Why Credit Management Is the Silent Killer of FMCG Profitability

Outstanding payments from distributors represent the single largest drain on working capital for Indian FMCG companies. A 2025 FICCI survey found that Indian FMCG brands have an average of 22-35% of their monthly distribution revenue locked in distributor outstanding at any given time. For a company doing Rs 100 crore in annual sales through distribution, that means Rs 6-10 crore in perpetual working capital lock-up, money that could be deployed for growth, inventory, or debt reduction.

The problem is not that distributors are unwilling to pay. Most distributors in cities like Mumbai, Delhi, Bangalore, and Hyderabad intend to settle on time. The problem is that manual credit management systems lack the real-time visibility, consistent enforcement, and proactive alerting needed to keep collections on track. When an ASM manually checks outstanding against a credit limit using yesterday's Tally printout, the data is already stale, and the decision is already compromised.

Types of Credit Limits in FMCG Distribution

Credit management in Indian FMCG distribution is not one-size-fits-all. Different brands and distributors use different credit structures depending on the relationship, volume, and risk profile. Here are the primary types:

- Fixed credit limit: A hard cap on total outstanding amount (e.g., Rs 5 lakh). Once the distributor's outstanding reaches Rs 5 lakh, no new orders are accepted until payments are made. Simple but inflexible.

- Revolving credit: A credit line that replenishes as payments come in. If the limit is Rs 10 lakh and Rs 3 lakh is outstanding, Rs 7 lakh is available for new orders. Most common in established relationships.

- Slab-based credit: Credit limit varies with monthly purchase volume. A distributor buying Rs 20 lakh per month gets Rs 8 lakh credit; buying Rs 50 lakh gets Rs 15 lakh credit. Incentivizes volume growth.

- Credit days: Instead of an amount cap, time-based limit (e.g., 15-day credit). All invoices must be settled within 15 days. Orders blocked if any invoice exceeds 15 days.

- Hybrid model: Combines amount and days. Credit limit of Rs 10 lakh AND 21-day credit period, whichever triggers first. This is the recommended approach for most Indian FMCG operations.

The billing and invoicing module in a modern DMS supports all these credit structures with configurable rules per distributor, per brand. The flexibility to apply different models to different distributors based on their risk profile is essential for managing a diverse network that spans from Rs 5 lakh monthly distributors in Lucknow to Rs 2 crore monthly super-stockists in Ahmedabad.

How Manual Credit Control Fails

In most Indian FMCG companies, credit control is supposed to work like this: the finance team sets a credit limit, the sales team checks the limit before booking an order, and orders exceeding the limit are blocked until payment is received. In practice, this process breaks down at every step.

The ASM Override Problem

Area Sales Managers (ASMs) are measured on sales targets. When a distributor is over their credit limit but wants to place a large order, the ASM has every incentive to push the order through. The override request goes to the regional manager, who also has a sales target to meet. Before you know it, overrides become the norm, not the exception. In some FMCG companies, 40-60% of orders involve credit limit overrides, rendering the entire credit control framework meaningless.

The damage compounds over time. Once a distributor learns that credit limits are routinely overridden, they lose the incentive to pay on time. A distributor who would naturally settle in 15 days starts stretching to 25-30 days because they know the supply will not stop. This behavioral shift across 200+ distributors can increase the company's overall DSO by 8-12 days, locking up crores in additional working capital.

Stale Data Problem

In manual systems, the credit limit check happens against the last known outstanding balance, which might be from the previous day's Tally closing or, worse, the previous week's statement. Payments received today are not reflected until the next data update. This lag means the sales team might block a distributor who has already paid, or worse, approve an order for a distributor who is actually over-limit. The stale data problem is particularly acute for dairy distributors who place orders daily.

Inconsistent Enforcement

Without a system that uniformly enforces credit rules, enforcement depends on individual ASMs. Some are strict, others are lenient. The result is an uneven credit landscape where disciplined distributors feel penalized while others exploit the system. This inconsistency erodes trust in the brand-distributor relationship. A distributor in Pune who always pays on time but sees a neighboring distributor getting unlimited supply despite chronic overdues will justifiably question the fairness of the arrangement.

Digital Credit Enforcement

A distribution management system transforms credit control from a manual, easily-overridden process to a systematic, real-time enforcement mechanism. Here is how each component works:

Hard-Stop Order Blocking

When a distributor's outstanding exceeds their credit limit, the system blocks new order placement at the source, whether through the mobile app, web portal, or even manual order entry. The block is automatic and cannot be bypassed by the salesman or delivery staff. Override authority is limited to specific roles (e.g., Regional Manager or Finance Head) with full audit trail capturing who approved the override, when, why, and for what amount.

This hard-stop mechanism changes behavior fundamentally. When distributors know that exceeding the credit limit will physically stop their next order, they prioritize payment. The psychological impact of a system-enforced block is far greater than a phone call from an ASM requesting payment.

Real-Time Outstanding Calculation

The system calculates outstanding in real time by combining: all unpaid invoices + dispatched-but-not-yet-invoiced goods + orders confirmed-but-not-yet-dispatched - payments received (including cheques in clearing) - credit notes approved. This gives a true real-time credit position, not a stale snapshot from yesterday's books.

For the calculation to be accurate, the system must capture every transaction as it happens. When a distributor makes a UPI payment at 10:30 AM, the credit limit should reflect this by 10:31 AM, allowing a blocked order to proceed. This real-time reflection is impossible in Tally-based workflows where data entry happens at end-of-day. The payment collection module integrates with banking systems to capture digital payments in near-real-time.

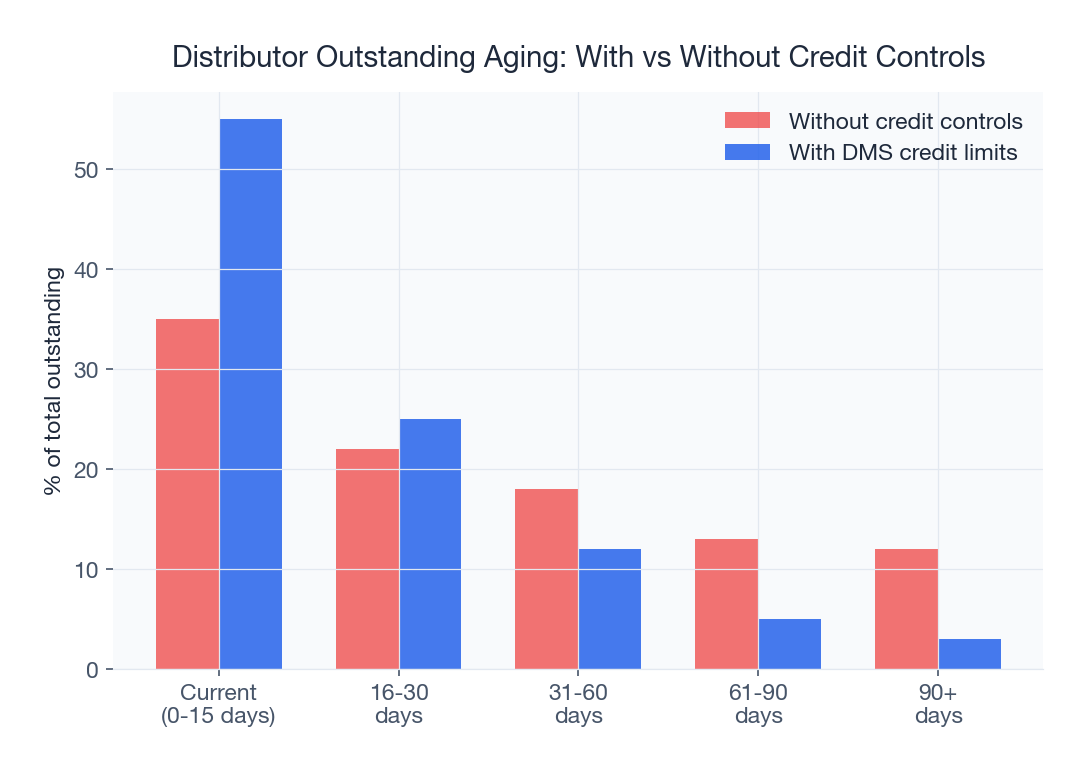

Automated Aging and Escalation

The analytics module generates aging buckets (0-7 days, 8-15 days, 16-30 days, 30+ days) and triggers automated escalation:

- At 80% credit utilization: SMS reminder to distributor with current outstanding and available limit

- At 100% utilization: Email alert to ASM with distributor details and aging breakdown

- At 110% (post-override): Alert to Regional Manager with override history and risk assessment

- At 120%: Auto-hold on all orders, escalation to Finance Head, distributor placed on "watch list"

- At 30+ days overdue: Automated demand notice generation, field collection task assigned

Each escalation step is documented for audit purposes and visible on the distributor's credit management dashboard.

Dynamic Credit Adjustment

Top-performing distributors who consistently pay on time and grow volumes deserve higher credit limits. The system can recommend credit limit increases based on payment history, purchase trends, and risk scoring. Conversely, distributors with deteriorating payment behavior trigger credit limit reduction recommendations. This dynamic approach replaces the annual credit review process that most FMCG companies follow with a continuous, data-driven credit optimization cycle.

Credit Scoring for Retailers and Sub-Stockists

Credit management extends beyond the brand-to-distributor relationship. Distributors themselves extend credit to retailers and sub-stockists, often informally. A distributor might have Rs 50 lakh outstanding from 500 retailers, with no systematic way to assess which retailers are creditworthy and which are risky.

A DMS-based credit scoring system for retailers considers:

| Scoring Factor | Weight | Data Source |

|---|---|---|

| Payment history (last 6 months) | 30% | Invoice and payment records |

| Order consistency | 20% | Order management data |

| Average payment days | 20% | Payment tracking module |

| Cheque bounce history | 15% | Banking reconciliation |

| Business vintage | 10% | Retailer master data |

| Market reputation | 5% | Salesman input via mobile app |

Retailers scoring above 80 get higher credit limits and longer payment windows. Those scoring below 50 are placed on cash-only or advance payment terms. This data-driven approach replaces the salesman's subjective judgment, which often favors friendly retailers over creditworthy ones. Our retailer tracking solution provides the data foundation for retailer credit scoring.

Manual vs Automated Credit Management

| Parameter | Manual/Tally | DMS-Automated |

|---|---|---|

| Outstanding data freshness | Previous day or older | Real-time (within minutes) |

| Order blocking | Manual check by ASM | Automatic hard-stop |

| Override tracking | No audit trail | Full audit trail with approval chain |

| Aging alerts | Monthly or quarterly review | Daily automated alerts |

| Payment reconciliation | Manual matching in Tally | Auto-matched with bank feeds |

| DSO visibility | Calculated quarterly in Excel | Real-time per distributor |

| Bad debt prevention | Reactive (after default) | Proactive (early warning signals) |

| Credit limit review | Annual or ad-hoc | Continuous dynamic scoring |

Working Capital Math: The Impact of Credit Control

Consider an FMCG company with Rs 80 crore annual distribution revenue and an average DSO (Days Sales Outstanding) of 28 days:

- Working capital locked: Rs 80 crore x (28/365) = Rs 6.14 crore

- If DSO reduced to 18 days: Rs 80 crore x (18/365) = Rs 3.95 crore

- Working capital freed: Rs 6.14 crore - Rs 3.95 crore = Rs 2.19 crore

- At 14% cost of capital: Annual saving of Rs 30.7 lakh in interest costs alone

For context, the annual cost of a DMS platform is typically Rs 3-8 lakh. The working capital benefit alone provides 4-10x ROI. Add reduced bad debt write-offs (typically Rs 10-30 lakh savings annually) and faster order-to-cash cycles, and the total ROI exceeds 8-15x. See our detailed guide on ROI calculation for distribution software.

Five DSO Improvement Strategies

- Real-time credit enforcement: Block orders when limits are breached, no exceptions without documented approval. This single change typically reduces DSO by 5-8 days within the first quarter.

- Payment-linked incentives: Early payment discounts (1-2% for payment within 7 days) funded by working capital savings. A 1% cash discount on a Rs 10 lakh invoice costs Rs 10,000 but saves Rs 4,000-6,000 in interest on working capital, with the balance justified by faster cash conversion.

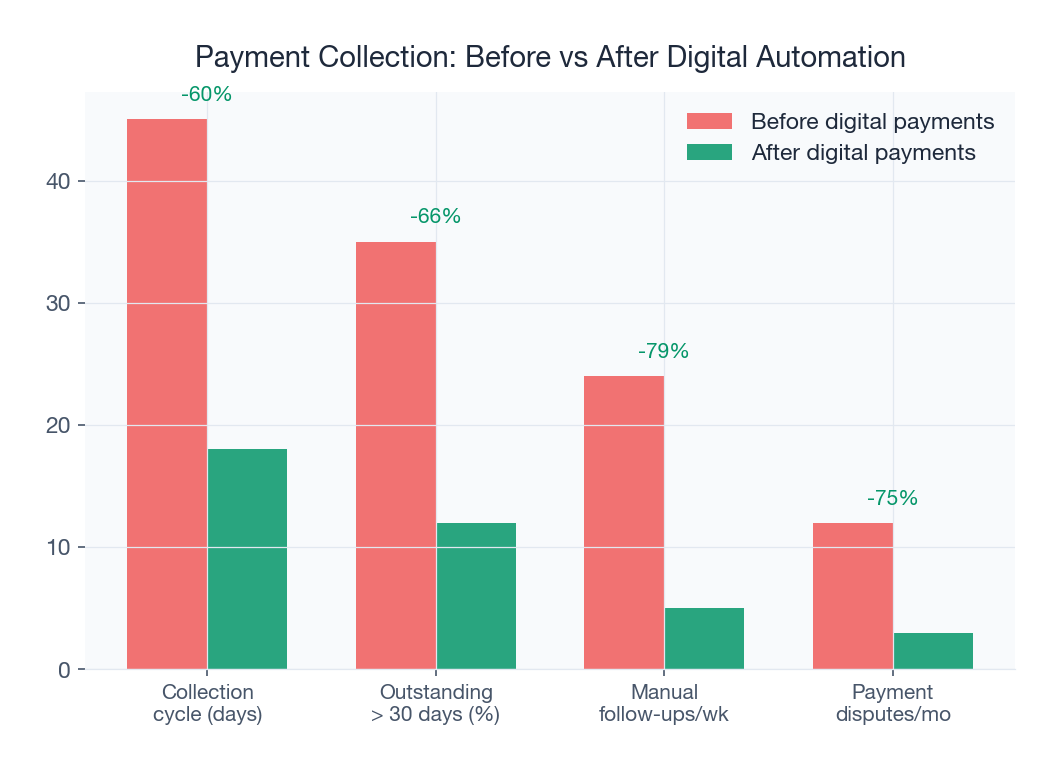

- Digital payment integration: UPI, NEFT, and RTGS payment tracking through the payment collection module. When distributors can see their outstanding and pay via UPI directly from the mobile app, payment friction drops significantly.

- Cheque-to-digital migration: Eliminate the 3-5 day float of cheque clearing by encouraging digital payments. Many distributors in Kolkata, Chennai, and other metros still pay by cheque out of habit rather than necessity. A small incentive for digital payment accelerates the transition.

- Weekly settlement rhythm: Move from monthly to weekly settlement cycles for high-volume distributors. This reduces average outstanding per distributor and creates a more predictable cash flow pattern for both parties.

Credit Management for Dairy Distribution

Dairy distribution presents unique credit challenges because of daily ordering cycles. A dairy distributor places orders every day, receives goods every day, and should ideally pay every day or every few days. The short shelf life of dairy products means the brand cannot afford to stop supply (products will spoil at the plant), but continuing to supply an over-limit distributor compounds the credit risk.

Effective credit management strategies specific to dairy distribution include:

- Daily credit limit recalculation: Unlike monthly FMCG products, dairy credit limits must refresh daily based on the previous day's deliveries and payments

- Perishable stock risk adjustment: Credit exposure includes the value of stock in the distributor's cold storage that could become worthless if the relationship deteriorates

- Auto-debit arrangements: Standing instructions for daily/weekly UPI auto-debit linked to delivery value

- Route-level collection: Delivery staff collect payments during the next day's delivery, reducing the payment cycle to 24-48 hours

For dairy-specific strategies, read our comprehensive guides on dairy distribution software and payment collection for dairy distributors.

Case Study: Ahmedabad FMCG Company

An FMCG brand operating through 180 distributors across Gujarat implemented SpireStock's credit management module. The company had a DSO of 34 days and Rs 4.2 crore locked in distributor outstanding. Credit limit overrides were running at 55% of all orders, meaning the credit control framework was effectively non-functional.

- DSO reduced from 34 days to 16 days within 6 months of implementation

- Outstanding reduced from Rs 4.2 crore to Rs 1.8 crore, freeing Rs 2.4 crore in working capital

- Credit limit overrides dropped from 55% of orders to 8%, with every override documented and approved at the appropriate level

- Bad debt write-offs reduced from Rs 18 lakh/year to Rs 2.5 lakh/year, a saving of Rs 15.5 lakh annually

- Distributor satisfaction improved because transparent, consistent rules replaced arbitrary enforcement

- Collection efficiency (payment within credit period) improved from 62% to 91%

Multi-Brand Credit Management: The Distributor's Perspective

For distributors handling 5-15 brands, credit management works in both directions: they receive credit from brands and extend credit to retailers. A multi-brand distributor in Surat might have Rs 15 lakh credit from Brand A, Rs 8 lakh from Brand B, and Rs 20 lakh from Brand C, while simultaneously extending Rs 50 lakh in aggregate credit to 300 retailers. The cash flow dynamics of this intermediary position require careful management.

When retailers delay payment, the distributor's credit utilization with brands increases. If the distributor gets blocked by Brand A due to outstanding exceeding the limit, but the underlying cause is retailers not paying for Brand A products, the problem requires retailer-level collection action, not just a payment to Brand A. A DMS that tracks outstanding at the retailer-brand level (how much each retailer owes for each brand's products) enables this level of root-cause analysis. The analytics module surfaces these insights in actionable dashboards that the distributor's collection team can act on daily.

Common Mistakes in Credit Management

- Setting credit limits too high: Being generous with credit to win distributors creates long-term working capital problems. Start at 50% of expected monthly purchases and increase based on performance.

- No periodic review: Credit limits set at onboarding and never revised based on actual performance. Market conditions change, distributor businesses grow or shrink, and credit limits must reflect current reality.

- Ignoring partial payments: Accepting partial payments without linking them to specific invoices creates reconciliation nightmares. Always apply payments against the oldest invoices first (FIFO payment application).

- Override without accountability: Allowing overrides without tracking who approved and why. Every override should require documented justification and be visible in reports.

- Punishing good distributors: Applying the same strict rules to consistently on-time payers and chronic defaulters. A tiered approach rewards good payment behavior with higher limits and more flexibility.

Explore our broader solutions for FMCG distribution and consumer goods distribution. Learn about distribution tracking and demand forecasting capabilities that complement credit management, and read our comparison of manual vs digital distribution to understand the full transformation potential.

Outstanding payments eating into your profitability? SpireStock's credit management module enforces limits in real time, reduces DSO by 30-50%, and frees crores in working capital. Start your free trial or view pricing to see the impact on your bottom line.

Sources & References

Frequently Asked Questions

Average DSO in Indian FMCG distribution ranges from 21-45 days depending on the category and region. Dairy distribution tends to have lower DSO (7-15 days) due to perishable products, while packaged foods and homecare have higher DSO (25-45 days). Best-in-class companies achieve DSO under 15 days with digital credit enforcement.

First, investigate the root cause. If the distributor has genuine cash flow issues, consider reducing the credit limit and increasing order frequency. If the distributor is growing rapidly, a credit limit increase may be justified. Use the DMS to track payment patterns and have a data-backed conversation. Never allow chronic over-limit operation without documented escalation.

The hybrid model (both amount and days) is recommended for most FMCG distributors. Credit limit alone does not prevent old invoices from lingering. Credit days alone does not prevent concentration risk. The hybrid triggers a block when either condition is breached, providing comprehensive protection.

Digital payment tracking (UPI, NEFT, RTGS) provides real-time payment visibility. When a distributor makes a payment via UPI, the DMS reflects it within minutes, immediately freeing up credit limit for new orders. Cheque payments have a 3-5 day clearing delay during which the credit limit remains consumed.

For a company with Rs 50-100 crore in distribution revenue, reducing DSO by 10 days frees Rs 1.5-3 crore in working capital. At 14% cost of capital, this saves Rs 20-40 lakh annually in interest costs. Add reduced bad debt write-offs (typically Rs 10-20 lakh savings) and the total ROI is 5-10x the software cost.

Start conservative. Set the initial credit limit at 50% of expected monthly purchases with a 15-day credit period. After 3 months of consistent on-time payments, increase to 75%. After 6 months, review and set the long-term limit based on actual performance. The DMS tracks payment history to make data-driven credit decisions.

Related SpireStock Features

GST-compliant invoicing with HSN codes, gate passes, and financial ledger.

Powerful dashboards with sales trends, MIS reports, and distribution analytics.

End-to-end order lifecycle from placement to delivery with multi-level approval workflows.

Related Industries

End-to-end dairy distribution software for milk, curd, paneer, and ghee brands. Manage orders, crates, cold chain, and GST billing in one platform.

Streamline FMCG distribution with order management, beat planning, retailer tracking, and GST billing. Built for Indian FMCG supply chains.

Distribution management for consumer goods brands. Manage distributors, retailers, schemes, and sales analytics across India. Start free trial.

Related Solutions

Track distributor and retailer payments. Cash, UPI, cheque collection with reconciliation, ageing reports, and credit limit management.

Manage your entire distributor network digitally. Onboarding, credit limits, outstanding tracking, and performance analytics. Start free trial.

Track and manage your retail network. Geo-tag outlets, capture secondary sales, manage beats, and monitor retailer performance. Try SpireStock.

Related Entities

Ready to Streamline Your Distribution?

Start your free 30-day trial and see how SpireStock can transform your dairy, FMCG or consumer-goods distribution operation, from order capture to crate recovery.

SpireStock Team

Distribution Technology Experts

SpireStock Team writes for SpireStock on distribution management, supply-chain optimisation and field operations for Indian dairy and FMCG brands.