ભારતીય FMCG માં સિંગલ-ચેનલ વિતરણનો અંત

દાયકાઓ સુધી, ભારતીય FMCG વિતરણ સીધું હતું: ઉત્પાદન કરો, C&F એજન્ટોને મોકલો, વિતરકોને પહોંચાડો અને સેલ્સમેનને kirana stores આવરી લેવા દો. General trade (GT) FMCG વેચાણના 90% થી વધુ હિસ્સો ધરાવતું હતું, અને વિતરકનું એકમાત્ર કામ તેના વિસ્તારના kiranas ને સારી રીતે સ્ટોક રાખવાનું હતું. તે દુનિયા હવે અસ્તિત્વમાં નથી.

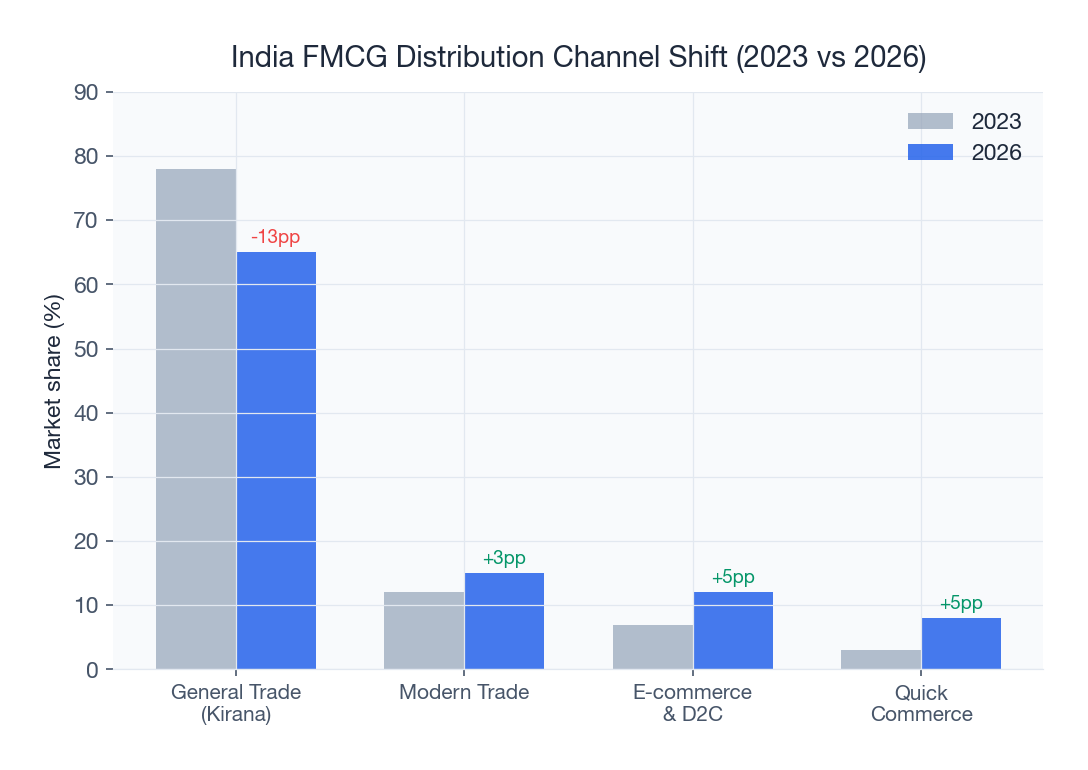

2026 ની શરૂઆત સુધીમાં, ભારતીય FMCG વેચાણ ઓછામાં ઓછી ચાર અલગ ચેનલો દ્વારા વહે છે — general trade (હજુ પણ આશરે 65-68% વેચાણ સાથે પ્રબળ), modern trade (DMart, Reliance Retail, BigBazaar અનુગામીઓ દ્વારા 12-15%), direct-to-consumer અથવા D2C (5-7% અને વાર્ષિક 30%+ વૃદ્ધિ) અને quick commerce (Blinkit, Zepto, Swiggy Instamart અને BigBasket દ્વારા 8-10%). દરેક ચેનલમાં અલગ અર્થશાસ્ત્ર, અલગ ચુકવણી ચક્ર, અલગ ઓર્ડર પેટર્ન અને અલગ માર્જિન માળખું છે.

FMCG વિતરક માટે, આ મલ્ટિ-ચેનલ વાસ્તવિકતા મૂળભૂત પડકાર સર્જે છે: તમે સ્પર્ધાત્મક — ક્યારેક વિરોધાભાસી — માંગ ધરાવતી ચેનલોમાં ઇન્વેન્ટરી, કિંમત, schemes અને સેલ્સ ટીમોનું સંચાલન કેવી રીતે કરો છો? જવાબ એકીકૃત ટેકનોલોજી દ્વારા સંચાલિત ઓમ્નિચેનલ વિતરણ વ્યૂહરચનામાં છે. એકીકૃત order management system વિના, વિતરકો અરાજકતાનો સામનો કરે છે — એક ચેનલમાં ઓવરસપ્લાય, બીજામાં stockouts અને બધામાં માર્જિન ધોવાણ.

ચેનલ અર્થશાસ્ત્ર: દરેક વિતરકે જાણવા જરૂરી નંબરો

ઓમ્નિચેનલ વ્યૂહરચના ઘડતા પહેલા, તમારે દરેક ચેનલના અર્થશાસ્ત્રને સમજવું જોઈએ. તફાવતો સ્પષ્ટ છે અને નફાકારકતા પર સીધી અસર કરે છે.

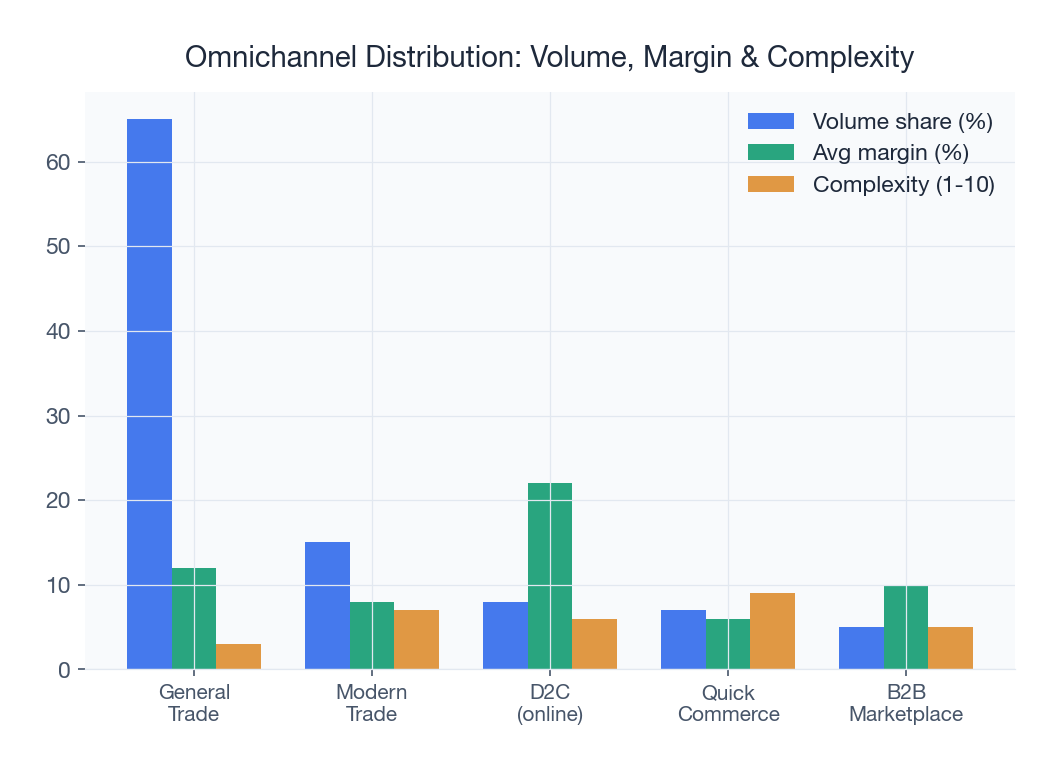

| પેરામીટર | General Trade (GT) | Modern Trade (MT) | D2C (Own/Marketplace) | Quick Commerce |

|---|---|---|---|---|

| વિતરક માર્જિન | MRP પર 3.5-8% | MRP પર 1-3% | લાગુ નથી (બ્રાન્ડ સીધો) | MRP પર 2-5% |

| ચુકવણીની શરતો | 7-21 દિવસ (ઘણીવાર વિલંબિત) | 30-60 દિવસ | ગ્રાહક દ્વારા પ્રીપેઇડ | 15-30 દિવસ |

| સરેરાશ ઓર્ડર મૂલ્ય | ₹2,000-₹8,000 | ₹50,000-₹5,00,000 | ₹400-₹1,200 | ₹200-₹600 |

| ઓર્ડર આવૃત્તિ | દર રિટેલર સાપ્તાહિક | સાપ્તાહિક/પખવાડિક | માંગ પર, વ્યક્તિગત | દૈનિક, નાના બેચ |

| રિટર્ન/ડેમેજ દર | 1-3% | 3-5% | 8-15% (ખાસ કરીને ખોરાક) | 2-4% |

| Scheme/પ્રમોશન ખર્ચ | વેચાણના 5-10% | વેચાણના 12-20% | 15-30% (ગ્રાહક સંપાદન) | 10-18% (પ્લેટફોર્મ ફી + પ્રમોઝ) |

| ડિલિવરી લોજિસ્ટિક્સ | વિતરક દ્વારા સંચાલિત | વિતરકથી DC | 3PL અથવા બ્રાન્ડ લોજિસ્ટિક્સ | Dark store પુનઃપૂર્તિ |

| ટેકનોલોજી પર નિર્ભરતા | નીચી-મધ્યમ | ઉચ્ચ (EDI એકીકરણ) | ખૂબ જ ઉચ્ચ | ખૂબ જ ઉચ્ચ (API-આધારિત) |

મુખ્ય સમજ: જ્યારે GT વિતરકો માટે શ્રેષ્ઠ માર્જિન અને સૌથી ઓછી જટિલતા આપે છે, સૌથી ઝડપથી વિકસતી ચેનલો — D2C અને quick commerce — સૌથી વધુ ટેકનોલોજી-સઘન પણ છે. જે વિતરકો આ ચેનલોને અવગણે છે તેઓ ગ્રાહક ખરીદી બદલાતા વોલ્યુમ ગુમાવવાનું જોખમ રાખે છે, પરંતુ જે અપૂર્ણ રીતે પ્રવેશે છે તેઓ માર્જિન સંકોચનનો સામનો કરશે.

શા માટે ચેનલ સંઘર્ષ વિતરકો માટે સૌથી મોટો ખતરો છે

મલ્ટિ-ચેનલ વિતરણનું સૌથી ખતરનાક પરિણામ ચેનલ સંઘર્ષ છે. જ્યારે સમાન ઉત્પાદન વિવિધ ચેનલોમાં વિવિધ કિંમતો અથવા વિવિધ schemes સાથે ઉપલબ્ધ હોય, ત્યારે તે કિંમત આર્બિટ્રેજ બનાવે છે જે સમગ્ર નેટવર્કમાં વિશ્વાસ અને માર્જિનને નુકસાન પહોંચાડે છે.

ભારતીય FMCG માં સામાન્ય ચેનલ સંઘર્ષ દૃશ્યો

- કિંમત અંડરકટિંગ: બ્રાન્ડ તેની D2C વેબસાઇટ પર પ્રતિ યુનિટ ₹10 છૂટ આપે છે જે kirana રિટેલર મેચ કરી શકતો નથી, ગ્રાહકોને general trade થી દૂર લઈ જાય છે

- Scheme સ્ટેકિંગ: Quick commerce પ્લેટફોર્મ "buy 2 get 1 free" ઓફર ચલાવે છે જે વિતરકની હાલની GT scheme સાથે વિરોધાભાસી છે, રિટેલર્સ અને ગ્રાહકોને ગૂંચવણમાં મૂકે છે

- ટેરિટરી ઓવરલેપ: Modern trade ચેઇન C&F એજન્ટ પાસેથી સીધો સ્ત્રોત મેળવે છે, સ્થાનિક વિતરકને બાયપાસ કરે છે, પરંતુ વિતરક પાસેથી રિટર્ન અને રિપ્લેસમેન્ટ સંભાળવાની અપેક્ષા રાખે છે

- Dark store cannibalisation: મુંબઈ અથવા બેંગલુરુ માં Blinkit dark store સ્થાનિક વિતરક જેવા જ pin codes ની સેવા આપે છે, અસરકારક રીતે સમાન ગ્રાહક માંગને બે ચેનલોમાં વિભાજિત કરે છે

આ સંઘર્ષોનું સંચાલન કરવા માટે બધી ચેનલોમાં કિંમત, ઇન્વેન્ટરી અને scheme અમલીકરણમાં રીઅલ-ટાઈમ દૃશ્યતા જરૂરી છે. અહીં distribution channel conflict management કાર્યકારી પછીના વિચાર કરતાં વ્યૂહાત્મક પ્રાથમિકતા બને છે. મજબૂત sales analytics સંઘર્ષને વહેલા ઓળખવા અને વિતરક અર્થશાસ્ત્ર પર તેની અસરને માપવા માટે આવશ્યક છે.

ઓમ્નિચેનલ વિતરણ વ્યૂહરચના બનાવવી: એક ફ્રેમવર્ક

અસરકારક ઓમ્નિચેનલ વ્યૂહરચનાનો અર્થ બધી ચેનલોને સમાન રીતે વર્તવાનો નથી. તેનો અર્થ દરેક ચેનલના વ્યૂહાત્મક મૂલ્ય અને અર્થશાસ્ત્રના આધારે — ઇન્વેન્ટરી, માનવબળ, મૂડી — સંસાધનોને ઇરાદાપૂર્વક ફાળવવાનો છે.

પગલું 1: ચેનલ પોર્ટફોલિયો મૂલ્યાંકન

દરેક ચેનલને બે અક્ષો પર મેપ કરો: આવકમાં વર્તમાન યોગદાન અને વૃદ્ધિ માર્ગ. 2026 માં મોટાભાગના ભારતીય FMCG વિતરકો માટે, પોર્ટફોલિયો આ રીતે દેખાય છે:

- General Trade: ઉચ્ચ આવક, સપાટથી લઈને નીચા સિંગલ-ડિજિટ વૃદ્ધિ. cash cow જે બધું જ ભંડોળ આપે છે

- Modern Trade: મધ્યમ આવક, મધ્યમ વૃદ્ધિ. લાંબા ચુકવણી ચક્રને કારણે ઉચ્ચ કાર્યકારી મૂડી જરૂરી છે

- Quick Commerce: નીચીથી મધ્યમ આવક, 40-60% વાર્ષિક વૃદ્ધિ. શહેરી FMCG માટે ભવિષ્યનું યુદ્ધભૂમિ

- D2C: વિતરકો માટે નીચી આવક (મોટેભાગે બ્રાન્ડ-સીધો), પરંતુ ગ્રાહક પસંદગીઓને પ્રભાવિત કરે છે જે GT માંગમાં ટપકે છે

પગલું 2: ચેનલ દ્વારા ઇન્વેન્ટરી ફાળવણી

સૌથી સામાન્ય ઓમ્નિચેનલ નિષ્ફળતા એ બધી ચેનલો માટે એક અવિભાજિત ઇન્વેન્ટરી પૂલ ચલાવવી છે. દરેક ચેનલમાં અલગ માંગ પેટર્ન છે:

- GT ઇન્વેન્ટરી: સ્થિર સાપ્તાહિક પુનઃપૂર્તિ, ઐતિહાસિક ડેટા પર આધારિત આગાહી કરી શકાય તેવી માંગ, 15-20 દિવસનો સેફ્ટી સ્ટોક

- MT ઇન્વેન્ટરી: પ્રમોશનલ કેલેન્ડર દ્વારા ચાલતી અસમાન માંગ, લાંબા lead times ને કારણે 25-30 દિવસનો સેફ્ટી સ્ટોક જરૂરી

- Quick commerce ઇન્વેન્ટરી: અત્યંત અસ્થિર, એપ-વ્યાપી સેલ ઇવેન્ટ્સ દરમિયાન સ્પાઇકિંગ; 3-5 દિવસના બફર સ્ટોક સાથે dark stores માટે દૈનિક પુનઃપૂર્તિ જરૂરી

જે વિતરકો દિલ્હી, પુણે અને હૈદરાબાદ જેવા શહેરોમાં કાર્યરત છે — જ્યાં ચારેય ચેનલો સક્રિય છે — તેમને એક જ ડેશબોર્ડ પરથી ચેનલ-વિશિષ્ટ ઇન્વેન્ટરી પૂલનું સંચાલન કરવા માટે multi-tenant workspace ક્ષમતા જરૂરી છે.

પગલું 3: કિંમત અને Scheme સંવાદિતા

એક કિંમત શાસન ફ્રેમવર્ક સ્થાપિત કરો જે ચેનલ સંઘર્ષને અટકાવે:

- Minimum Advertised Price (MAP) નીતિ: કિંમત યુદ્ધો રોકવા માટે બધી ચેનલોએ વ્યાખ્યાયિત લઘુત્તમ કિંમતે અથવા તેનાથી વધુ વેચવું જોઈએ

- ચેનલ-વિશિષ્ટ SKUs: વિવિધ ચેનલો માટે વિવિધ pack sizes અથવા bundles ઓફર કરો. GT માટે 500g pack, MT માટે 1kg value pack, D2C માટે combo pack

- એકીકૃત scheme engine: ચેનલોમાં schemes વ્યાખ્યાયિત અને લાગુ કરવા માટે કેન્દ્રિત સિસ્ટમનો ઉપયોગ કરો, કોઈ ઓવરલેપ અથવા સંઘર્ષ ન થાય તેની ખાતરી કરો. SpireStock નું scheme engine ચોક્કસપણે આ પડકાર માટે રચાયેલ છે

- રીઅલ-ટાઈમ કિંમત મોનિટરિંગ: અનધિકૃત ડિસ્કાઉન્ટિંગ શોધવા માટે ચેનલો અને માર્કેટપ્લેસમાં સ્પર્ધક અને પોતાની બ્રાન્ડની કિંમતને ટ્રેક કરો

પગલું 4: એકીકૃત ઓર્ડર સંચાલન

ઓમ્નિચેનલ વિતરણનો આધારશિલા એક જ order management system છે જે બધી ચેનલોમાંથી ઓર્ડર પ્રક્રિયા કરે છે. તેના વિના, વિતરકો ચાર અલગ-અલગ વર્કફ્લો સાથે ચાર અલગ વ્યવસાયોનું સંચાલન કરે છે — કાર્યકારી જટિલતા અને ભૂલ દરને ચતુર્ગુણ કરે છે.

એક એકીકૃત સિસ્ટમ સક્ષમ કરે છે:

- એક જ ઇન્વેન્ટરી દૃશ્ય: બધી ચેનલોમાં દૃશ્યમાન રીઅલ-ટાઈમ સ્ટોક સ્તરો, ઓવરસેલિંગ અટકાવે છે

- ક્રોસ-ચેનલ ઓર્ડર પ્રાથમિકતા: જ્યારે સ્ટોક મર્યાદિત હોય, નિયમ-આધારિત ફાળવણી ખાતરી કરે છે કે સૌથી વધુ માર્જિન અથવા સૌથી વ્યૂહાત્મક ચેનલને પ્રાથમિકતા મળે

- એકીકૃત ઇન્વોઇસિંગ: બધી ચેનલો માટે એક invoice and billing system, GST પાલન અને સમાધાનને સરળ બનાવે છે

- માંગ સંવેદન: બધી ચેનલોમાંથી એકત્રિત માંગ ડેટા સિંગલ-ચેનલ ડેટાની તુલનામાં આગાહીની ચોકસાઈમાં 20-30% સુધારો કરે છે

ભારતીય વિતરકો માટે ઓમ્નિચેનલ ટેકનોલોજી સ્ટેક

હેતુ-નિર્મિત ટેકનોલોજી વિના ઓમ્નિચેનલ વ્યૂહરચના અમલમાં મૂકવી અશક્ય છે. અહીં 2026 માં ભારતીય FMCG વિતરકોને જરૂરી ટેકનોલોજી સ્ટેક છે.

લેયર 1: કોર Distribution Management System (DMS)

આ કેન્દ્રીય નર્વસ સિસ્ટમ છે — distributor management, ઇન્વેન્ટરી, ઇન્વોઇસિંગ અને રિપોર્ટિંગ સંભાળે છે. તેણે મલ્ટિ-ચેનલ કામગીરીને ઍડ-ઑન મોડ્યુલ તરીકે નહીં પણ મૂળભૂત રીતે સપોર્ટ કરવી જોઈએ. મુખ્ય ક્ષમતાઓમાં શામેલ છે:

- મલ્ટિ-વેરહાઉસ સંચાલન: GT godown, MT staging area અને quick commerce buffer stock માટે અલગ સ્ટોક ટ્રેકિંગ

- ચેનલ-વાર P&L: માત્ર સંકલિત નંબરો જ નહીં પણ ચેનલ સ્તરે નફાકારકતા વિશ્લેષણ

- કોન્ફિગરેબલ વર્કફ્લો: GT ઓર્ડર (₹10,000 થી નીચે ઓટો-એપ્રુવ) વિરુદ્ધ MT ઓર્ડર (₹1 લાખથી વધુ રકમ માટે ક્રેડિટ ચેક જરૂરી) માટે વિવિધ મંજૂરી પ્રક્રિયાઓ

લેયર 2: API એકીકરણ લેયર

Modern trade અને quick commerce ચેનલો APIs અને Electronic Data Interchange (EDI) દ્વારા સંચાર કરે છે. ટેકનોલોજી સ્ટેકે સપોર્ટ કરવો જોઈએ:

- રિટેલર પોર્ટલ APIs: DMart ની Infinia સિસ્ટમ, Reliance Retail ના JioMart B2B પોર્ટલ અને સમાન પ્લેટફોર્મ્સમાંથી સ્વચાલિત ઓર્ડર ઇન્જેશન

- Quick commerce APIs: Blinkit, Zepto અને Swiggy Instamart dark store સિસ્ટમો માટે રીઅલ-ટાઈમ ઇન્વેન્ટરી પુશ

- Marketplace એકીકરણ: Amazon, Flipkart અને JioMart ગ્રાહક પ્લેટફોર્મ સાથે સ્વચાલિત ઓર્ડર પૂર્તિ અને ઇન્વેન્ટરી સિંક

- એકાઉન્ટિંગ એકીકરણ: નાણાકીય ડેટા સુસંગતતા માટે Tally, Busy અથવા SAP સાથે દ્વિ-દિશા સિંક

લેયર 3: Analytics અને Decision Intelligence

બહુવિધ ચેનલોમાંથી ડેટા વહેવાથી, analytics layer વ્યૂહાત્મક નિર્ણયો માટે મહત્વપૂર્ણ બને છે:

- ચેનલ મિક્સ ઓપ્ટિમાઇઝેશન: દરેક ચેનલને SKU ફાળવણીની કેટલી ટકાવારી કુલ માર્જિન મહત્તમ કરે છે?

- Cannibalisation શોધ: શું quick commerce વૃદ્ધિ નવા ગ્રાહકો પાસેથી આવી રહી છે કે GT વોલ્યુમ ખસેડવાથી?

- ચેનલ દ્વારા Scheme ROI: કયા પ્રમોશન વધારાનું વોલ્યુમ ચલાવે છે વિરુદ્ધ માત્ર ચેનલો વચ્ચે માંગ ખસેડે છે?

- માંગ આગાહી: ML મોડેલો જે ચેનલ-વિશિષ્ટ સિઝનાલિટી, તહેવાર સમયગાળા અને પ્લેટફોર્મ સેલ ઇવેન્ટ્સને ધ્યાનમાં લે છે

લેયર 4: Field Force અને Logistics

માનવ તત્વ મહત્વપૂર્ણ રહે છે, ખાસ કરીને GT કામગીરી માટે. ટેક સ્ટેકમાં શામેલ હોવું જોઈએ:

- સેલ્સમેન એપ: GT beat coverage, field force tracking અને in-market execution માટે

- રૂટ આયોજન: ઓપ્ટિમાઇઝ્ડ રૂટ જે એક જ વાહન રન પર GT outlets, MT deliveries અને quick commerce dark store પુનઃપૂર્તિનો સમાવેશ કરી શકે છે

- ડિલિવરી સંચાલન: MT અને quick commerce SLAs માટે e-POD (electronic proof of delivery) સાથે રીઅલ-ટાઈમ ડિલિવરી ટ્રેકિંગ

Quick Commerce: જે ચેનલને વિતરકો અવગણી શકતા નથી

Quick commerce વિશેષ ધ્યાન માટે પાત્ર છે કારણ કે તે વાર્ષિક 50-60% વૃદ્ધિ કરી રહી છે અને ભારતના ટોચના 20 શહેરોમાં ગ્રાહક અપેક્ષાઓને મૂળભૂત રીતે પુનઃઆકાર આપી રહી છે. Blinkit (Zomato), Zepto અને Swiggy Instamart 2026 ની શરૂઆતમાં 10-15 મિનિટના સરેરાશ ડિલિવરી સમય સાથે દૈનિક 15 લાખથી વધુ ઓર્ડર પ્રક્રિયા કરે છે.

Quick Commerce વિતરકોને કેવી રીતે અસર કરે છે

- Dark store પુનઃપૂર્તિ: રિટેલર્સને ડિલિવર કરવાને બદલે, વિતરકો dark stores ને ડિલિવર કરે છે — quick commerce પ્લેટફોર્મ દ્વારા સંચાલિત વેરહાઉસ. ઓર્ડર પેટર્ન સંપૂર્ણપણે અલગ છે: સેંકડો SKUs માં નાની માત્રામાં દૈનિક ઓર્ડર

- સંકુચિત lead times: Quick commerce પ્લેટફોર્મ same-day અથવા next-day પુનઃપૂર્તિની અપેક્ષા રાખે છે. dark store માં stockout એટલે દિવસોમાં નહીં, કલાકોમાં વેચાણ ગુમાવવું

- SKU તર્કસંગતકરણ: Dark stores માત્ર 2,000-5,000 SKUs વહન કરે છે વિરુદ્ધ સામાન્ય MT સ્ટોરમાં 15,000+. લિસ્ટેડ થવા — અને રહેવા — માટે સતત ઉપલબ્ધતા અને સ્પર્ધાત્મક માર્જિન જરૂરી છે

- ડેટા શેરિંગ: પ્લેટફોર્મ ગ્રાન્યુલર વેચાણ ડેટા (કલાકવાર, dark store દ્વારા, SKU દ્વારા) શેર કરે છે જેનો ચતુર વિતરકો માંગ આયોજન માટે ઉપયોગ કરી શકે છે

ચેન્નઈ, અમદાવાદ અને કોલકાતા ના વિતરકો — જે શહેરોમાં quick commerce આક્રમક રીતે વિસ્તરી રહી છે — ને હવે dark store servicing ક્ષમતાઓ બનાવવી જરૂરી છે અથવા સીધી બ્રાન્ડ-ટુ-પ્લેટફોર્મ સપ્લાય ચેઇન દ્વારા બાયપાસ થવાનું જોખમ રાખવું પડશે.

કેસ સ્ટડી: મહારાષ્ટ્રમાં FMCG વિતરકની ઓમ્નિચેનલ યાત્રા

પુણે સ્થિત મધ્યમ કદના FMCG વિતરક, snacks, beverages અને personal care માં 8 બ્રાન્ડ્સનો પોર્ટફોલિયો સંભાળે છે, ઓમ્નિચેનલ સંક્રમણનું ઉદાહરણ આપે છે.

પ્રારંભિક બિંદુ (2025 ની શરૂઆત)

- આવક વિભાજન: GT 82%, MT 15%, D2C/quick commerce 3%

- સિસ્ટમો: GT બિલિંગ માટે અલગ Tally, MT ઓર્ડર ટ્રેકિંગ માટે Excel, quick commerce સંકલન માટે WhatsApp

- પીડા બિંદુઓ: વિલંબિત GT-પ્રાથમિકતા ડિસ્પેચને કારણે MT માં વારંવાર stockouts, dark store ઇન્વેન્ટરી સ્તરોમાં શૂન્ય દૃશ્યતા, ચેનલો વચ્ચે scheme સંઘર્ષોથી ₹3.2 લાખનો માસિક નુકસાન

ઓમ્નિચેનલ પરિવર્તન

વિતરકે ચેનલ-વિશિષ્ટ મોડ્યુલો સાથે એકીકૃત distribution management system લાગુ કરી:

- ચેનલ ફાળવણી સાથે એકીકૃત ઇન્વેન્ટરી: GT (60%), MT (25%) અને quick commerce (15%) માટે સમર્પિત સ્ટોક પૂલ, માંગ પર આધારિત ગતિશીલ રીબેલેન્સિંગ સાથે

- સ્વચાલિત MT ઓર્ડર પ્રક્રિયા: EDI એકીકરણે મેન્યુઅલ ઓર્ડર એન્ટ્રી દૂર કરી, દૈનિક પ્રક્રિયા સમય 4 કલાકથી 15 મિનિટ સુધી ઘટાડ્યો

- Quick commerce ડેશબોર્ડ: પુણેમાં 12 Blinkit અને 8 Zepto સ્થાનો પર રીઅલ-ટાઈમ dark store ઇન્વેન્ટરી સ્તરો, સ્વચાલિત પુનઃપૂર્તિ ટ્રિગર્સ સાથે

- કેન્દ્રિત scheme સંચાલન: સંઘર્ષ શોધ ચેતવણીઓ સાથે, એક જ એન્જિન દ્વારા સંચાલિત બધા ચેનલ પ્રમોશન

8 મહિના પછીના પરિણામો

- આવક વિભાજન: GT 68%, MT 17%, Quick commerce 12%, D2C પૂર્તિ 3% — તંદુરસ્ત વૈવિધ્યીકરણ

- કુલ આવક વૃદ્ધિ: વર્ષ-દર-વર્ષ 28%, જેમાં quick commerce માસિક ₹18 લાખનું યોગદાન આપે છે (₹3 લાખથી)

- Scheme સંઘર્ષ નુકસાન: દર મહિને ₹3.2 લાખથી ઘટીને ₹40,000 થયું

- MT fill rate: 78% થી 96% સુધી સુધાર્યું, રિટેલ ચેઇન સાથેના સંબંધો મજબૂત કર્યા

- કાર્યકારી મૂડી કાર્યક્ષમતા: વધુ સારી ઇન્વેન્ટરી ફાળવણી અને ઘટાડેલા ઓવરસ્ટોકિંગ દ્વારા 15% સુધારી

મુખ્ય સમજ: વિતરકે નવી ચેનલો માટે GT છોડ્યું નહીં. તેના બદલે, ટેકનોલોજીએ ચેનલોમાં કાર્યક્ષમ સંસાધન ફાળવણી સક્ષમ કરી, GT માર્જિનને રક્ષણ આપતા કુલ આવક વધારી. ચાવી એક ચેનલને બીજી ઉપર પસંદ કરવાની નહોતી — પરંતુ એકીકૃત દૃશ્યતા અને સ્વચાલિત વર્કફ્લો હતી.

ચેનલ સંઘર્ષ અટકાવવો: વ્યવહારુ વ્યૂહરચનાઓ

ઓમ્નિચેનલ વિશ્વમાં ચેનલ સંઘર્ષ અનિવાર્ય છે, પરંતુ તેનું સંચાલન કરી શકાય છે. અહીં અગ્રણી ભારતીય FMCG કંપનીઓ દ્વારા ઉપયોગમાં લેવાતી સાબિત વ્યૂહરચનાઓ છે:

વિભિન્ન ઉત્પાદન વ્યૂહરચના

ચેનલ-એક્સક્લુઝિવ SKUs અથવા pack sizes ઓફર કરો. ઉદાહરણ તરીકે, kirana stores માટે 200g pack, MT માટે 500g value pack, D2C માટે પ્રીમિયમ વેરિઅન્ટ અને quick commerce માટે combo pack. આ ચેનલોમાં સીધી કિંમત તુલનાઓ ઘટાડે છે.

GT રિટેલર્સ માટે માર્જિન રક્ષણ

GT રિટેલર્સ ભારતીય વિતરણની કરોડરજ્જુ છે. જે બ્રાન્ડ્સ રિટેલર માર્જિનનું રક્ષણ કરે છે — સારી trade schemes, loyalty programmes અને એક્સક્લુઝિવ પ્રમોશન દ્વારા — અન્ય ચેનલો વધે છતાં તંદુરસ્ત GT નેટવર્ક જાળવી રાખે છે. FMCG distributor margins નું સંપૂર્ણ ચિત્ર સમજવું આ સંતુલન ક્રિયા માટે આવશ્યક છે.

ટેકનોલોજી-સક્ષમ પારદર્શિતા

બ્રાન્ડ પ્રિન્સિપાલ સાથે ચેનલ પ્રદર્શન ડેટા શેર કરવા માટે sales analytics નો ઉપયોગ કરો. જ્યારે બ્રાન્ડ્સ જુએ છે કે ચોક્કસ quick commerce પ્રમોશન GT વેચાણને cannibalised કર્યું છે, ત્યારે તેઓ તેમની વ્યૂહરચના સમાયોજિત કરવાની વધુ સંભાવના ધરાવે છે — પરંતુ માત્ર ત્યારે જ જ્યારે વિતરક માત્ર ફરિયાદો નહીં, પણ વિશ્વસનીય ડેટા રજૂ કરી શકે.

ભૌગોલિક ચેનલ સંરેખણ

ચેનલ વ્યૂહરચનાઓને ભૌગોલિક વાસ્તવિકતાઓ સાથે સંરેખિત કરો. મુંબઈ અને દિલ્હી જેવા tier-1 શહેરોમાં, ચારેય ચેનલો સહઅસ્તિત્વ ધરાવશે અને સ્પર્ધા કરશે. ઇન્દોર અને નાગપુર જેવા tier-2 શહેરોમાં, GT અને MT પ્રબળ છે. ગ્રામીણ વિસ્તારોમાં, GT લગભગ સંપૂર્ણ બજાર છે. સંસાધન ફાળવણીએ આ વાસ્તવિકતા સાથે મેળ ખાવો જોઈએ.

2026 અને તે પછી માટે વિતરકની સર્વાઇવલ પ્લેબુક

ભારતીય FMCG વિતરણ લેન્ડસ્કેપ ઉદારીકરણ પછીના સૌથી નોંધપાત્ર પરિવર્તનમાંથી પસાર થઈ રહ્યું છે. જે વિતરકો સફળ થશે તેઓ ચોક્કસ લાક્ષણિકતાઓ શેર કરશે:

- ટેકનોલોજી-પ્રથમ માનસિકતા: ચેનલ-વિશિષ્ટ મેન્યુઅલ પ્રક્રિયાઓને વળગી રહેવાને બદલે મલ્ટિ-ચેનલ જટિલતા સંભાળતા એકીકૃત DMS પ્લેટફોર્મ્સમાં રોકાણ કરવું

- ડેટા-આધારિત નિર્ણયો: ઇન્વેન્ટરી ફાળવવા, schemes નું મૂલ્યાંકન કરવા અને બ્રાન્ડ સાથે વાટાઘાટ કરવા માટે ચેનલ analytics નો ઉપયોગ — ગટ instinct ને પુરાવા સાથે બદલવો

- ચેનલ ચપળતા: મોટાભાગનો નફો ઉત્પન્ન કરતા GT બેઝને રક્ષણ આપતા quick commerce જેવી નવી ચેનલોને સેવા આપવાની ઇચ્છા

- કાર્યકારી મૂડી શિસ્ત: વ્યાપક રીતે અલગ ચુકવણી ચક્ર સાથે ચેનલોમાં રોકડ પ્રવાહનું સંચાલન — GT cash retailers માટે 7 દિવસથી MT ચેઇન માટે 60 દિવસ

- બ્રાન્ડ ભાગીદારી અભિગમ: પોતાને માત્ર GT ડિલિવરી એજન્ટ તરીકે નહીં પણ ઓમ્નિચેનલ એક્ઝિક્યુશન પાર્ટનર તરીકે સ્થાન આપવું

જે વિતરકો આ વાતાવરણમાં નિષ્ફળ જાય છે તેઓ એ હશે જે મલ્ટિ-ચેનલ કામગીરીનો પ્રતિકાર કરે છે, ટેકનોલોજી એકીકરણનો અભાવ હોય છે, અથવા ચેનલ અર્થશાસ્ત્રનું કઠોરપણે સંચાલન કરવામાં નિષ્ફળ જાય છે.

ઓમ્નિચેનલ વિતરણ તરફ પ્રથમ પગલું ભરો

જો તમે ભારતીય FMCG વિતરક છો જે અનેક ચેનલોનું સંચાલન કરી રહ્યા છો — અથવા સંચાલન કરવાની તૈયારી કરી રહ્યા છો — તો સૌથી અસરકારક પગલું એ એકીકૃત distribution management platform લાગુ કરવાનું છે. સાયલોમાં ચેનલોનું સંચાલન કરવાનો ખર્ચ — અલગ સ્પ્રેડશીટ્સ, અલગ બિલિંગ સિસ્ટમો અને અલગ ટીમો દ્વારા — દર મહિને ગુમાવેલી કાર્યક્ષમતા, માર્જિન ધોવાણ અને ચૂકી ગયેલી તકોમાં વધે છે.

SpireStock ભારતીય વિતરકોને ઓમ્નિચેનલ કામગીરી માટે જરૂરી એકીકૃત પ્લેટફોર્મ પ્રદાન કરે છે: multi-channel order management, channel-specific workspaces, એકીકૃત invoicing and billing અને રીઅલ-ટાઈમ analytics across channels. પછી ભલે તમે સુરત માં kiranas ની સેવા આપો છો અથવા બેંગલુરુ માં dark stores ફરી ભરી રહ્યા છો, પ્લેટફોર્મ તમારી જરૂરિયાતો અનુસાર સ્કેલ થાય છે.

તમારી ઓમ્નિચેનલ વિતરણ વ્યૂહરચના બનાવવા તૈયાર છો? અમારી ટીમ સાથે સલાહ સુનિશ્ચિત કરો, અથવા તમારી વિતરણ કામગીરી માટે યોગ્ય ફિટ શોધવા અમારી યોજનાઓ શોધો.

સ્ત્રોતો અને સંદર્ભો

- RedSeer Strategy Consultants Quick Commerce Report 2025

- Nielsen India Retail Intelligence FMCG Channel Report 2025-26

- Retailers Association of India Modern Trade Growth Analysis 2026

વારંવાર પૂછાતા પ્રશ્નો

ઓમ્નિચેનલ વિતરણ એટલે એકસાથે અનેક વેચાણ ચેનલો દ્વારા ઉત્પાદન પ્રવાહનું સંચાલન — general trade (kirana stores), modern trade (DMart, Reliance), D2C (બ્રાન્ડ વેબસાઇટ) અને quick commerce (Blinkit, Zepto). આ માટે બધી ચેનલોમાં એકીકૃત ઇન્વેન્ટરી, કિંમત અને ઓર્ડર સંચાલનની જરૂર પડે છે.

General trade MRP પર 3.5-8% માર્જિન આપે છે, modern trade 1-3% અને quick commerce 2-5% પ્રદાન કરે છે. જોકે, ચુકવણીની શરતો નોંધપાત્ર રીતે બદલાય છે — GT 7-21 દિવસમાં ચૂકવે છે જ્યારે MT 30-60 દિવસ લે છે, જે વાસ્તવિક કાર્યકારી મૂડી વળતરને અસર કરે છે.

મુખ્ય વ્યૂહરચનામાં ચેનલ-એક્સક્લુઝિવ SKUs અથવા pack sizes, Minimum Advertised Price નીતિઓ, વિરોધાભાસી પ્રમોશન રોકવા માટે કેન્દ્રિત scheme સંચાલન અને cannibalisation શોધવા માટે રીઅલ-ટાઈમ analytics શામેલ છે. ટેકનોલોજી-સક્ષમ પારદર્શિતા બ્રાન્ડ્સ અને વિતરકોને ચેનલ વ્યૂહરચના પર સંરેખિત કરવામાં મદદ કરે છે.

Quick commerce માટે વિતરકોએ dark stores ને ઘણા SKUs માં નાની માત્રામાં દૈનિક પુનઃપૂર્તિ કરવી પડે છે, સંકુચિત same-day lead times અને API-આધારિત ઓર્ડર એકીકરણ. જે વિતરકો આ ક્ષમતાઓ બનાવે છે તેઓ નવી આવક ચેનલ મેળવે છે; જે નથી કરતા તેઓ બાયપાસ થવાનું જોખમ રાખે છે.

મલ્ટિ-ચેનલ ઓર્ડર સંચાલન, MT અને quick commerce પ્લેટફોર્મ માટે API એકીકરણ, ચેનલ-વાર ઇન્વેન્ટરી ફાળવણી, કેન્દ્રિત scheme engine, એકીકૃત ઇન્વોઇસિંગ અને ચેનલ-મિક્સ ઓપ્ટિમાઇઝેશન માટે analytics સાથેનું એકીકૃત DMS. દરેક ચેનલ માટે અલગ સિસ્ટમો અયોગ્ય જટિલતા સર્જે છે.

એક અવિભાજિત પૂલ ટાળો. માંગ પેટર્ન પર આધારિત દરેક ચેનલને સમર્પિત સ્ટોક ફાળવો — GT ને નિયમિત સાપ્તાહિક પુનઃપૂર્તિ સાથે 15-20 દિવસનો સેફ્ટી સ્ટોક, MT ને લાંબા lead times ને કારણે 25-30 દિવસ અને quick commerce ને દૈનિક પુનઃપૂર્તિ સાથે 3-5 દિવસ જરૂરી છે.

Quick commerce ઝડપથી tier-2 શહેરો જેવા કે પુણે, જયપુર, લખનૌ અને ચંદીગઢમાં વિસ્તરી રહી છે. 2027 સુધીમાં પ્લેટફોર્મ 40-50 શહેરો આવરી લેવાની યોજના ધરાવે છે. આ શહેરોના વિતરકોએ આ વૃદ્ધિ કબજે કરવા માટે હવે dark store સર્વિસિંગ ક્ષમતાઓ બનાવવાનું શરૂ કરવું જોઈએ.

ટેકનોલોજી સાથે GT કામગીરી મજબૂત કરીને શરૂ કરો — ડિજિટલ ઓર્ડર કેપ્ચર, રૂટ ઓપ્ટિમાઇઝેશન અને analytics. પછી તમારા વિસ્તારમાં 2-3 dark stores ને સેવા આપીને પસંદગીપૂર્વક quick commerce માં પ્રવેશો. એકસાથે બધી ચેનલોની સેવા આપવાનો પ્રયાસ કરવાને બદલે એક્ઝિક્યુશન ઉત્કૃષ્ટતા પર ધ્યાન કેન્દ્રિત કરો.

સંબંધિત SpireStock ફીચર્સ

મલ્ટિ-લેવલ મંજૂરી વર્કફ્લો સાથે પ્લેસમેન્ટથી ડિલિવરી સુધી એન્ડ-ટુ-એન્ડ ઓર્ડર લાઇફસાયકલ.

વેચાણ વલણો, MIS રિપોર્ટ્સ અને વિતરણ એનાલિટિક્સ સાથે શક્તિશાળી ડેશબોર્ડ્સ.

કસ્ટમ બ્રાન્ડિંગ અને કન્ફિગરેશન સાથે દરેક ગ્રાહક માટે અલગ વર્કસ્પેસ.

HSN કોડ, ગેટ પાસ અને ફાઇનાન્સ લેજર સાથે GST-કમ્પ્લાયન્ટ ઇન્વોઇસિંગ.

સંબંધિત ઉદ્યોગો

ઓર્ડર વ્યવસ્થાપન, બીટ આયોજન, રિટેલર ટ્રેકિંગ અને GST બિલિંગ સાથે FMCG વિતરણને સુવ્યવસ્થિત કરો.

કોલ્ડ ચેઇન ટ્રેકિંગ, ક્રેટ વ્યવસ્થાપન, રૂટ ઑપ્ટિમાઇઝેશન અને રિયલ-ટાઇમ ડિલિવરી દેખરેખ સાથે પીણાં વિતરણનું સંચાલન કરો.

ઉપભોક્તા ચીજવસ્તુઓ બ્રાન્ડ્સ માટે વિતરણ વ્યવસ્થાપન. સમગ્ર ભારતમાં વિતરકો, રિટેલર્સ, સ્કીમ અને વેચાણ એનાલિટિક્સનું સંચાલન કરો.

સંબંધિત ઉકેલો

તમારા સંપૂર્ણ distributor નેટવર્કનું ડિજિટલ રીતે સંચાલન કરો. ઓનબોર્ડિંગ, ક્રેડિટ મર્યાદા, બાકી ટ્રેકિંગ અને પ્રદર્શન વિશ્લેષણ. મફત ટ્રાયલ શરૂ કરો.

તમારા રિટેલ નેટવર્કને ટ્રૅક અને મેનેજ કરો. આઉટલેટ્સ જિયો-ટેગ કરો, ગૌણ sales કેપ્ચર કરો, બીટ્સ મેનેજ કરો અને retailer પ્રદર્શન મોનિટર કરો.

સંબંધિત એન્ટિટીઝ

તમારા વિતરણને સુવ્યવસ્થિત કરવા તૈયાર છો?

તમારી 30 દિવસની મફત ટ્રાયલ શરૂ કરો અને જુઓ કે SpireStock તમારા ડેરી, FMCG અથવા ગ્રાહક વસ્તુ વિતરણને ઓર્ડરથી ક્રેટ રિકવરી સુધી કેવી રીતે બદલી શકે છે.

SpireStock Team

ડિસ્ટ્રિબ્યુશન ટેક્નોલોજી નિષ્ણાતો

SpireStock Team SpireStock માટે ડિસ્ટ્રિબ્યુશન મેનેજમેન્ટ, સપ્લાય-ચેઇન ઑપ્ટિમાઇઝેશન અને ભારતીય ડેરી અને FMCG બ્રાન્ડ્સ માટેના ફીલ્ડ ઑપરેશન્સ પર લખે છે.