The Quick Commerce Explosion in India

Between 2020 and 2026, India's quick commerce sector has undergone one of the most dramatic growth trajectories in the country's retail history. What began as a pandemic-era experiment in 10-minute grocery delivery has matured into a Rs 40,000+ crore industry that is fundamentally redrawing the FMCG distribution map. For distributors serving Mumbai, Delhi, Bangalore, and other metro cities, this is no longer a future threat -- it is the present reality.

Blinkit (formerly Grofers), backed by Zomato, now operates over 2,000 dark stores across India. Zepto, founded by two Stanford dropouts, has scaled to 1,000+ micro-warehouses and crossed $1 billion in annualized revenue. Swiggy Instamart operates 600+ dark stores. BigBasket, now owned by Tata, has integrated quick commerce into its existing grocery delivery model. Together, these platforms deliver everything from milk and bread to shampoo and snacks in 10-30 minutes, 18 hours a day, 7 days a week.

The numbers tell a story that every FMCG distributor needs to understand. According to RedSeer Consulting, India's quick commerce market grew from roughly Rs 5,000 crore in 2021 to over Rs 40,000 crore in 2026, an eightfold increase in just five years. More importantly, quick commerce now accounts for 60-75% of all online FMCG sales in India. In metro cities, it has moved from a convenience channel to a primary purchasing channel for millions of urban consumers.

| Platform | Dark Stores (Approx.) | Delivery Promise | Key FMCG Categories | Metro Penetration |

|---|---|---|---|---|

| Blinkit | 2,000+ | 10-15 minutes | Full grocery, personal care, beverages, snacks | 25+ cities |

| Zepto | 1,000+ | 10 minutes | Grocery, staples, packaged food, personal care | 15+ cities |

| Swiggy Instamart | 600+ | 15-20 minutes | Grocery, FMCG, household essentials | 20+ cities |

| BigBasket (Tata) | 400+ | 15-30 minutes | Full grocery range including fresh | 15+ cities |

What makes this growth particularly significant for traditional distributors is the consumer behavior shift behind it. NielsenIQ data shows that once a consumer makes their first quick commerce purchase, they increase order frequency rapidly -- from 2-3 orders per month in month one to 8-12 orders per month by month six. These are not incremental purchases. They are direct substitutions of trips to the kirana store.

A KPMG study estimated that in top-8 Indian metros, quick commerce has already captured 8-12% of total FMCG retail value -- and this share is growing at 40-50% year-on-year. For context, modern trade (supermarkets and hypermarkets) took 15 years to reach 10% share nationally. Quick commerce achieved comparable metro penetration in under five years.

How Quick Commerce Bypasses Traditional Distribution

To understand why quick commerce is so disruptive to FMCG distributors, you need to understand how its supply chain works -- because it fundamentally eliminates several layers of the traditional distribution pyramid.

The Traditional FMCG Distribution Flow

In the conventional model that has served India for decades, the supply chain looks like this: Manufacturer to Carrying and Forwarding Agent (CFA) to Distributor to Retailer (kirana store) to Consumer. Each layer adds cost, takes margin, and introduces delay. A product manufactured in Baddi, Himachal Pradesh by a company like Dabur or ITC passes through 3-4 intermediaries before reaching the consumer's hands in Mumbai or Delhi. The total channel margin -- from factory gate to consumer -- runs 25-40% of MRP.

The Quick Commerce Supply Chain

Quick commerce platforms have collapsed this chain into a dramatically simpler flow: Manufacturer (or large wholesaler) to Dark Store to Consumer. There is no CFA. There is no distributor. There is no retailer. The platform procures directly from the brand or its national stockist, stores inventory in hyperlocal dark stores (typically 2,000-4,000 sq ft warehouses), and delivers to the consumer via its own gig delivery fleet.

For FMCG brands, this direct-to-dark-store model is enormously attractive. Here is why:

- Better margins: By cutting out distributors and retailers, brands can offer platforms 15-25% trade margins while still retaining more per-unit profit than the traditional GT channel.

- Real-time data: Quick commerce platforms provide brands with granular, real-time data on consumer purchasing patterns, basket composition, price sensitivity, and demand trends -- data that the traditional distribution chain has never been able to deliver.

- Speed to market: A new product launch can be live on Blinkit in 48 hours. Through traditional distribution, the same launch takes 4-8 weeks to reach retail shelves across even a single city.

- Demand-driven stocking: Platforms use AI-driven demand forecasting to stock dark stores with exactly what local consumers want, reducing returns and expiry waste.

- Promotional precision: Brands can run hyper-targeted promotions (specific pin codes, specific times, specific consumer segments) that are impossible in general trade.

The "Missing Distributor" Problem

The core issue for traditional distributors is stark: in the quick commerce model, they simply do not exist. The distributor's traditional value -- warehousing, credit extension, last-mile delivery to retailers, relationship management, scheme execution -- is either replicated by the platform's technology or deemed unnecessary.

When a brand like Parle, Britannia, or Marico decides to allocate 15-20% of its urban volume to quick commerce platforms, that volume does not flow through its existing distributor network. It flows through a completely parallel supply chain. The distributor's monthly billing drops, but their fixed costs -- godown rent, vehicle EMIs, salesman salaries -- remain the same. This is the fundamental disruption.

Key insight: Quick commerce does not compete with distributors for the same consumer. It competes for the same brand volume. When Blinkit sells 10,000 units of a shampoo brand in Mumbai in a month, those are 10,000 units that did not flow through any distributor's books.

The Real Impact on Indian Distributors

The impact of quick commerce on FMCG distribution is not uniform. It varies dramatically by geography, category, and distributor capability. Understanding these nuances is critical for developing an effective response.

Volume Loss: The Numbers

Based on data from Kotak Institutional Equities and industry surveys, FMCG distributors in metro cities have experienced 10-25% volume loss in categories heavily served by quick commerce. The variation depends on:

| Factor | Low Impact (10-12%) | High Impact (20-25%) |

|---|---|---|

| City tier | Tier-2 cities (Jaipur, Lucknow, Indore) | Top-8 metros (Mumbai, Delhi, Bangalore, Hyderabad) |

| Territory type | Mixed residential-commercial areas | Dense residential neighborhoods, apartment complexes |

| Category | Staples, cooking oil, atta | Beverages, snacks, personal care, instant food |

| Retailer base | Traditional kiranas with loyal customer base | Convenience stores near tech parks, metro stations |

Urban vs. Rural: A Tale of Two Indias

The quick commerce impact is overwhelmingly concentrated in urban India. In Mumbai, Bangalore, and Delhi NCR, distributors report measurable volume declines in affected categories. But step outside the top 20 cities, and the picture changes entirely.

In tier-3 and tier-4 towns -- Ratlam, Bellary, Baramati, Siwan -- quick commerce is virtually nonexistent. These markets, home to over 600 million consumers, remain entirely dependent on traditional distribution. The economics of quick commerce (dark store infrastructure, delivery fleet, digital payment adoption) make it unviable in towns below 5-10 lakh population. Distributors operating in these markets have seen no volume impact from quick commerce, and likely will not for several years.

For distributors operating across mixed territories -- some urban beats affected, some rural beats untouched -- the net impact depends on their portfolio mix. A distributor with 70% of volume in Pune city and 30% in surrounding talukas will feel it differently than one with the reverse ratio.

Category-Wise Impact: Who Is Hit Hardest

Not all FMCG categories are equally affected. The impact correlates with three factors: purchase frequency, brand substitutability, and cold chain requirements.

- Most affected -- Beverages and snacks: These are impulse and convenience categories where quick commerce excels. Brands like PepsiCo, Coca-Cola, Haldiram's, and Lay's see significant volume flowing through dark stores. Beverage distributors in metros report 15-25% volume shifts.

- Highly affected -- Personal care and household: Shampoos, soaps, detergents, and household cleaners are heavily purchased on quick commerce. These are planned replenishment purchases that consumers increasingly schedule through apps rather than kirana visits.

- Moderately affected -- Packaged food and staples: Atta, oil, rice, and dal see some shift, but consumer price sensitivity and the need for larger pack sizes (5kg, 10kg) moderate the impact. Quick commerce works better for 500g-1kg packs.

- Least affected -- Dairy and fresh: This is where dairy distributors have a structural advantage. Fresh milk, curd, paneer, and other chilled dairy products require specialized cold chain infrastructure that quick commerce dark stores struggle to replicate at the consistency and scale of established dairy distribution networks. The daily subscription model for milk still flows overwhelmingly through traditional channels.

According to IBEF data, India's overall FMCG sector is valued at over $220 billion, with general trade still accounting for 65-70% of total sales. But the growth is happening disproportionately in digital channels. General trade growth has slowed to 4-6% annually, while quick commerce is growing at 40-50%. The structural shift is unmistakable, even if the absolute share remains in GT's favor for now.

Why Distributors Still Matter (And Will Continue To)

Amid the disruption narrative, it is easy to lose sight of a fundamental truth: traditional FMCG distribution in India is not going away. The reasons are structural, economic, and deeply embedded in how India shops.

12 Million Kirana Stores That Quick Commerce Cannot Reach

India has approximately 12-13 million kirana stores. Quick commerce currently serves consumers in 25-30 cities. Even within those cities, dark store coverage is limited to specific neighborhoods. The vast majority of India's retail infrastructure -- the millions of kiranas across tier-2, tier-3, tier-4 towns, and rural India -- will continue to depend on traditional distributors for the foreseeable future.

Consider the math: even if quick commerce reaches 100 cities (an ambitious target for the next 3-5 years), it would cover roughly 30-35% of India's urban population and less than 15% of the total population. The remaining 85% of consumers will buy their FMCG products from kirana stores served by distributors.

Credit Extension: The Invisible Backbone

One of the most underappreciated roles of the Indian FMCG distributor is credit extension. Distributors typically extend 7-21 days of credit to their retailers, enabling small shopkeepers to stock goods without upfront capital. This credit infrastructure -- estimated at Rs 2-3 lakh crore outstanding at any given time across India -- is what keeps millions of small retailers operational.

Quick commerce platforms do not extend credit to retailers (they have no retailers). They do not finance the working capital needs of India's vast informal retail network. Without distributors, the credit architecture that sustains kirana commerce would collapse, and no technology platform has offered a viable alternative at scale.

Relationship-Based Selling and Merchandising

Indian FMCG distribution runs on relationships. A distributor's salesman who visits a kirana store three times a week does not just take orders. He manages shelf placement, introduces new SKUs, handles complaints, collects payments, ensures scheme benefits are applied correctly, and serves as the human interface between a multinational brand and a family-owned shop. This relationship-based selling model drives 80% of new product trial in general trade.

Quick commerce replaces this with an algorithm. It works brilliantly for established, high-velocity SKUs. But for new product launches, niche brands, regional products, and categories that require consumer education (think health supplements, organic products, specialized baby care), the distributor's salesforce remains indispensable.

Cold Chain Expertise for Dairy and Perishables

India's dairy distribution network handles 500+ million litres of milk daily through a cold chain infrastructure built over decades. This includes insulated vehicles, refrigerated storage at distributor points, crate management systems, and early-morning delivery schedules calibrated to ensure freshness. Dairy distributors have invested crores in this infrastructure.

Quick commerce dark stores maintain some refrigeration, but their cold chain capabilities cannot match the depth and reliability of established dairy distribution networks, especially for products like loose curd, fresh paneer, flavored milk, and ice cream. This structural advantage means dairy distributors face the lowest disruption risk from quick commerce.

Physical Merchandising and Visibility

In a kirana store, shelf placement matters enormously. The distributor's salesman negotiates display positions, sets up standees and danglers, ensures products are visible and accessible. In quick commerce, visibility is algorithmic -- determined by ad spend and platform ranking. While large brands can afford to pay for digital visibility, the thousands of regional and mid-size brands that built their businesses through GT merchandising would lose their competitive advantage in a purely digital channel.

Five Strategies for Distributors to Compete in the Quick Commerce Era

Survival and growth for Indian FMCG distributors in the quick commerce era requires proactive adaptation, not passive resistance. Here are five actionable strategies that forward-thinking distributors are already implementing.

Strategy 1: Digitize Operations with a Distribution Management System

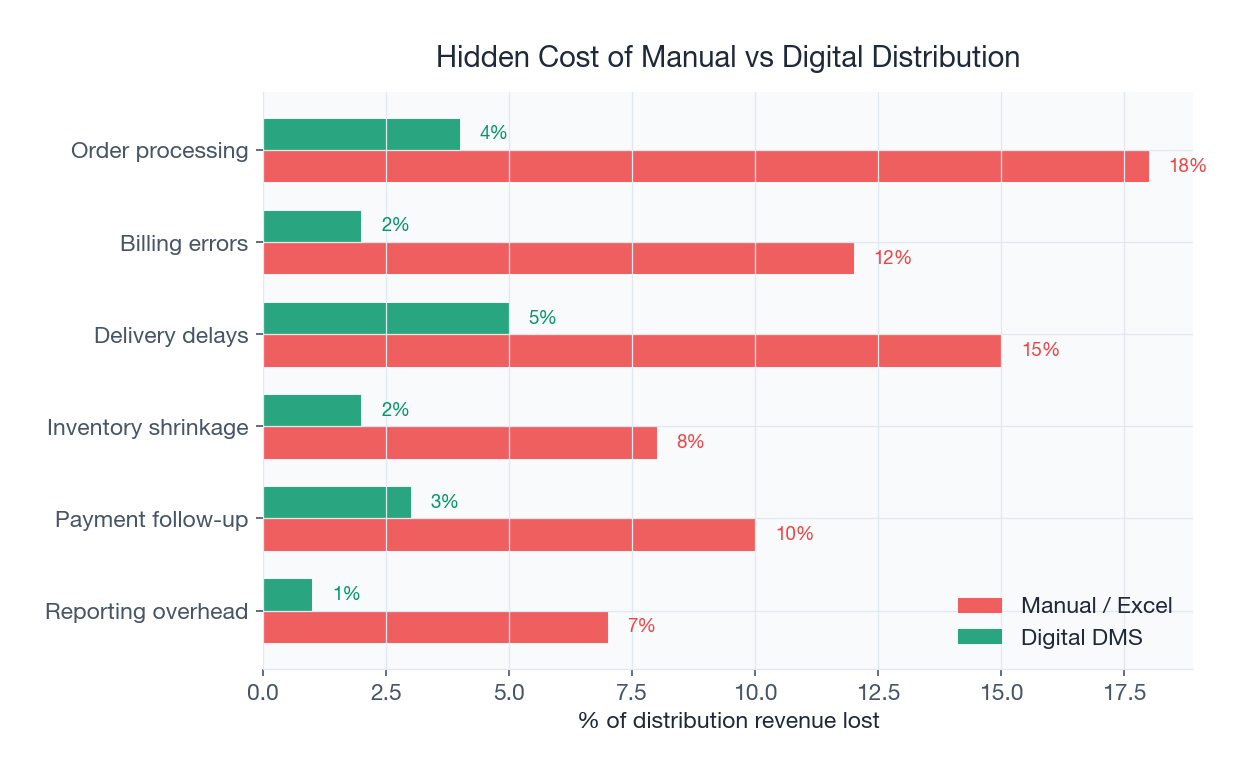

The single most important investment a distributor can make today is implementing a modern Distribution Management System (DMS). Quick commerce wins partly because of its technology backbone -- real-time inventory, data-driven stocking, automated operations. Distributors can close this technology gap by digitizing their own operations.

A comprehensive DMS like SpireStock provides:

- Digital order management: Replace phone calls and WhatsApp orders with a structured order management system that retailers can use from their smartphones. Faster ordering means more frequent ordering.

- Route optimization: AI-powered route planning reduces delivery costs by 20-30%, improving margins that are under pressure from volume loss.

- Real-time inventory visibility: Know exactly what is in stock, what is running low, and what needs reordering -- eliminating stockouts that push retailers to alternative sources.

- Sales analytics: Data dashboards that show SKU-wise performance, retailer ordering patterns, and territory trends help distributors make decisions with the same data-driven precision as quick commerce platforms.

- Scheme management: Automated scheme engines ensure retailers get their correct incentives instantly, building trust and loyalty.

The data is clear: digitized distributors retain retailers at 2-3x the rate of manual-operation distributors, because they offer a more reliable, transparent, and efficient service experience. Read our detailed guide on distribution management software in India for a comprehensive comparison of available solutions.

Strategy 2: Add Value Through Retailer Services

When quick commerce competes on speed-to-consumer, distributors need to compete on value-to-retailer. The distributors thriving in the quick commerce era are those who have evolved from mere product suppliers to full-service retail partners.

- Retailer credit scoring and management: Use DMS data to offer optimized credit terms based on each retailer's payment history. Good payers get extended credit; risky accounts get tighter terms. This data-driven approach, managed through retailer tracking systems, replaces the gut-feel credit decisions that lead to bad debts.

- Merchandising support: Help retailers optimize their shelf layout, manage product assortment, and improve their store's visual appeal. A well-merchandised kirana store attracts more foot traffic, which benefits both the retailer and the distributor.

- Digital enablement: Help your retailers get listed on Google Maps, set up digital payment acceptance, and even create simple online ordering for their walk-in customers. The more competitive your retailers are against quick commerce, the more volume they will pull through your distribution.

- Business advisory: Share anonymized category insights with retailers. "Stores your size in this area are selling 40% more beverages by stocking energy drinks" -- this kind of data-driven advice, drawn from your analytics platform, builds a relationship no algorithm can replace.

Strategy 3: Expand into Underserved Territories

While quick commerce platforms fight over the same 25-30 metro cities, vast swathes of India remain underserved by organized distribution. Tier-3 and tier-4 towns, semi-urban areas, and rural markets represent a massive growth opportunity for distributors willing to expand.

India has approximately 7,000+ towns with populations between 50,000 and 5 lakh. Most of these towns are served by fragmented, unorganized distribution networks. A digitized distributor with efficient route optimization, proper distribution tracking, and systematic retailer coverage can capture significant market share in these territories.

Brands are actively seeking distribution partners in these markets because quick commerce cannot serve them. ITC, Dabur, Marico, and other large FMCG companies have explicitly stated in analyst calls that they are investing in expanding their GT distribution depth in sub-lakh-population towns precisely because digital channels cannot reach these consumers.

Strategy 4: Become a Quick Commerce Fulfillment Partner

If you cannot beat them, join them -- but on your terms. Some forward-thinking distributors are repositioning themselves as fulfillment partners for quick commerce platforms rather than viewing them purely as competitors.

The opportunity works like this: quick commerce platforms need reliable local suppliers to stock their dark stores. Instead of always sourcing from large national wholesalers, many platforms are open to working with established local distributors who can ensure:

- Consistent stock availability with minimal stockouts

- Fast replenishment (multiple deliveries per day if needed)

- Freshness management for near-expiry products

- Returns handling and reverse logistics

- Local market knowledge on demand patterns

Distributors in Mumbai and Bangalore who have successfully become dark store suppliers report that while margins are thinner (5-8% vs. 8-12% in GT), the volume is consistent, payment is faster (7-15 days vs. 15-30 days in GT), and the operational overhead is lower (bulk delivery to a few dark stores vs. individual delivery to hundreds of retailers).

This strategy requires having the distribution tracking and inventory management infrastructure to meet platform SLAs. A DMS is essentially a prerequisite.

Strategy 5: Diversify Categories and Revenue Streams

Distributors who rely on a single brand or a narrow category are most vulnerable to quick commerce disruption. If your entire business is snacks distribution and 20% of that volume migrates to Blinkit, your margins may not survive.

Diversification strategies include:

- Add complementary categories: If you distribute beverages, add snacks and packaged foods. If you do dairy, add bakery products. Your route infrastructure and retailer relationships are already in place; additional categories are incremental revenue with minimal incremental cost.

- Regional and emerging brands: Quick commerce platforms prioritize high-velocity national brands. This creates an opening for distributors to become the go-to partner for regional and emerging brands that cannot afford quick commerce listing fees and need GT distribution to build their base.

- Private label and local products: Some distributors are developing private label products in categories like packaged water, cleaning supplies, and paper products. With existing retailer relationships and delivery infrastructure, private label can add 5-10% to margins.

- Value-added services: Offer retailers POSM (point of sale materials) management, return logistics, empty bottle/crate collection, and other services that brands will pay for. These service revenues are immune to quick commerce disruption.

How SpireStock Helps Distributors Stay Competitive

In the quick commerce era, the distributors who thrive will be those who match digital platforms in operational efficiency while leveraging their human advantages in relationship management and market reach. SpireStock is purpose-built for exactly this challenge.

Real-Time Data to Match Digital Platforms

Quick commerce platforms win partly because they operate on real-time data. SpireStock gives distributors the same advantage with real-time sales analytics that track every order, every delivery, every payment across your entire network. Know which SKUs are trending, which retailers are reducing orders (an early warning sign of volume leakage), and which territories need attention -- all from a single dashboard.

Stronger Retailer Relationships Through Transparency

When retailers can see their order history, pending credits, scheme benefits, and delivery status through a digital retailer portal, trust deepens. SpireStock's retailer-facing features transform the distributor-retailer relationship from transactional to partnership-based, creating switching costs that protect against both quick commerce pull and competitor push.

Route Efficiency That Protects Margins

With volumes under pressure, margins become critical. SpireStock's route optimization reduces fuel costs by 20-30% and increases drops per vehicle per day by 15-25%. For a distributor operating 10 vehicles across Delhi NCR, this translates to Rs 12-18 lakh in annual savings -- savings that directly offset any volume decline from quick commerce.

Scheme Transparency That Builds Trust

One of the biggest retailer complaints in traditional distribution is opacity around trade schemes. "Am I getting the right scheme benefit?" is a question that erodes trust. SpireStock's automated scheme engine applies correct incentives at the point of order, with full visibility for both the distributor and the retailer. When your retailers trust that they are getting fair treatment, they stay loyal even when quick commerce offers competitive pricing.

Ready to future-proof your distribution operations? Book a free demo to see how SpireStock equips distributors to compete effectively in the quick commerce era, or explore our pricing plans designed for distributors of every scale.

Case Studies: Distributors Who Adapted Successfully

Case Study 1: Sharma FMCG Distribution, Delhi NCR

Rajesh Sharma has been distributing packaged foods and personal care products across South Delhi and Faridabad for 14 years. By 2024, he was watching his monthly billing drop from Rs 85 lakh to Rs 68 lakh as retailers in residential areas reported losing customers to Blinkit and Zepto. Instead of cutting costs and accepting decline, Sharma invested in digitizing his operation.

He implemented SpireStock's distributor management platform, starting with digital order management for his 380 retailers. Within three months, order processing time dropped from 3 hours daily (phone calls and WhatsApp) to 40 minutes. He used the freed-up time to add a new snack brand to his portfolio and expanded into 45 new retailer outlets in areas of Faridabad that were previously underserved.

The result: within 8 months, his monthly billing recovered to Rs 82 lakh -- not by winning back volume lost to quick commerce, but by growing in categories and territories where quick commerce could not compete. His delivery cost per drop fell by 22% through route optimization, which more than compensated for the thinner margins on his expanded territory.

Case Study 2: Nandi Beverages, Bangalore

Nandi Beverages distributes soft drinks, packaged water, and energy drinks across East Bangalore, one of the most quick-commerce-saturated markets in India. Between 2023 and 2025, their beverage volume through kirana stores dropped 28% as consumers -- especially the tech workforce in Whitefield and Marathahalli -- shifted to ordering drinks on Zepto and Blinkit.

Nandi's response was twofold. First, they approached two quick commerce platforms about becoming a dark store supplier for their territory. Leveraging their existing cold storage infrastructure and fleet of insulated vehicles, they secured contracts to supply three Blinkit dark stores and two Zepto warehouses. This "if you can't beat them, supply them" approach recovered 60% of their lost volume, albeit at lower margins.

Second, they used SpireStock's analytics platform to identify their strongest-performing kirana segments -- roadside tea stalls, office canteens, and gym/fitness centers -- that were largely immune to quick commerce substitution. They doubled down on these segments, adding bulk water and health drinks to their portfolio. Combined, these strategies brought Nandi's total revenue 8% above their pre-disruption baseline.

Case Study 3: Patil Distribution Network, Pune

The Patil family has operated a multi-brand FMCG distribution business across Pune and Pimpri-Chinchwad for 22 years. With six major brand principals and 620 active retail outlets, they were one of the larger general trade distributors in western Maharashtra. Quick commerce impact on their business was moderate (12% volume loss in personal care, 8% in snacks) but the trend line was worrying.

Rather than viewing quick commerce purely as a threat, the Patils repositioned their business as a "distribution-as-a-service" platform. Using SpireStock's sales productivity tools and distribution tracking, they built a pitch to three emerging D2C brands that needed offline distribution but lacked the network. By offering these brands ready-made access to 620 retailers with digital ordering, route-optimized delivery, and real-time sales tracking, the Patils signed three new brand principals within six months.

Their insight was critical: as large brands shift volume to quick commerce, emerging brands need distributors more than ever. The distributor who can offer data-driven, digitized distribution services becomes the preferred partner for the next generation of FMCG brands.

What Leading FMCG Brands Are Doing: The Hybrid Distribution Model

While the quick commerce narrative often positions brands as abandoning traditional distribution, the reality is more nuanced. Leading Indian FMCG companies are recognizing that quick commerce and general trade serve different consumer needs, and both channels are essential for national coverage.

ITC: Investing in GT Depth

ITC, one of India's largest FMCG conglomerates, has been explicit about its commitment to general trade even as it grows its digital commerce presence. In its 2025 annual report, ITC noted that it expanded its direct distribution reach to 30+ lakh retail outlets, a 15% increase over the previous year. The company has invested in equipping its distributors with digital tools and has introduced channel-exclusive SKUs to prevent price conflict between GT and quick commerce.

ITC's strategy is instructive: use quick commerce for urban convenience categories (snacks, instant foods, personal care) while strengthening GT distribution for its broader portfolio (atta, spices, biscuits, stationery) across India's depth markets.

Dabur: Reconnecting with Kiranas

Dabur launched a "Kirana Mitra" (Friend of Kirana) program in 2024, equipping its distributors with digital ordering tools and offering kirana store owners training on category management, display optimization, and digital payments. According to Business Standard, Dabur's program reached 5 lakh kirana stores in its first year and contributed to a 7% increase in GT sell-through rates.

The program explicitly acknowledged that kiranas were feeling threatened by quick commerce and positioned Dabur as an ally in their survival. By helping kiranas become more competitive, Dabur ensured that its GT distribution network -- which still delivers 62% of its revenue -- remained strong.

Marico: The Hybrid Model Pioneer

Marico has been perhaps the most thoughtful about building a hybrid distribution model. The company routes its fast-moving urban SKUs (Saffola oils, Parachute coconut oil in small packs) through quick commerce while keeping its deeper portfolio (hair oils, value packs, rural-focused products) exclusively in GT. Crucially, Marico ensures that its distributors receive compensation for brand-building in territories where quick commerce also operates, recognizing that GT visibility drives awareness that benefits all channels.

What This Means for Distributors

The message from these brand strategies is clear: FMCG companies are not abandoning distributors -- they are reconfiguring the distributor's role. Distributors who position themselves as digitally capable, data-driven, and willing to evolve will retain and grow their brand partnerships. Those who resist change risk being replaced as brands consolidate their GT networks around fewer, stronger distributors.

The Future: Coexistence of Quick Commerce and Traditional Distribution

The question for Indian FMCG distribution is not whether quick commerce or traditional distribution will "win." Both will coexist, serving different consumer segments, different geographies, and different purchase occasions. The future is hybrid, and understanding how this hybrid market will evolve is essential for strategic planning.

The Segmented Market of 2026 and Beyond

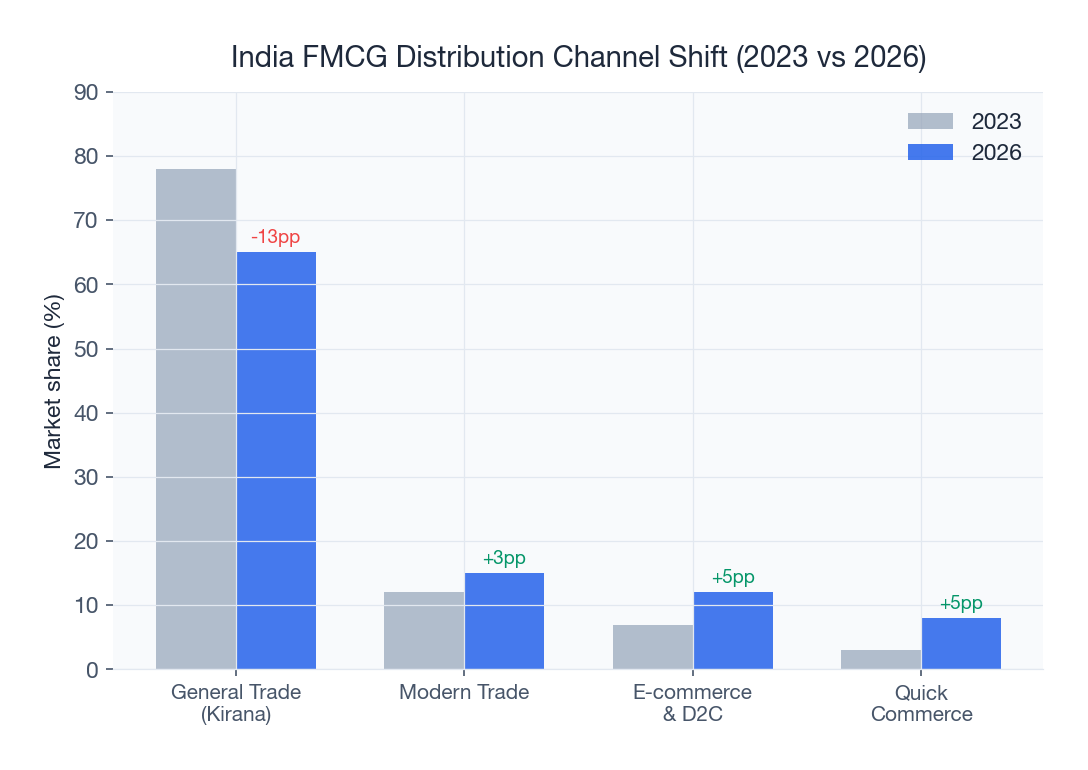

By 2028-2030, the Indian FMCG distribution landscape will likely settle into a clear segmentation:

- Quick commerce (15-20% of total FMCG): Dominant in top-30 cities for convenience, impulse, and replenishment purchases. High-velocity national brands, premium products, and small pack sizes.

- E-commerce/marketplace (8-10% of total FMCG): Bulk purchases, value packs, niche and specialty products. Amazon, Flipkart, and brand D2C websites.

- Modern trade (12-15% of total FMCG): Weekly/monthly stock-up shopping, promotions, and fresh produce. D-Mart, Reliance Retail, Star Bazaar.

- General trade via distributors (55-65% of total FMCG): Daily needs, credit-based purchasing, relationship selling, regional products, and the entire rural and semi-urban market. This is where 12 million kirana stores and hundreds of thousands of distributors will continue to operate.

The key insight is that even in the most optimistic projections for digital commerce, general trade will retain a majority share of Indian FMCG sales through the end of this decade. The channel will shrink in relative terms (from 80% to 55-65%), but absolute GT volumes will continue to grow as India's total FMCG market expands from $220 billion to $350+ billion.

The Distributor of the Future

The FMCG distributor of 2030 will look quite different from the distributor of 2020. Here is what will define the successful distributor:

- Technology-first operations: Every order digital, every delivery tracked, every payment recorded. The distributor's DMS will be as sophisticated as any quick commerce platform's backend.

- Data-driven decision making: Using analytics to optimize product mix, territory coverage, and retailer engagement -- not relying on gut feel and historical patterns.

- Multi-channel capability: Serving both traditional retailers and potentially quick commerce dark stores, modern trade outlets, and institutional customers through the same infrastructure.

- Value-added services: Moving beyond product distribution to offer retailers credit management, merchandising support, digital enablement, and business advisory.

- Portfolio diversification: Handling 5-8 brand principals across complementary categories, reducing dependence on any single brand's channel decisions.

Key insight: The distributors who will thrive in the next decade are not those who resist quick commerce, but those who learn from it. Adopt the technology, embrace the data, improve the efficiency -- and combine it with the human relationships, credit infrastructure, and market depth that no platform can replicate.

The disruption is real, but so is the opportunity. India's FMCG market is growing fast enough to accommodate both quick commerce and traditional distribution. The distributors who adapt, digitize, and evolve will not just survive -- they will capture a disproportionate share of the growth that lies ahead.

Ready to build a future-proof distribution business? Talk to our distribution technology experts to understand how SpireStock can help you compete and grow in the quick commerce era. Or explore our pricing plans to get started today.

Sources & References

- RedSeer Consulting, India Quick Commerce Market Sizing Report 2025-26

- Kotak Institutional Equities, FMCG Distribution Disruption: Quick Commerce Impact Assessment

- NielsenIQ, India FMCG Channel Share and Consumer Behavior Shifts 2025

- IBEF, FMCG Sector Overview: India Brand Equity Foundation

- Business Standard, FMCG Brands Reconnect with Kirana Stores Amid Quick Commerce Rise

Frequently Asked Questions

Quick commerce platforms like Blinkit, Zepto, and Swiggy Instamart bypass traditional distributors entirely by sourcing directly from manufacturers and delivering to consumers from dark stores. FMCG distributors in metro cities have experienced 10-25% volume loss in categories like beverages, snacks, and personal care, with the highest impact in dense residential neighborhoods.

Beverages and snacks are most affected (15-25% volume shift in metros), followed by personal care and household products. Packaged food and staples see moderate impact. Dairy and fresh products are least affected because quick commerce dark stores cannot match the cold chain infrastructure of established dairy distribution networks.

No. Quick commerce is viable only in 25-30 Indian cities and cannot reach the 12 million kirana stores across tier-2, tier-3, and rural India. Even by 2030, general trade is projected to retain 55-65% of total FMCG sales. Traditional distributors remain essential for credit extension, relationship selling, and market depth.

Five key strategies: (1) Digitize operations with a Distribution Management System for real-time data and efficiency, (2) Add value through retailer services like credit management and merchandising support, (3) Expand into underserved tier-3 and tier-4 territories, (4) Become a dark store fulfillment partner for quick commerce platforms, (5) Diversify product categories and revenue streams.

India's quick commerce market has grown from approximately Rs 5,000 crore in 2021 to over Rs 40,000 crore in 2026, an eightfold increase. Quick commerce now accounts for 60-75% of all online FMCG sales in India and 8-12% of total FMCG retail value in top-8 metro cities.

Yes, some distributors are successfully repositioning as dark store fulfillment partners. By leveraging existing warehousing, cold storage, and fleet infrastructure, distributors can supply quick commerce platforms with consistent stock availability and fast replenishment. Margins are thinner (5-8% vs. 8-12% in GT) but volume is consistent and payments are faster.

No. Leading brands like ITC, Dabur, and Marico are adopting hybrid distribution models. They use quick commerce for urban convenience categories while strengthening GT distribution for their broader portfolio. Brands are investing in distributor digitization and expanding GT reach in sub-lakh-population towns where quick commerce cannot operate.

A Distribution Management System gives distributors technology parity with quick commerce platforms: real-time sales analytics, digital order management, route optimization (20-30% cost reduction), automated scheme management, and retailer tracking. Digitized distributors retain retailers at 2-3x the rate of manual-operation distributors.

Related SpireStock Features

End-to-end order lifecycle from placement to delivery with multi-level approval workflows.

Zone, town, and route-based delivery management with optimization.

Powerful dashboards with sales trends, MIS reports, and distribution analytics.

Real-time GPS tracking of vehicles and drivers with route optimization for faster deliveries.

Flexible incentive schemes, flat, bulk-pack, and quantitative, applied automatically.

Related Industries

Streamline FMCG distribution with order management, beat planning, retailer tracking, and GST billing. Built for Indian FMCG supply chains.

Manage beverage distribution with cold chain tracking, crate management, route optimization, and real-time delivery monitoring. Try SpireStock free.

End-to-end dairy distribution software for milk, curd, paneer, and ghee brands. Manage orders, crates, cold chain, and GST billing in one platform.

Related Solutions

Manage your entire distributor network digitally. Onboarding, credit limits, outstanding tracking, and performance analytics. Start free trial.

Track and manage your retail network. Geo-tag outlets, capture secondary sales, manage beats, and monitor retailer performance. Try SpireStock.

Boost field sales team productivity with beat planning, GPS attendance, order capture, and performance analytics. Built for Indian FMCG teams.

Related Entities

Ready to Streamline Your Distribution?

Start your free 30-day trial and see how SpireStock can transform your dairy, FMCG or consumer-goods distribution operation, from order capture to crate recovery.

SpireStock Team

Distribution Technology Experts

SpireStock Team writes for SpireStock on distribution management, supply-chain optimisation and field operations for Indian dairy and FMCG brands.