The Payment Collection Challenge in Dairy Distribution

Cash flow is the lifeblood of any business, but it is especially critical in dairy distribution where companies must pay farmers and processors regularly regardless of when distributors pay. Yet delayed payments are endemic in Indian dairy distribution, the average collection period is 15-30 days, with some accounts stretching to 45-60 days or beyond. At a Rs 200-crore dairy, every additional day of Days Sales Outstanding (DSO) ties up roughly Rs 55 lakh in working capital, so a 10-day improvement is worth Rs 5.5 crore of released cash. That is real money that could fund growth, better farmer prices, or a long-overdue infrastructure upgrade.

This is not just a financial problem. It creates a cascade: strained supplier relationships, inability to invest in growth, increased borrowing costs, and in extreme cases, viability threats. Yet many dairy companies manage collections through manual follow-ups, scattered records, and inconsistent enforcement. The same dynamic affects operators across dairy distribution, FMCG distribution, beverage distribution, and consumer goods, every industry serving kirana-led retail markets faces the same collection discipline challenge.

Why Dairy Payment Collection Is Uniquely Challenging

- Daily transactions, with orders every day, the transaction volume is massive and tracking becomes complex

- Multiple payment modes, cash, UPI, cheque, NEFT, credit adjustments, and scheme claims all mix together

- Returns and adjustments, damaged goods, expired products, and short deliveries create credits that complicate reconciliation

- Relationship sensitivity, aggressive collection damages distributor relationships that took years to build

- Informal practices, many transactions still happen through verbal commitments and informal arrangements

- Low margins, dairy operates on thin margins, so every bad debt rupee hurts disproportionately

These dynamics mean that generic accounts-receivable tools built for monthly invoicing do not work for dairy. You need collection discipline that fits a daily order cycle and accommodates the operational realities of perishable-goods distribution.

Building a Systematic Payment Collection Process

1. Establish Clear Credit Policies

Define credit terms before the first transaction, not after the first default. Each distributor should have documented credit limits, payment periods, and consequences for overdue amounts. Make these part of the distributor onboarding process, not an afterthought introduced six months in when problems start surfacing.

2. Digitize All Transactions

Every order, delivery, invoice, payment, return, and adjustment must be recorded digitally in your order management and billing system. This creates an irrefutable ledger that both you and the distributor can reference at any time, eliminating the "I thought I paid" conversations and the endless back-and-forth over which credit note applied to which invoice.

3. Automate Payment Reminders

Set up automated reminders that trigger based on payment due dates:

- 3 days before due, friendly reminder with outstanding amount and payment options

- On due date, payment due notification

- 3 days overdue, overdue alert with a request to clear

- 7 days overdue, escalation to sales manager with potential credit hold warning

- 14 days overdue, automatic credit hold; new orders blocked until payment is made

4. Enable Digital Payment Options

Make it easy for distributors to pay. Support UPI, NEFT, IMPS, and online payment links in addition to traditional cash and cheque. The easier it is to pay, the faster payments come in. A distributor in Bangalore who can clear an invoice by tapping a UPI link on their phone will always pay faster than one who has to visit the bank.

5. Implement Credit Controls

Automatic credit limit enforcement is the most effective collection tool. When a distributor's outstanding balance exceeds their credit limit, the system blocks new orders until payments bring the balance within limits. This creates urgency without confrontation, the system says no, not the sales rep.

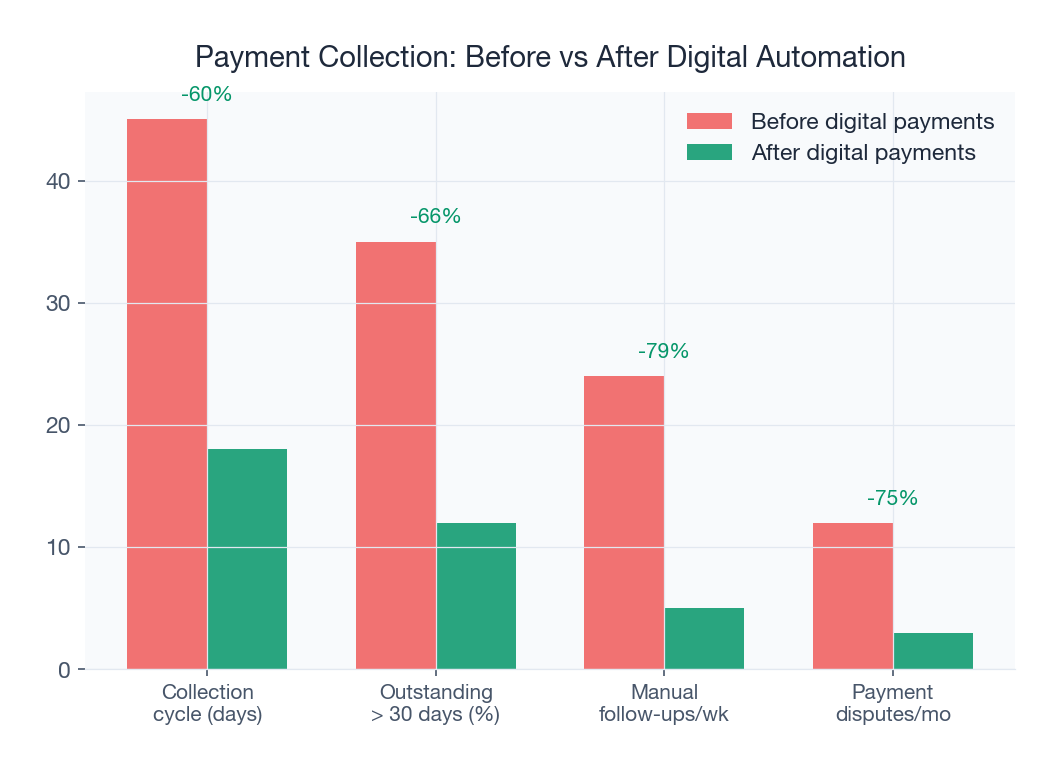

Collection Performance Benchmarks

| Metric | Manual Process | Digital (SpireStock) | Impact |

|---|---|---|---|

| Average DSO | 28 days | 16 days | -12 days |

| Bad debt ratio | 1.8% | 0.4% | -1.4 pts |

| Collection efficiency | 73% | 94% | +21 pts |

| Dispute rate | 11% | 1.5% | -9.5 pts |

| Reconciliation time (monthly) | 38 hours | 4 hours | -89% |

| Same-day payment receipts | 18% | 61% | +43 pts |

Leveraging Technology for Better Collections

Real-Time Outstanding Dashboard

SpireStock's analytics provide real-time visibility into outstanding amounts across your distributor network, total receivables, aging analysis, overdue amounts, and payment trends. This dashboard helps you prioritize collection efforts where they will have the most impact. Without it, most companies chase the loudest distributor rather than the highest-value overdue account.

Field Collection Support

When sales staff visit distributors, they can view outstanding amounts, record payments on the spot through the mobile app, and issue digital receipts. This makes every field visit a potential collection opportunity. Combined with structured field activity tracking, you get a multiplier effect: more visits, more collection opportunities, more payments received.

Reconciliation Automation

Monthly reconciliation, matching your records with each distributor's, is dramatically simplified when both sides have access to the same digital ledger. Disputes about amounts, dates, and adjustments drop by 90% when the data is transparent and shared.

Payment Link Automation

The latest UPI integrations let you auto-generate payment links attached to every invoice. The distributor taps the link, pays, and both systems update in real time. No manual matching, no end-of-day reconciliation batch, no disputes about which invoice a given payment was against.

Payment Collection Best Practices

- Separate sales from collection, do not make your sales team the primary collection mechanism; their role is relationship and revenue growth

- Incentivize early payment, offer small discounts (0.5-1%) for advance payment or prompt settlement

- Penalize late payment, charge interest on overdue amounts (within legal limits) and communicate this policy clearly

- Regular ledger sharing, send weekly or fortnightly ledger statements to every distributor proactively

- Escalation protocols, define clear escalation paths from sales representative to manager to director for chronic defaulters

- Credit insurance, for large outstandings, consider trade credit insurance from providers like ECGC or Coface

The right payment collection solution enforces all of these practices automatically so they do not depend on any one person's vigilance. Automation is what turns best practices into standard operating procedures.

Collection Economics: Why This Matters So Much

Consider a Rs 150-crore dairy with 28 days DSO. Reducing that to 18 days releases approximately Rs 4.1 crore of working capital, money that can fund a new plant expansion, buy 14 new delivery vehicles, or pay for a three-year DMS subscription 40 times over. And this is before counting the reduction in interest costs (many mid-sized dairies carry short-term borrowing at 10-12% APR, so Rs 4 crore of freed working capital saves Rs 40-48 lakh in interest every year).

Companies in Pune, Chennai, and Delhi that have gone through this transformation report remarkably consistent numbers. The savings pay for the software within 4-6 months and compound every year thereafter.

Dealing With Chronic Defaulters

Every distribution network has a handful of chronic late payers. The temptation is to let them slide because they drive revenue. Resist that temptation. Chronic defaulters rarely reform on their own; they need firm boundaries. Establish a clear path: notice, formal warning, credit hold, final warning, and termination. Document every step in the system so there is no ambiguity if the relationship ends in a legal dispute.

Contrast that with a brand like Amul or Nandini, both of whom run tight credit policies with zero exceptions. Their discipline is precisely why their distributor networks are so financially healthy.

Integration With Accounting

Payment data from SpireStock integrates with Tally, Busy, SAP, and other accounting systems so every payment received is reflected in your financial books without manual data entry. This closes the loop between operations and finance and eliminates the end-of-month scramble that used to consume entire days. For deeper reading, see our companion pieces on managing dairy distributors and GST billing for dairy distribution.

Start Collecting Smarter Today

For dairy companies operating in the dairy distribution market, improving collection efficiency from 70% to 95% (a common improvement with systematic digital management) can free up crores in working capital, money that can be reinvested in growth, new products, or better terms with the FMCG distribution supply chain. Talk to our team for a working-capital assessment, review SpireStock pricing to understand the commercial structure, or book a demo to see the collection dashboard live against your distributor ledger.

Case Study: Regional Dairy Cuts DSO by 11 Days

A Rs 180-crore regional dairy operating in Ahmedabad and surrounding districts rolled out SpireStock's integrated payment collection workflow in Q2 2024. Over the next six months, their Days Sales Outstanding dropped from 29 days to 18 days, bad debt fell from 2.1% of revenue to 0.5%, and their collection team size shrank from 4 full-time accountants to 2 (the freed staff were reassigned to credit analysis). Total cash released: approximately Rs 5.4 crore of working capital. Total annual savings including interest: Rs 68 lakh. Payback on the software: under two months.

What made the difference was not just the software but the discipline to use it every day. The finance head committed to personally reviewing the aging dashboard every morning at 9:15 AM and driving the collection calls for any account over 21 days overdue. After three months, the distributor network had internalized the new rhythm, and most payments began arriving well within terms.

Collections in Tough Economic Conditions

When the broader economy tightens, collection becomes harder. Distributors face their own cash flow pressures and delay payments upstream. The companies that handle these cycles best are the ones with real-time visibility and disciplined escalation. A bad quarter reveals who has the data and process to act quickly versus who is flying blind. Build the infrastructure during good times so you can use it when conditions get tough.

Reporting Rhythm

Weekly collection reviews should cover: top 10 overdue accounts, accounts approaching credit limits, aging distribution trends, and recovery progress on prior issues. Monthly reviews should expand to cover collection efficiency by territory, by sales manager, by product category, and by payment mode. This structured rhythm is what separates companies that merely collect money from companies that actively manage their receivables as a strategic lever.

Credit Scoring for Distributors

Advanced operators are now applying internal credit scoring to their distributor networks, similar to how banks score retail borrowers. Inputs include payment history, volume growth, business longevity, geographic stability, and financial data from the distributor's own accounts. The output is a credit score that drives automatic credit limit decisions, scheme eligibility, and early-warning alerts. This data-driven approach removes the subjectivity and favouritism that plague manual credit management and protects the company from predictable defaults.

When to Escalate Legally

Most payment disputes never need to go legal if the underlying discipline is in place. But for the small number that do, having a clear digital audit trail is invaluable. Every order, delivery, invoice, payment, adjustment, and communication is logged with timestamps and user IDs. If a dispute reaches arbitration or court, this documentation is dispositive. The same infrastructure that drives daily collection also provides the evidence base for any legal escalation, which in turn creates a credible deterrent against bad actors.

Working Capital Optimization Beyond Collections

Collections are one lever in a broader working capital strategy. Combine faster collections with optimized inventory levels, smarter production scheduling, and better supplier payment terms, and the combined impact can be dramatic. A Rs 260-crore regional dairy we worked with released Rs 12 crore of working capital in 18 months through a combined program, 50% from collection improvements, 30% from inventory rationalization, and 20% from supplier term renegotiation. The collection improvement funded the rest of the program several times over.

The Bottom Line

Systematic payment collection is not glamorous, but it is one of the most leveraged improvements a dairy company can make. Every day of DSO reduction releases working capital; every percentage point of bad debt reduction protects the bottom line; every dispute eliminated frees up management time for growth activities. The discipline required is not technical, it is cultural. Build the habits, use the tools, and the results follow within a single quarter.

Sources & References

Frequently Asked Questions

The industry average is 15-30 days, though it varies widely. Some well-managed networks operate on 7-day terms, while poorly managed networks see averages of 45-60 days. Digital payment management typically reduces the average by 7-10 days.

Each distributor has a configured credit limit based on their volume and payment history. When their outstanding balance exceeds this limit, the system automatically blocks new order placement and notifies both the distributor and the sales team. Orders resume once payments bring the balance within limits.

Support all common modes: UPI (growing fastest in India), NEFT/IMPS for bank transfers, cheque (still used for large amounts), cash (common in smaller markets), and online payment links. The more options available, the fewer excuses for delayed payment.

Digitize all transactions (orders, deliveries, returns, adjustments) in a system accessible to both parties. Share ledger statements regularly. When both you and the distributor see the same data in real time, disputes virtually disappear.

Yes, a clearly communicated interest policy (typically 1.5-2% per month) creates financial motivation for timely payment. However, enforce it consistently across all distributors to avoid relationship issues. The policy should be part of the distributor agreement from day one.

Payment records from SpireStock integrate with accounting software (Tally, Busy, SAP), ensuring that every payment received is reflected in your financial books without manual data entry. This eliminates reconciliation gaps between operations and finance teams.

Yes, field staff can record cash collections, generate digital receipts, and even share UPI payment links with distributors during visits. The payment is immediately reflected in the distributor's outstanding balance and visible to the accounts team.

Key KPIs include: Days Sales Outstanding (DSO), collection efficiency percentage, overdue amount as percentage of total receivables, aging analysis (current/30/60/90+ days), and payment mode distribution. Review these weekly to stay on top of collection health.

Related SpireStock Features

Related Solutions

Track distributor and retailer payments. Cash, UPI, cheque collection with reconciliation, ageing reports, and credit limit management.

Manage your entire distributor network digitally. Onboarding, credit limits, outstanding tracking, and performance analytics. Start free trial.

Related Entities

Ready to Streamline Your Distribution?

Start your free 30-day trial and see how SpireStock can transform your dairy, FMCG or consumer-goods distribution operation, from order capture to crate recovery.

SpireStock Team

Product & Industry Insights

SpireStock Team leads product at SpireStock, where the team ships distribution management software for India's dairy, FMCG and consumer-goods brands.