ પ્રત્યે તીવ્રપણે શંકાસ્પદ છે. વિશ્વાસ બનાવવા માટે સતત ઉપલબ્ધતા, ગુણવત્તાની ખાતરી અને માઉથ-થી-માઉથ — એકલા ભારે જાહેરાત નહીં — ની જરૂર છે. આનો અર્થ એ છે કે મોટાભાગના ભારતીય શહેરો કરતાં સુરતમાં વિતરણ સુસંગતતા વધુ મહત્વપૂર્ણ છે. માત્ર 2-3 દિવસ ચાલતો સ્ટોકઆઉટ વફાદાર ગ્રાહકોને કાયમ માટે સ્પર્ધકો તરફ બદલી શકે છે.

ઝીરો-સેલ્સ એલર્ટ સાથે ડિજિટલ રિટેલર ટ્રેકિંગ ખાતરી કરે છે કે વિતરકો ઉપલબ્ધતા અંતરને બ્રાન્ડ-સ્વિચિંગ ઘટનાઓ બને તે પહેલા પકડી લે.

મીઠાશ માટેનો સ્વાદ અને સ્નેકિંગ સંસ્કૃતિ

સુરત ભારતની સ્નેકિંગ અને મીઠાઈ રાજધાની છે. પેકેજ્ડ સ્નેક્સ, નમકીન અને મીઠાઈઓનો માથાદીઠ વપરાશ રાષ્ટ્રીય સરેરાશ કરતાં 2-3 ગણો છે. Balaji Wafers, Gopal Namkeen અને Atul Bakery જેવી સ્થાનિક બ્રાન્ડ્સ રાષ્ટ્રીય ખેલાડીઓ સાથે પ્રભુત્વ ધરાવતા બજાર હિસ્સાની માંગ કરે છે. વિતરકો જે સ્થાનિક અને રાષ્ટ્રીય બંને સ્નેક બ્રાન્ડ્સ વહન કરે છે તે આઉટલેટ પેનિટ્રેશનને મહત્તમ બનાવે છે — સુરતમાં રિટેલરો એવા વિતરક સાથે કામ કરશે નહીં જે Lay's સાથે Balaji સપ્લાય કરી શકતા નથી.

તહેવાર-સંચાલિત માંગ સ્પાઇક્સ

ગુજરાતનું તહેવાર કેલેન્ડર આત્યંતિક માંગ વોલેટિલિટી ચલાવે છે. ઉત્તરાયણ (જાન્યુઆરી), નવરાત્રી (ઓક્ટોબર), દિવાળી (ઓક્ટોબર-નવેમ્બર) અને ધનતેરસ ચોક્કસ શ્રેણીઓમાં 3-5x સામાન્ય માંગ સ્પાઇક્સ બનાવે છે — રસોઈ તેલ, મીઠાઈઓ, સૂકા મેવા, વ્યક્તિગત સંભાળ ગિફ્ટ પેક્સ અને ક્લીનિંગ ઉત્પાદનો. ઐતિહાસિક માંગ એનાલિટિક્સ અને પ્રી-પોઝિશનિંગ ક્ષમતાઓ વગરના વિતરકો સતત તહેવારો દરમિયાન ઓછો સ્ટોક કરે છે અને પછી વધુ સ્ટોક કરે છે.

સ્થાનિક વિ રાષ્ટ્રીય બ્રાન્ડ્સ: સુરત ગતિશીલતા

સુરતમાં ભારતની સૌથી રસપ્રદ સ્થાનિક-વિ-રાષ્ટ્રીય બ્રાન્ડ ગતિશીલતામાંની એક છે. મજબૂત સ્થાનિક બ્રાન્ડ્સ ઘણી FMCG શ્રેણીઓ પર પ્રભુત્વ ધરાવે છે:

| શ્રેણી | અગ્રણી સ્થાનિક બ્રાન્ડ | રાષ્ટ્રીય સ્પર્ધક | સ્થાનિક બ્રાન્ડ હિસ્સો (અંદાજ) |

|---|---|---|---|

| સ્નેક્સ/નમકીન | Balaji Wafers, Gopal | Lay's, Haldiram's | 55-65% |

| બેકરી | Atul Bakery, Monginis | Britannia, Parle | 35-45% |

| ડેરી | Amul, Sagar | Mother Dairy, Nestle | 70%+ |

| ખાદ્ય તેલ | Tirupati, Gemini | Fortune, Saffola | 40-50% |

| મસાલા | Ramdev, Badshah | MDH, Everest | 50-60% |

વિતરકો માટે વ્યૂહાત્મક અસર: તમે મજબૂત સ્થાનિક બ્રાન્ડ ભાગીદારી વગર સધ્ધર સુરત વિતરણ વ્યવસાય બનાવી શકતા નથી. રિટેલરો અપેક્ષા રાખે છે કે તેમના પ્રાથમિક વિતરક પ્રભુત્વ ધરાવતી સ્થાનિક બ્રાન્ડ્સ વહન કરે. માત્ર-રાષ્ટ્રીય વિતરકો 40-50% થી નીચે આઉટલેટ પેનિટ્રેશન સાથે સંઘર્ષ કરે છે, જ્યારે સ્થાનિક અને રાષ્ટ્રીય બંને પોર્ટફોલિયો વહન કરતા મલ્ટિ-બ્રાન્ડ ઓપરેટરો 70-85% પેનિટ્રેશન પ્રાપ્ત કરે છે.

મલ્ટિ-બ્રાન્ડ પોર્ટફોલિયોનું સંચાલન કરવા માટે સક્ષમ ડિસ્ટ્રિબ્યુટર મેનેજમેન્ટ સિસ્ટમ ની જરૂર છે જે બ્રાન્ડ-મુજબ સ્કીમ્સ, અલગ લેજર્સ, બ્રાન્ડ-વિશિષ્ટ કિંમતો અને એકીકૃત રિપોર્ટિંગ સંભાળે — બધું વેરહાઉસ ટીમને દબાવી દેતી કાર્યકારી જટિલતા વગર.

સુરત માટે વિશિષ્ટ વિતરણ પડકારો

1. ચોમાસું અને પૂરનું જોખમ

સુરત ભારતના સૌથી પૂર-પ્રવણ શહેરોમાંનું એક છે. 2006 ની તાપી નદીના પૂર સંદર્ભ બિંદુ રહે છે, પરંતુ નિયમિત ચોમાસું પણ કતારગામ, ઉધના, પાંડેસરા અને વરાછાના ભાગો જેવા નીચાણવાળા વિસ્તારોમાં પાણી ભરાવાનું કારણ બને છે. વિતરણ ઓપરેટરોએ આ માટે યોજના કરવી જોઈએ:

- ભારે ચોમાસાની ઘટનાઓ દરમિયાન 2-5 દિવસનો સંપૂર્ણ ડિલિવરી શટડાઉન

- જૂન પહેલા ઊંચા વેરહાઉસમાં બફર સ્ટોક પ્રી-પોઝિશનિંગ

- પ્રાથમિક રસ્તાઓ ભરાય ત્યારે રીરૂટિંગ ક્ષમતા

- લાસ્ટ-માઇલ ડિલિવરી માટે વોટરપ્રૂફ પેકેજિંગ

એકીકૃત ફ્લીટ મેનેજમેન્ટ અને ટ્રાફિક-જાગૃત રૂટ ઓપ્ટિમાઇઝેશન ધરાવતા વિતરકો ચોમાસા દરમિયાન 75-80% ડિલિવરી અનુપાલન જાળવી રાખે છે, જ્યારે મેન્યુઅલ ઓપરેટરો માટે આ 40-50% છે. ચોમાસાની યોજનાના વ્યાપક પરિપ્રેક્ષ્ય માટે, FMCG માં ચોમાસાના વિતરણ પડકારો પરની અમારી માર્ગદર્શિકા જુઓ.

2. રોકડ-આધારિત અર્થતંત્ર અને ચુકવણી સંગ્રહ

ભારતના ડિજિટલ ચુકવણી દબાણ છતાં, સુરતના હીરા અને ટેક્સટાઇલ ઉદ્યોગો નોંધપાત્ર રીતે રોકડ પર ચાલે છે. ઘણા હીરા પોલિશિંગ યુનિટ્સ કામદારોને રોકડમાં ચૂકવણી કરે છે, અને આ રોકડ અર્થતંત્ર રિટેલ વ્યવહારો સુધી વિસ્તરે છે. વિતરકો સમકક્ષ શહેરો કરતાં વધુ રોકડ-હેન્ડલિંગ આવશ્યકતાઓનો સામનો કરે છે. રીઅલ-ટાઇમ સમાધાન સાથે ડિજિટલ ચુકવણી સંગ્રહ આનું સંચાલન કરવામાં મદદ કરે છે — જ્યાં શક્ય હોય ત્યાં UPI અને બેંક ટ્રાન્સફર કેપ્ચર કરે છે જ્યારે જ્યાં રોકડ પ્રભુત્વ ધરાવે છે ત્યાં કડક રોકડ સંગ્રહ શિસ્ત જાળવી રાખે છે.

3. શ્રમ ઉપલબ્ધતા અને જાળવણી

સુરતના હીરા અને ટેક્સટાઇલ ઉદ્યોગો વેરહાઉસ અને ડિલિવરી શ્રમ માટે FMCG વિતરણ સાથે સીધી સ્પર્ધા કરે છે. પીક હીરા પ્રોસેસિંગ સીઝન દરમિયાન, શ્રમ ખર્ચ 20-30% વધે છે અને નોકરી છોડવાનું વધે છે. વિતરણ ઓપરેટરોને સ્પર્ધાત્મક વેતન અને ટેકનોલોજીની જરૂર છે જે શ્રમ નિર્ભરતા ઘટાડે — ઓટોમેટેડ ઓર્ડર પ્રોસેસિંગ, ડિજિટલ પિકિંગ યાદીઓ અને મોબાઇલ એપ-આધારિત ડિલિવરી પુષ્ટિ પ્રતિ-ઓર્ડર શ્રમ આવશ્યકતાઓને 30-40% ઘટાડે છે.

4. ભાષા અને સંચાર

સુરતનું કાર્યબળ ગુજરાતી, હિન્દી, કાઠિયાવાડી, મારવાડી અને વધુને વધુ ઓડિયા અને ભોજપુરી બોલે છે. વિતરણ સોફ્ટવેર અને ફિલ્ડ-ફોર્સ ટૂલ્સે બહુભાષી ઇન્ટરફેસને સપોર્ટ કરવો જોઈએ. ગુજરાતી અને હિન્દી ભાષાના સપોર્ટ સાથેની મોબાઇલ એપ્સ ડિલિવરી સ્ટાફ અને બીટ સેલ્સમેન વચ્ચે 40-50% વધુ અપનાવવાનો દર જુએ છે.

5. ટેક્સટાઇલ મંદીમાં ક્રેડિટ જોખમ

સુરતનો ટેક્સટાઇલ ઉદ્યોગ ચક્રીય છે અને વૈશ્વિક માંગ વધઘટ માટે ખુલ્લો છે. મંદી દરમિયાન, ટેક્સટાઇલ પટ્ટાના રિટેલરો રોકડ પ્રવાહના દબાણનો સામનો કરે છે જે FMCG ચુકવણીમાં વિલંબમાં કાસ્કેડ થાય છે. વિતરકોને સક્રિય ક્રેડિટ લિમિટ મેનેજમેન્ટ ની જરૂર છે જે માત્ર ઐતિહાસિક ચુકવણી પેટર્ન જ નહીં પણ ઉદ્યોગ સ્થિતિના આધારે એક્સપોઝરને સમાયોજિત કરે છે.

સુરત FMCG વિતરણમાં ટેકનોલોજી અપનાવવી

વર્તમાન સ્થિતિ

સુરતનું વિતરણ ટેકનોલોજી અપનાવવું પુણે અને બેંગ્લોરથી પાછળ છે પરંતુ ઝડપથી વેગ પકડી રહ્યું છે. મોટાભાગના વિતરકો સ્ટેજ 1-2 માં છે:

- સ્ટેજ 1 (Tally + મેન્યુઅલ): 55-60% સુરત વિતરકો — પેપર ઓર્ડર્સ, મેન્યુઅલ રૂટ્સ, Tally બિલિંગ

- સ્ટેજ 2 (Tally + મૂળભૂત DMS): 25-30% — એપ-આધારિત ઓર્ડર્સ, મૂળભૂત રૂટ પ્લાનિંગ

- સ્ટેજ 3 (સંપૂર્ણ DMS + ERP): 10-15% — રીઅલ-ટાઇમ એનાલિટિક્સ સાથે એન્ડ-ટુ-એન્ડ ઓટોમેશન

આ અપનાવવાનું અંતર પ્રચંડ તક રજૂ કરે છે. વિતરકો જે સ્પર્ધકો પહેલા સ્ટેજ 3 પર જાય છે તેઓ કવરેજ, ખર્ચ કાર્યક્ષમતા અને બ્રાન્ડ સંબંધોમાં માળખાકીય ફાયદાઓ મેળવે છે. સંક્રમણ માટે માર્ગદર્શન માટે, અમારી Tally થી DMS સ્થળાંતર માર્ગદર્શિકા જુઓ.

ટેકનોલોજી જે સુરતમાં ROI આપે છે

ડિજિટલ ઓર્ડર મેનેજમેન્ટ: ફોન-આધારિત ઓર્ડરિંગ અરાજકતાને માળખાગત એપ-આધારિત ઓર્ડરિંગ સાથે બદલે છે. સુરત વિતરકો અપનાવ્યા પછી ઓર્ડર ચોકસાઈમાં 20-25% સુધારો અને ઓર્ડર-પ્રોસેસિંગ સમયમાં 45% ઘટાડો જણાવે છે.

રૂટ ઓપ્ટિમાઇઝેશન: સુરતના ભીડભાડવાળા હીરા અને ટેક્સટાઇલ પટ્ટાઓ રૂટ ઓપ્ટિમાઇઝેશન ને નિર્ણાયક બનાવે છે. સ્માર્ટ રૂટિંગ દરરોજ પ્રતિ રૂટ 2-4 કલાક બચાવે છે અને પ્રતિ બીટ આવરી લેવાયેલા આઉટલેટ્સને 40 થી 60-70 સુધી વધારે છે.

સ્કીમ ઓટોમેશન: મલ્ટિ-બ્રાન્ડ પોર્ટફોલિયોમાં 15-20 સહવર્તી સ્કીમ્સ ચાલતી હોવા સાથે, મેન્યુઅલ સ્કીમ ગણતરી ભૂલો વગર અશક્ય છે. સ્કીમ એન્જિન્સ વિવાદો દૂર કરે છે અને 95%+ અનુપાલન સુનિશ્ચિત કરે છે.

GST-અનુપાલન બિલિંગ: E-invoicing આદેશો કડક બની રહ્યા છે. ઓટોમેટેડ GST અને e-invoice જનરેશન સાથેનું એકીકૃત બિલિંગ અનુપાલન જોખમ દૂર કરે છે.

ફિલ્ડ ફોર્સ ટ્રેકિંગ: જિયો-ફેન્સિંગ સાથેનું હાજરી ટ્રેકિંગ અને મોબાઇલ એપ-આધારિત મુલાકાત પુષ્ટિ ફિલ્ડ ફોર્સ ઉત્પાદકતામાં 20-30% વધારો કરે છે.

બીટ પ્લાનિંગ: ડેટા-આધારિત પ્રદેશ ફાળવણી સાથેનું માળખાગત બીટ પ્લાનિંગ સુરતના વિવિધ ઝોનમાં શ્રેષ્ઠ કવરેજ સુનિશ્ચિત કરે છે.

સુરતમાં FMCG બ્રાન્ડ્સ માટેની તકો (2026)

1. પ્રીમિયમ અને ઓર્ગેનિક FMCG

સુરતની ઉચ્ચ ડિસ્પોઝેબલ આવક અને આરોગ્ય-સભાન હીરા ઉદ્યોગ કાર્યબળ વધતા પ્રીમિયમ FMCG બજાર બનાવે છે. ઓર્ગેનિક ઘી, કોલ્ડ-પ્રેસ્ડ તેલ, પ્રીમિયમ હેલ્થ ડ્રિંક્સ અને નેચરલ વ્યક્તિગત સંભાળ ઉત્પાદનો વાર્ષિક 25-30% ના દરે વધી રહ્યા છે. વિતરકો જે અડાજણ, અઠવા અને વેસુમાં પ્રીમિયમ-કેન્દ્રિત સબ-ડિસ્ટ્રિબ્યુશન ચેનલો બનાવે છે તે માસ-માર્કેટ વિતરણ કરતાં 2-3 ગણા વધારે માર્જિન કબજે કરે છે.

2. સંસ્થાકીય અને B2B વિતરણ

સુરતના 50,000+ ટેક્સટાઇલ યુનિટ્સ અને 5,000+ હીરા યુનિટ્સ કામદાર કેન્ટીન, પેન્ટ્રી અને કલ્યાણ સપ્લાય દ્વારા સંસ્થાકીય FMCG વોલ્યુમ વાપરે છે. આ B2B ચેનલ ઓછી-સેવા પ્રાપ્ત છે અને અનુમાનિત માંગ સાથે પુનરાવર્તિત આવક આપે છે. સંસ્થાકીય ખાતાઓને કાર્યક્ષમ રીતે સેવા આપવા માટે CFA અને ડેપો મેનેજમેન્ટ ક્ષમતાઓ આવશ્યક છે.

3. નવી ટાઉનશિપ ફર્સ્ટ-મૂવર ફાયદો

વેસુ, પાલ, અલથાણ અને ડિંડોલીમાં દરેક નવી ટાઉનશિપ 2-3 વર્ષમાં 5,000-15,000 નવા ઘરો બનાવે છે. વિતરકો જે સ્પર્ધા સ્થાપિત થાય તે પહેલા કવરેજ સ્થાપિત કરે છે તેઓ 60-70% બજાર હિસ્સો કબજે કરે છે જે વર્ષો સુધી ચાલુ રહે છે. ડિસ્ટ્રિબ્યુશન કવરેજ એનાલિટિક્સ દ્વારા વહેલી શોધ અહીં સ્પર્ધાત્મક હથિયાર છે.

4. પ્રાદેશિક બ્રાન્ડ વિતરણ

ગુજરાતની ઘણી પ્રિય પ્રાદેશિક બ્રાન્ડ્સ પાસે સુરતમાં વ્યવસાયિક વિતરણ ઇન્ફ્રાસ્ટ્રક્ચરનો અભાવ છે. વિતરકો જે મલ્ટિ-બ્રાન્ડ, ટેકનોલોજી-સક્ષમ વિતરણ આપે છે તે ખંડિત પ્રાદેશિક બ્રાન્ડ સપ્લાય ચેઇન્સને એકીકૃત કરી શકે છે અને અત્યંત નફાકારક પોર્ટફોલિયો બનાવી શકે છે. સિંગલ પ્લેટફોર્મ પર મલ્ટિ-બ્રાન્ડ વિતરણ પરની અમારી માર્ગદર્શિકા કાર્યકારી મોડેલને આવરી લે છે.

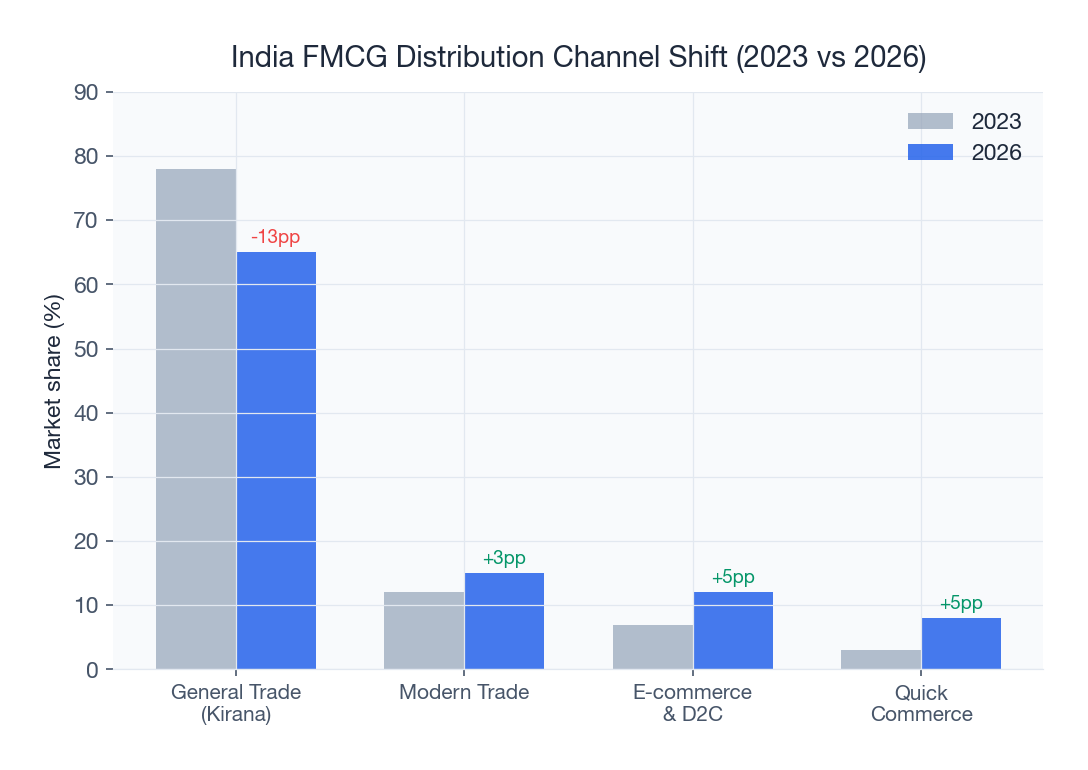

5. ક્વિક કોમર્સ અને ઇ-કોમર્સ ફુલફિલમેન્ટ

ક્વિક કોમર્સ Blinkit, Zepto અને Swiggy Instamart દ્વારા સુરતમાં પ્રવેશી રહ્યું છે. વિતરકો જે પોતાને આ પ્લેટફોર્મ માટે ડાર્ક-સ્ટોર સપ્લાયર તરીકે સ્થાન આપે છે તે પરંપરાગત વિતરણને કેનિબલાઇઝ કર્યા વગર ઉચ્ચ-વૃદ્ધિ ચેનલ ઉમેરે છે. આ લેન્ડસ્કેપને સમજવું નિર્ણાયક છે — FMCG વિતરણ પર ક્વિક કોમર્સની અસર નું અમારું વિશ્લેષણ જુઓ.

સુરત વિતરકો માટે ROI બેંચમાર્ક

| KPI | સરેરાશ (સુરત) | ટોપ-ક્વાર્ટાઇલ (સુરત) |

|---|---|---|

| પ્રતિ બીટ/દિવસ આઉટલેટ્સ | 40-50 | 65-75 |

| ઓર્ડર-થી-ડિસ્પેચ સમય | 4-6 કલાક | 90 મિનિટથી ઓછા |

| ફિલ રેટ | 85% | 96%+ |

| DSO (બાકી દિવસોના વેચાણ) | 16-22 દિવસ | 8-12 દિવસ |

| સ્કીમ અનુપાલન | 72% | 94%+ |

| ડિલિવરી અનુપાલન (ચોમાસું) | 45% | 80%+ |

| પ્રતિ આઉટલેટ સેવા આપવાનો ખર્ચ | Rs 85-120 | Rs 50-70 |

| ફિલ્ડ ફોર્સ ટર્નઓવર (વાર્ષિક) | 32% | 18% થી ઓછા |

વિતરકો જે ફુલ-સ્ટેક વિતરણ ટેકનોલોજી અપનાવે છે તેઓ સતત 6-9 મહિનામાં સરેરાશથી ટોપ-ક્વાર્ટાઇલ પ્રદર્શન સુધી જાય છે. ROI નોંધપાત્ર છે — વિગતવાર ગણતરી ફ્રેમવર્ક માટે, અમારું વિતરણ સોફ્ટવેર ROI કેલ્ક્યુલેટર જુઓ.

સુરતમાં લોન્ચ કરવું: વિતરકની ચેકલિસ્ટ

- સચિન GIDC અથવા પાંડેસરા ઔદ્યોગિક વિસ્તારમાં વેરહાઉસ જગ્યા સુરક્ષિત કરો (ઓછું ભાડું, સારી રોડ એક્સેસ)

- વરાછા, અડાજણ/અઠવા, કતારગામ/ઉધના, રિંગ રોડ અને વેસુ/પાલને આવરી લેતા 4-6 વિતરકોની નિમણૂક કરો

- રિટેલરો સુધી પહોંચતા પહેલા ઓછામાં ઓછી 2-3 મજબૂત સ્થાનિક બ્રાન્ડ્સ (Balaji, Gopal, Amul) સાથે ભાગીદારી કરો

- પ્રથમ દિવસથી મોબાઇલ એપ સાથે સંપૂર્ણ DMS તૈનાત કરો — મેન્યુઅલ શરૂ ન કરો અને પછી સ્થળાંતર કરો

- સુરતમાં તમારા પ્રથમ જૂન પહેલા ચોમાસાની આકસ્મિક યોજના બનાવો

- ટેક્સટાઇલ પટ્ટાના આઉટલેટ્સ માટે ક્રેડિટ લિમિટ રૂઢિચુસ્ત રીતે સેટ કરો, માસિક સમીક્ષા કરો

- 6 મહિનામાં 2,500 આઉટલેટ્સ, 12 મહિનામાં 5,000 લક્ષ્ય રાખો

- લોન્ચથી GST-અનુપાલન બિલિંગ અને e-invoicing એકીકૃત કરો

- ડેટા-આધારિત એનાલિટિક્સ નો ઉપયોગ કરીને સાપ્તાહિક પ્રદર્શન સમીક્ષા કરો

- ફિલ્ડ ફોર્સ ભરતી વહેલી યોજના કરો — ડિલિવરી સ્ટાફ માટે સ્પર્ધા તીવ્ર છે

સુરત વિ અન્ય ગુજરાત FMCG બજારો

સુરતની વિતરણ ગતિશીલતા અમદાવાદ અને અન્ય ગુજરાત બજારોથી નોંધપાત્ર રીતે અલગ છે:

| પેરામીટર | સુરત | અમદાવાદ | વડોદરા |

|---|---|---|---|

| વૃદ્ધિ દર | 14-16% | 9-11% | 8-10% |

| પ્રીમિયમ SKU હિસ્સો | 28-32% | 22-26% | 18-22% |

| સ્થાનિક બ્રાન્ડ વર્ચસ્વ | ઉચ્ચ | ખૂબ ઉચ્ચ | મધ્યમ |

| મોડર્ન ટ્રેડ પરિપક્વતા | ઝડપથી વધી રહ્યું | પરિપક્વ | પ્રારંભિક તબક્કો |

| શ્રમ સ્પર્ધા | ખૂબ ઉચ્ચ (હીરા/ટેક્સટાઇલ) | મધ્યમ | નીચું |

| ચોમાસામાં વિક્ષેપનું જોખમ | ઉચ્ચ (તાપી પૂર) | નીચું | મધ્યમ |

| સ્થળાંતરિત ગ્રાહક વિવિધતા | ખૂબ ઉચ્ચ | મધ્યમ | નીચું |

ગુજરાતના વિતરણ લેન્ડસ્કેપના વ્યાપક દૃશ્ય માટે, અમારું ગુજરાત ડેરી સપ્લાય ચેઇન વિશ્લેષણ જુઓ.

FMCG માટે સુરતનું તહેવાર અને મોસમી કેલેન્ડર

ઇન્વેન્ટરી પ્લાનિંગ માટે સુરતના માંગ કેલેન્ડરને સમજવું આવશ્યક છે:

- ઉત્તરાયણ (14 જાન્યુઆરી): સ્નેક્સ, બેવરેજિસ, ખાદ્ય તેલમાં વિશાળ સ્પાઇક. સુરતનો પતંગ તહેવાર 2 અઠવાડિયા માટે સામાન્ય સ્નેક વેચાણને 4-5 ગણું ચલાવે છે

- હોળી (માર્ચ): વ્યક્તિગત સંભાળ, રંગો, મીઠાઈઓ, બેવરેજિસમાં ઉછાળો

- નવરાત્રી (ઓક્ટોબર): 9-દિવસનો તહેવાર રસોઈ તેલ, ઘી, સ્નેક અને મીઠાઈની માંગ ચલાવે છે. ગુજરાતની સૌથી મોટી સાંસ્કૃતિક ઘટના

- દિવાળી/ધનતેરસ (ઓક્ટોબર-નવેમ્બર): સમગ્ર FMCG ઉછાળો, ખાસ કરીને સૂકા મેવા, મીઠાઈઓ, વ્યક્તિગત સંભાળ ગિફ્ટ પેક્સ, ક્લીનિંગ ઉત્પાદનો

- લગ્ન સીઝન (નવેમ્બર-ફેબ્રુઆરી): બલ્ક ખરીદી, કેટરિંગ સપ્લાય, વ્યક્તિગત સંભાળ માટે સતત માંગ

- ચોમાસું (જૂન-સપ્ટેમ્બર): માંગ ઇન્ડોર વપરાશ તરફ વળે છે — પેકેજ્ડ ખોરાક, બેવરેજિસ, હેલ્થ ઉત્પાદનો વધે છે જ્યારે નાશવંત વિતરણને લોજિસ્ટિક્સ પડકારોનો સામનો કરવો પડે છે

વિતરકો જે દરેક તહેવારના 8-12 અઠવાડિયા પહેલા ઐતિહાસિક એનાલિટિક્સ નો ઉપયોગ કરીને યોજના કરે છે તેઓ સતત પ્રતિક્રિયાશીલ ઓપરેટરો કરતાં 25-35% વધુ મોસમી આવક કબજે કરે છે. અમારી તહેવારી સીઝન વિતરણ યોજના માર્ગદર્શિકા વિગતવાર ફ્રેમવર્ક પ્રદાન કરે છે.

સુરતનું લાંબા ગાળાનું વ્યૂહાત્મક મહત્વ

FMCG બ્રાન્ડ્સ માટે સુરતનું વ્યૂહાત્મક મહત્વ વેગ આપતા માર્ગ પર છે. આગામી દિલ્હી-મુંબઈ ઔદ્યોગિક કોરિડોર (DMIC) સુરત થઈને પસાર થાય છે, સૂચિત બુલેટ ટ્રેન સુરતને મુંબઈ અને અમદાવાદ સાથે જોડશે, અને સુરત ડાયમંડ બોર્સ — વિશ્વનું સૌથી મોટું ઓફિસ બિલ્ડિંગ — એ શહેરના આર્થિક મહત્વને વધુ એકીકૃત કર્યું છે. આ ઇન્ફ્રાસ્ટ્રક્ચર રોકાણો આગામી દાયકા માટે રાષ્ટ્રીય સરેરાશથી ઘણા વધારે વસ્તી વૃદ્ધિ, ઔદ્યોગિક વિસ્તરણ અને FMCG વપરાશ વૃદ્ધિને ચલાવશે.

બ્રાન્ડ્સ અને વિતરકો જે હવે મજબૂત સુરત કામગીરી સ્થાપિત કરે છે તેઓ ગુજરાતના — અને ભારતના — FMCG વૃદ્ધિનો અપ્રમાણસર હિસ્સો કબજે કરવા માટે પોતાને સ્થાન આપી રહ્યા છે. જાગૃતિ વધતી જાય તેમ ટેકનોલોજી-સક્ષમ વિતરણમાં ફર્સ્ટ-મૂવર ફાયદાની વિન્ડો સંકોચાઈ રહી છે. અમારા પ્રાઇસિંગ પેજ પર SpireStock ની ક્ષમતાઓનું અન્વેષણ કરો, અમારી 2026 DMS તુલના માં વિકલ્પો સાથે તુલના કરો, અથવા સુરત-વિશિષ્ટ વિતરણ વ્યૂહરચના કૉલ બુક કરો.

સ્ત્રોતો અને સંદર્ભો

- IBEF, India Brand Equity Foundation, Gujarat State Profile

- NielsenIQ, India FMCG Market Insights

- RBI, Reserve Bank of India, Handbook of Statistics on Indian States

- Surat Municipal Corporation, Surat City Profile and Demographics

વારંવાર પૂછાતા પ્રશ્નો

સુરતનું FMCG બજાર વાર્ષિક Rs 14,000-16,000 કરોડનું અંદાજવામાં આવે છે, જે વર્ષ-દર-વર્ષ 14-16% ના દરે વધી રહ્યું છે. શહેરના હીરા અને ટેક્સટાઇલ ઉદ્યોગો ટિયર-2 ભારતીય શહેરોમાં સૌથી વધુ માથાદીઠ ડિસ્પોઝેબલ આવક ઊભી કરે છે, જે FMCG વપરાશ પેટર્ન ચલાવે છે જે ટિયર-2 બજારોને બદલે મેટ્રો જેવા હોય છે.

સુરતની હીરા અને ટેક્સટાઇલ ઉદ્યોગની સંપત્તિ, મલ્ટિ-પ્રાદેશિક પસંદગીઓ સાથેનું વિશાળ સ્થળાંતરિત કાર્યબળ, ઉચ્ચ ડિસ્પોઝેબલ આવક, પૂર-પ્રવણ ભૂગોળ અને મજબૂત સ્થાનિક બ્રાન્ડ વફાદારીનું અનન્ય સંયોજન અન્ય કોઈપણ ગુજરાત અથવા ભારતીય ટિયર-2 શહેરથી અલગ વિતરણ ગતિશીલતા બનાવે છે. પ્રીમિયમ SKU અપનાવવાનો દર સમકક્ષ શહેરો કરતાં 30-40% વધારે છે.

સુરતના મુખ્ય FMCG વિતરણ ઝોન વરાછા (હીરા પટ્ટો, ઉચ્ચ-ઘનતા કિરાણા), અડાજણ અને અઠવા (પ્રીમિયમ રહેણાંક), કતારગામ અને ઉધના (ટેક્સટાઇલ પટ્ટો, માસ માર્કેટ), વેસુ અને પાલ (ઉભરતા પ્રીમિયમ) અને રિંગ રોડ કોરિડોર (સંસ્થાકીય અને B2B) છે. દરેક ઝોનને વિવિધ વિતરણ વ્યૂહરચનાઓ અને SKU મિક્સની જરૂર છે.

સુરત વિતરક માર્જિન જનરલ ટ્રેડમાં ખાદ્ય તેલ માટે 2.5-4% થી લઈને હેલ્થ ફૂડ અને ઓર્ગેનિક ઉત્પાદનો માટે 15-22% સુધી હોય છે. પ્રાદેશિક અને પ્રીમિયમ બ્રાન્ડ્સ રાષ્ટ્રીય માસ બ્રાન્ડ્સ કરતાં નોંધપાત્ર રીતે વધુ સારા માર્જિન આપે છે. વોલ્યુમ માટે રાષ્ટ્રીય બ્રાન્ડ્સ અને માર્જિન માટે પ્રાદેશિક બ્રાન્ડ્સનો સંતુલિત પોર્ટફોલિયો નફાકારકતાને ઑપ્ટિમાઇઝ કરે છે.

તાપી નદીને કારણે સુરત ભારતના સૌથી પૂર-પ્રવણ શહેરોમાંનું એક છે. નિયમિત ચોમાસું કતારગામ અને ઉધના જેવા નીચાણવાળા વિસ્તારોમાં 2-5 દિવસનો સંપૂર્ણ ડિલિવરી શટડાઉન કરે છે. રૂટ ઓપ્ટિમાઇઝેશન અને ફ્લીટ મેનેજમેન્ટ ટેકનોલોજી ધરાવતા વિતરકો ચોમાસા દરમિયાન 75-80% ડિલિવરી અનુપાલન જાળવી રાખે છે, જ્યારે મેન્યુઅલ ઓપરેટરો માટે આ 40-50% છે.

સ્થાનિક બ્રાન્ડ્સ ઘણી શ્રેણીઓમાં વર્ચસ્વ ધરાવતી બજાર હિસ્સો ધરાવે છે: Balaji Wafers અને Gopal (55-65% સ્નેક હિસ્સો), Amul (70%+ ડેરી હિસ્સો), Ramdev અને Badshah (50-60% મસાલા હિસ્સો) અને Atul Bakery (35-45% બેકરી હિસ્સો). વિતરકો મજબૂત સ્થાનિક બ્રાન્ડ ભાગીદારી વગર સધ્ધર સુરત કામગીરી બનાવી શકતા નથી.

સુરત વિતરકોને ડિજિટલ ઓર્ડર મેનેજમેન્ટ, ભીડભાડવાળી લેન માટે રૂટ ઓપ્ટિમાઇઝેશન, મલ્ટિ-બ્રાન્ડ પોર્ટફોલિયો માટે સ્કીમ ઓટોમેશન, e-invoicing સાથે GST-અનુપાલન બિલિંગ, બહુભાષી સપોર્ટ સાથે ફિલ્ડ ફોર્સ ટ્રેકિંગ અને ચોમાસાની આકસ્મિક રૂટિંગની જરૂર છે. સંપૂર્ણ DMS અપનાવવાથી વિતરકો 6-9 મહિનામાં સરેરાશથી ટોપ-ક્વાર્ટાઇલ પ્રદર્શન સુધી પહોંચે છે.

હા. SpireStock સુરતમાં જરૂરી તમામ વિતરણ વર્કફ્લોને સપોર્ટ કરે છે જેમાં મલ્ટિ-બ્રાન્ડ પોર્ટફોલિયો મેનેજમેન્ટ, ઉચ્ચ-ઘનતા ઝોન માટે રૂટ ઓપ્ટિમાઇઝેશન, સ્કીમ ઓટોમેશન, GST-અનુપાલન બિલિંગ, બહુભાષી મોબાઇલ એપ્સ અને રીઅલ-ટાઇમ એનાલિટિક્સ સામેલ છે. પ્લેટફોર્મ સુરતના અનન્ય પડકારોને હેન્ડલ કરે છે જેમાં ચોમાસામાં રીરૂટિંગ અને મલ્ટિ-પ્રાદેશિક SKU મેનેજમેન્ટ સામેલ છે.

સંબંધિત SpireStock ફીચર્સ

વાહનો અને ડ્રાઇવરો માટે રીઅલ-ટાઇમ GPS ટ્રેકિંગ સાથે ઝડપી ડિલિવરી માટે રૂટ ઑપ્ટિમાઇઝેશન.

ઝોન, ટાઉન અને રૂટ આધારિત ડિલિવરી મેનેજમેન્ટ ઓપ્ટિમાઇઝેશન સાથે.

વેચાણ વલણો, MIS રિપોર્ટ્સ અને વિતરણ એનાલિટિક્સ સાથે શક્તિશાળી ડેશબોર્ડ્સ.

લવચીક ઇન્સેન્ટિવ સ્કીમ્સ, ફ્લેટ, બલ્ક-પેક અને જથ્થાત્મક, આપમેળે લાગુ.

મલ્ટિ-લેવલ મંજૂરી વર્કફ્લો સાથે પ્લેસમેન્ટથી ડિલિવરી સુધી એન્ડ-ટુ-એન્ડ ઓર્ડર લાઇફસાયકલ.

સંબંધિત ઉદ્યોગો

સંબંધિત ઉકેલો

તમારા સંપૂર્ણ distributor નેટવર્કનું ડિજિટલ રીતે સંચાલન કરો. ઓનબોર્ડિંગ, ક્રેડિટ મર્યાદા, બાકી ટ્રેકિંગ અને પ્રદર્શન વિશ્લેષણ. મફત ટ્રાયલ શરૂ કરો.

તમારા રિટેલ નેટવર્કને ટ્રૅક અને મેનેજ કરો. આઉટલેટ્સ જિયો-ટેગ કરો, ગૌણ sales કેપ્ચર કરો, બીટ્સ મેનેજ કરો અને retailer પ્રદર્શન મોનિટર કરો.

ડેરી અને FMCG ડિલિવરી વાહનો માટે GPS ફ્લીટ ટ્રેકિંગ, ડ્રાઇવર મેનેજમેન્ટ અને રૂટ ઓપ્ટિમાઇઝેશન. ઇંધણ ખર્ચ 25% ઘટાડો. SpireStock અજમાવો.

સંબંધિત એન્ટિટીઝ

તમારા વિતરણને સુવ્યવસ્થિત કરવા તૈયાર છો?

તમારી 30 દિવસની મફત ટ્રાયલ શરૂ કરો અને જુઓ કે SpireStock તમારા ડેરી, FMCG અથવા ગ્રાહક વસ્તુ વિતરણને ઓર્ડરથી ક્રેટ રિકવરી સુધી કેવી રીતે બદલી શકે છે.

SpireStock Team

ડિસ્ટ્રિબ્યુશન ટેક્નોલોજી નિષ્ણાતો

SpireStock Team SpireStock માટે ડિસ્ટ્રિબ્યુશન મેનેજમેન્ટ, સપ્લાય-ચેઇન ઑપ્ટિમાઇઝેશન અને ભારતીય ડેરી અને FMCG બ્રાન્ડ્સ માટેના ફીલ્ડ ઑપરેશન્સ પર લખે છે.