प्राथमिक आणि दुय्यम विक्री म्हणजे काय?

FMCG पुरवठा साखळीतील प्रत्येक उत्पादन ग्राहकापर्यंत पोहोचण्यापूर्वी अनेक हातांमधून जाते. प्रत्येक हस्तांतरण एक वेगळा विक्री व्यवहार दर्शविते आणि हे व्यवहार समजून घेणे वितरण प्रभावीपणे व्यवस्थापित करण्यासाठी मूलभूत आहे. भारतात, जिथे पुरवठा साखळी जगातील सर्वात स्तरीय आहे, तीन संज्ञा कारखान्यापासून ग्राहकापर्यंतच्या वस्तूंच्या प्रवाहाची व्याख्या करतात.

प्राथमिक विक्री म्हणजे उत्पादक (किंवा ब्रँड) आणि वितरक (किंवा C&F एजंट) यांच्यातील व्यवहार. जेव्हा Britannia त्यांच्या मुंबई येथील कारखान्यातून ठाणे येथील सुपर स्टॉकिस्टला बिस्किटांचा एक ट्रक पाठवते, तेव्हा ती प्राथमिक विक्री असते. उत्पादक महसूल नोंदवतो, वितरक इन्व्हेंटरीचा ताबा घेतो आणि वस्तू कारखाना गोदामातून वितरकाच्या गोदामात जातात.

दुय्यम विक्री म्हणजे वितरक आणि किरकोळ विक्रेता यांच्यातील व्यवहार. जेव्हा तो ठाणे सुपर स्टॉकिस्ट मुलुंडमधील किराणा दुकानात सेल्समन पाठवतो आणि 5 कार्टन Marie Gold ची ऑर्डर बुक करतो, तेव्हा ती दुय्यम विक्री असते. वितरकाची इन्व्हेंटरी कमी होते, किरकोळ विक्रेत्याला ग्राहकांना विकण्यासाठी माल मिळतो आणि पैसा (किंवा क्रेडिट) किरकोळ विक्रेत्याकडून वितरकाकडे परत येतो.

तृतीयक विक्री म्हणजे किरकोळ विक्रेता आणि ग्राहक यांच्यातील अंतिम व्यवहार. जेव्हा एखादा ग्राहक त्या मुलुंडमधील किराणा दुकानात जातो आणि 30 रुपयांना Marie Gold चे पाकीट खरेदी करतो, तेव्हा ती तृतीयक विक्री असते. हा प्रत्यक्ष उपभोगाचा क्षण आहे, ज्या ठिकाणी खरी मागणी व्यक्त केली जाते.

हा फरक महत्त्वाचा आहे कारण प्रत्येक स्तर एक वेगळी कथा सांगतो. प्राथमिक विक्री तुम्हाला सांगते की वितरकांनी काय खरेदी केले. दुय्यम विक्री तुम्हाला सांगते की किरकोळ विक्रेते काय साठवत आहेत. तृतीयक विक्री तुम्हाला सांगते की ग्राहकांना प्रत्यक्षात काय हवे आहे. बहुतेक भारतीय FMCG ब्रँडसना प्राथमिक विक्रीची उत्कृष्ट दृश्यमानता असते कारण ते स्वतः बिल तयार करतात. परंतु बहुसंख्य कंपन्यांसाठी दुय्यम आणि तृतीयक विक्री हा एक ब्लॅक बॉक्स राहतो आणि या अंधत्वामुळे त्यांना चुकीच्या पद्धतीने वाटप केलेली संसाधने, संपलेला स्टॉक आणि अयशस्वी उत्पादन लाँचमध्ये कोट्यवधी रुपयांचा फटका बसतो.

तुम्ही FMCG ब्रँडसाठी वितरण व्यवस्थापित करत असाल आणि दुय्यम विक्री ट्रॅकिंग प्रत्यक्षात कसे कार्य करते हे पाहू इच्छित असाल, तर SpireStock चा मोफत डेमो बुक करा आणि तुमच्या संपूर्ण चॅनेलवर रिअल-टाइम दृश्यमानतेचा अनुभव घ्या.

भारतीय FMCG ब्रँडसाठी हा फरक का महत्त्वाचा आहे

प्राथमिक आणि दुय्यम विक्रीतील फरक हा शैक्षणिक नाही. ब्रँड घेत असलेल्या प्रत्येक धोरणात्मक निर्णयावर त्याचा थेट परिणाम होतो, उत्पादन नियोजनापासून ते क्षेत्र विस्तार, योजना डिझाइन आणि वितरक मूल्यांकनापर्यंत. तरीही आश्चर्यकारक संख्येने भारतीय FMCG कंपन्या, अगदी 500 कोटी+ महसूल असलेल्या, जवळजवळ संपूर्णपणे प्राथमिक विक्री डेटावर आधारित महत्त्वपूर्ण निर्णय घेत राहतात.

प्राथमिक विक्री डेटा तुम्हाला सांगतो की तुमच्या वितरकांनी तुमच्याकडून काय खरेदी केले. तो तुम्हाला सांगत नाही की त्या वस्तू वितरकाच्या गोदामात विकल्या न जाता पडल्या आहेत का, पुण्यातील किरकोळ विक्रेते तुमच्या टॉप SKU संपवत आहेत तर नागपूरमधील वितरक अतिरिक्त स्टॉकमध्ये बुडत आहेत का किंवा तो प्रभावी Q3 महसूल आकडा खरी मागणीने चालविला होता का किंवा दिवाळीपूर्वी आक्रमक चॅनेल लोडिंगने.

दुय्यम विक्री डेटा तुम्हाला सांगतो की प्रत्यक्षात काय विकले जात आहे. हे कोणत्या SKU किरकोळ शेल्फमधून बाहेर जात आहेत, कोणत्या क्षेत्रात खरी मागणी आहे, कोणते वितरक किरकोळ स्तरावर चांगले काम करत आहेत (फक्त मोठ्या ऑर्डर देत नाहीत) आणि तुमचे नवीन उत्पादन लाँच प्रत्यक्षात गती मिळवत आहे का किंवा फक्त वितरकांचे शेल्फ भरत आहे का हे दर्शविते.

केवळ प्राथमिक विक्रीसाठी ऑप्टिमाइझ करणाऱ्या कंपन्या नेहमीच एका धोकादायक पॅटर्नमध्ये पडतात: ते तिमाही लक्ष्यांना पूर्ण करण्यासाठी चॅनेलमध्ये इन्व्हेंटरी ढकलतात, वाढीचा भ्रम निर्माण करतात तर प्रत्यक्ष सेल-थ्रू स्थिर किंवा घटत राहते. या पॅटर्नला एक नाव आहे आणि याने संपूर्ण भारतातील वितरण नेटवर्क उद्ध्वस्त केले आहेत.

एका तिमाहीत 100 कोटी रुपयांच्या समान प्राथमिक विक्री असलेले दोन ब्रँड विचारात घ्या. ब्रँड A चे प्राथमिक-ते-दुय्यम गुणोत्तर 1.05 आहे, म्हणजे वितरकांनी जे खरेदी केले त्यापैकी 95% किरकोळ विक्रेत्यांना पुढे विकले गेले. ब्रँड B चे गुणोत्तर 1.4 आहे, म्हणजे वितरकांनी विकलेल्यापेक्षा 40% जास्त इन्व्हेंटरीवर बसले आहेत. ब्रँड A चे वितरण नेटवर्क निरोगी आहे. ब्रँड B हा परतावा, एक्सपायरी क्लेम्स आणि वितरक अॅट्रिशनचा टाइम बॉम्ब आहे. एकट्या प्राथमिक विक्री आकड्याने हा फरक कधीही उघड केला नसता.

चॅनेल स्टफिंग समस्या

चॅनेल स्टफिंग, ज्याला ट्रेड लोडिंग असेही म्हणतात, ही नैसर्गिक मागणीच्या पलीकडे वितरण चॅनेलमध्ये अतिरिक्त इन्व्हेंटरी ढकलण्याची प्रथा आहे. ही भारतीय FMCG वितरणातील सर्वात व्यापक आणि विनाशकारी समस्यांपैकी एक आहे आणि ती जवळजवळ नेहमीच प्राथमिक कामगिरी मेट्रिक म्हणून प्राथमिक विक्रीवरील अतिअवलंबनातून उद्भवते.

चॅनेल स्टफिंग कसे होते

यंत्रणा सरळ आहे. एक ब्रँड त्याच्या एरिया सेल्स मॅनेजर्स (ASM) साठी प्राथमिक विक्रीवर आधारित तिमाही लक्ष्ये सेट करतो, वितरकांना विकलेल्या वस्तूंचे मूल्य. लक्ष्ये गाठण्याच्या दबावाखाली ASM वितरकांना त्यांना आवश्यकतेपेक्षा मोठ्या ऑर्डर देण्यास पटवून देतो, बहुतेकदा अल्प-मुदतीच्या सवलती, विस्तारित क्रेडिट किंवा अतिरिक्त योजना लाभांसह गोड केले जाते. वितरक सहमत होतो कारण कागदावर अर्थशास्त्र आकर्षक दिसते. ब्रँड महसूल बुक करतो आणि लक्ष्य गाठल्याचा उत्सव साजरा करतो.

परंतु वस्तू किरकोळ स्तरावर हलत नाहीत. वितरकाकडे आता इष्टतम 15-20 दिवसांऐवजी 45 दिवसांची इन्व्हेंटरी आहे. उत्पादने एक्सपायरीच्या जवळ येतात. वितरक ती साफ करण्यासाठी मोठ्या सवलतीत स्टॉक डंप करण्यास सुरुवात करतो, ब्रँड इक्विटीचे नुकसान करतो आणि शेजारच्या वितरकांना कमी करतो. जेव्हा अतिरिक्त स्टॉक शेवटी संपतो, तेव्हा वितरक परतावा दाखल करतो आणि 15 लाख रुपयांच्या महसुलासारखे दिसणारे 8 लाख रुपयांच्या प्रत्यक्ष वसूल विक्री आणि 3 लाख रुपयांच्या परतावा प्रक्रिया खर्चात बदलते.

चॅनेल स्टफिंगचा वास्तविक खर्च

RedSeer Consulting च्या 2024 अहवालानुसार, चॅनेल स्टफिंगमुळे भारतीय FMCG उद्योगाला संपलेल्या वस्तू, परतावा लॉजिस्टिक्स, खराब झालेले वितरक संबंध आणि विकृत मागणी सिग्नल्समध्ये वार्षिक 8,000-12,000 कोटी रुपये खर्च येतो. वैयक्तिक ब्रँडसाठी, खर्च खालीलप्रमाणे दिसून येतो:

- उत्पादन परतावा आणि एक्सपायरी क्लेम्स स्टफिंग समस्या असलेल्या ब्रँडसाठी प्राथमिक विक्रीच्या सरासरी 3-8%, शिस्तबद्ध ब्रँडसाठी 1% पेक्षा कमीच्या तुलनेत

- वितरक अॅट्रिशन वार्षिक 15-25% धावत आहे कारण निराश वितरक त्यांना सातत्याने ओव्हरलोड करणाऱ्या ब्रँड्सना सोडतात

- मागणी सिग्नल विकृती उत्पादन नियोजन त्रुटी निर्माण करते जे पुरवठा साखळीत पसरतात

- योजना गळती कारण वितरक इन्व्हेंटरी साफ करण्यासाठी अनधिकृत बाजारात अतिरिक्त स्टॉक वळवतात. याबद्दल आमच्या FMCG मध्ये योजना गळती प्रतिबंध या तपशीलवार मार्गदर्शकात अधिक वाचा

- ब्रँड इक्विटी क्षरण कारण मोठ्या सवलतीचा स्टॉक घाऊक बाजार आणि ऑनलाइन प्लॅटफॉर्मवर दिसून येतो

चॅनेल स्टफिंग कसे शोधावे

प्राथमिक निर्देशक हे प्राथमिक-ते-दुय्यम विक्री गुणोत्तर आहे. बहुतेक FMCG श्रेणींसाठी निरोगी गुणोत्तर 0.95 आणि 1.15 दरम्यान असते, म्हणजे वितरकांना विकल्या जाणाऱ्या प्रत्येक 100 रुपयांच्या वस्तूंसाठी, त्याच कालावधीत 87-105 रुपये किरकोळ विक्रेत्यांना पुढे विकले जातात (वितरक सुरक्षा स्टॉक संपवल्यास उच्च-मागणी कालावधीत गुणोत्तर 1 च्या खाली येऊ शकते).

सातत्याने 1.3 च्या वर असलेले प्राथमिक-ते-दुय्यम गुणोत्तर हे रेड फ्लॅग आहे. याचा अर्थ वितरक विकू शकतात त्यापेक्षा वेगाने इन्व्हेंटरी जमा करत आहेत. 1.5 च्या वरचे गुणोत्तर हे गंभीर चॅनेल स्टफिंग समस्या दर्शविते ज्यासाठी तातडीचा हस्तक्षेप आवश्यक आहे.

इतर चेतावणी चिन्हांमध्ये हे समाविष्ट आहे:

- वेगाने हलणाऱ्या SKU साठी वितरक दिवस-इन्व्हेंटरी (DOI) 25 दिवसांपेक्षा जास्त

- मागील तीन-महिन्यांच्या आधारावर परतावा दर 3% च्या वर चढत आहे

- प्रत्येक महिन्याच्या किंवा तिमाहीच्या शेवटच्या 5 दिवसांत प्राथमिक विक्रीत वाढ

- मानक कालावधीच्या पलीकडे विस्तारित क्रेडिट अटींची विनंती करणारे वितरक

- प्राथमिक विक्री वाढ दर्शवित असताना दुय्यम विक्री स्थिर किंवा घटत राहते

SpireStock त्याच्या सेल्स अॅनालिटिक्स मॉड्यूल द्वारे रिअल-टाइम प्राथमिक-ते-दुय्यम गुणोत्तर डॅशबोर्ड प्रदान करते, ब्रँड मॅनेजर्सना स्टफिंग पॅटर्न महाग समस्या बनण्यापूर्वी शोधण्यास सक्षम करते.

भारतात दुय्यम विक्री कशी ट्रॅक करावी

भारतात दुय्यम विक्री ट्रॅक करणे ही FMCG वितरणातील सर्वात आव्हानात्मक ऑपरेशनल समस्यांपैकी एक आहे. विकसित बाजारांच्या विपरीत जिथे इलेक्ट्रॉनिक POS सिस्टीम किरकोळ व्यवहार स्वयंचलितपणे कॅप्चर करतात, भारताच्या किरकोळ लँडस्केपवर 12+ दशलक्ष किराणा दुकानांचे वर्चस्व आहे जे किमान तंत्रज्ञान पायाभूत सुविधांसह कार्य करतात. हे वास्तव दुय्यम विक्री कॅप्चरला एक अनन्यसाधारण भारतीय समस्या बनवते ज्यासाठी भारत-विशिष्ट उपाय आवश्यक आहेत.

भारतात दुय्यम विक्री ट्रॅकिंग का कठीण आहे

अनेक संरचनात्मक घटक दुय्यम विक्री डेटा संकलन कठीण करतात:

- विखंडित किरकोळ विक्री, भारतात 12 दशलक्षाहून अधिक किराणा दुकाने आहेत, बहुतेकांकडे POS सिस्टीम, बारकोड स्कॅनर किंवा खरेदीचा डिजिटल रेकॉर्ड नाही

- रोख-जड व्यवहार, वितरकांकडून किराणा खरेदीच्या 60-70% रोख व्यवहार आहेत ज्यामध्ये हस्तलिखित बिले किंवा अजिबात बिले नाहीत

- प्रति किरकोळ विक्रेता अनेक वितरक, एक किराणा दुकान 15-25 वेगवेगळ्या वितरकांकडून खरेदी करू शकते, ज्यामुळे कोणत्याही एका स्रोताकडून संपूर्ण चित्र मिळणे अशक्य होते

- मर्यादित कनेक्टिव्हिटी, टियर-3 आणि टियर-4 शहरांमधील अनेक किरकोळ क्षेत्रांमध्ये असंगत इंटरनेट प्रवेश आहे

- डिजिटल स्वीकाराला विरोध, कर अनुपालन दृश्यमानतेच्या चिंतेमुळे वितरक आणि किरकोळ विक्रेते दोघेही तंत्रज्ञान स्वीकारण्यास विरोध करू शकतात

दुय्यम विक्री कॅप्चर करण्याच्या पद्धती

या आव्हानांना न जुमानता, भारतीय FMCG ब्रँडसने दुय्यम विक्री ट्रॅकिंगसाठी अनेक दृष्टिकोन विकसित केले आहेत, प्रत्येकाचे अचूकता, खर्च आणि स्केलेबिलिटीमध्ये वेगवेगळे ट्रेड-ऑफ आहेत:

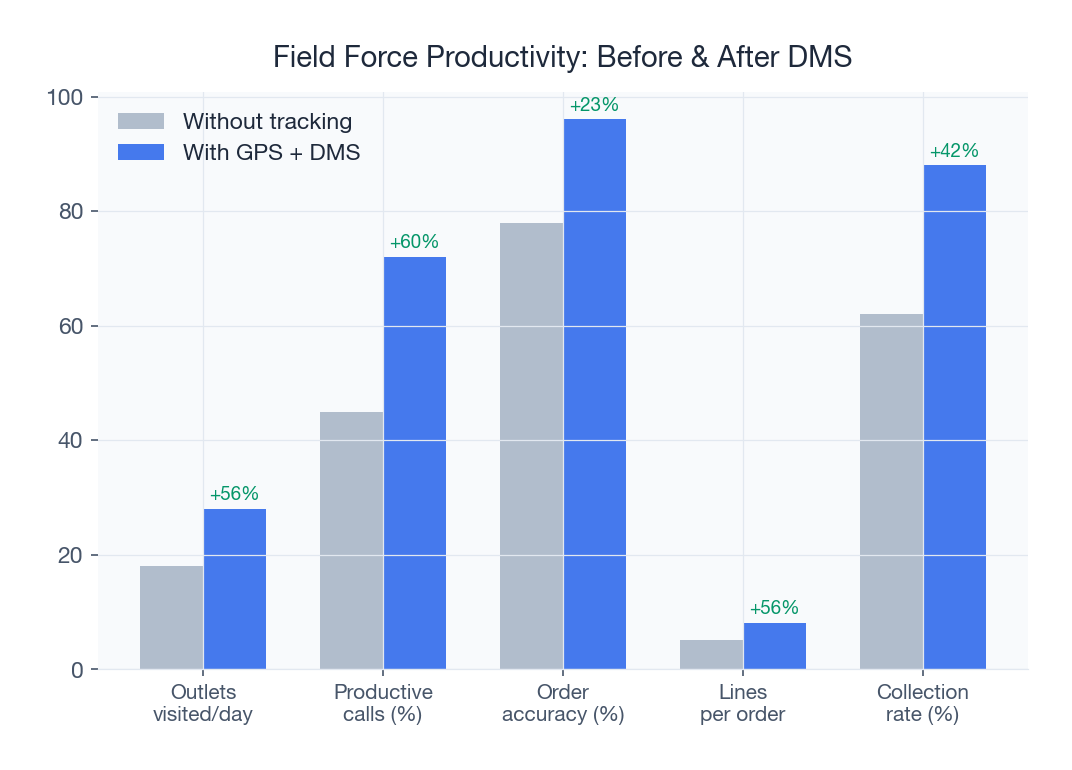

1. फील्ड फोर्स मोबाइल अॅप्स (सेल्समन-स्तरीय कॅप्चर)

बहुतेक भारतीय FMCG कंपन्यांसाठी सर्वात प्रभावी पद्धत म्हणजे वितरक सेल्समन (ऑर्डर बुकर्स) यांना मोबाइल अॅप सुसज्ज करणे जे किरकोळ स्तरावर ठेवलेली प्रत्येक ऑर्डर कॅप्चर करते. जेव्हा सेल्समन किराणा दुकानाला भेट देतो आणि ऑर्डर बुक करतो, तेव्हा अॅप SKU, प्रमाण, किरकोळ विक्रेता तपशील, GPS स्थान आणि टाइमस्टॅम्प रेकॉर्ड करते. हा डेटा रिअल टाइममध्ये ब्रँडकडे प्रवाहित होतो, वितरण नेटवर्कमधील दुय्यम विक्रीचे जवळजवळ-संपूर्ण चित्र प्रदान करतो.

SpireStock चे फील्ड फोर्स मोबाइल अॅप खराब कनेक्टिव्हिटी असलेल्या भागात ऑफलाइन कार्य करते आणि डिव्हाइस पुन्हा कनेक्ट झाल्यावर स्वयंचलितपणे सिंक होते. हे ग्रामीण आणि अर्ध-शहरी क्षेत्रांना त्रास देणारी कनेक्टिव्हिटी समस्या सोडवते. हजेरी आणि बीट ट्रॅकिंग सोबत एकत्रित केल्यावर, हे किती किरकोळ विक्रेत्यांना भेट दिली जात आहे, किती वारंवार आणि नियोजित बीट मार्ग पाळला जात आहे की नाही याची दृश्यमानता देखील प्रदान करते.

2. वितरक व्यवस्थापन प्रणाली (DMS) एकत्रीकरण

अनेक मोठे वितरक त्यांचे स्वतःचे बिलिंग सॉफ्टवेअर (Tally, Busy, Marg किंवा सानुकूल-निर्मित उपाय) वापरतात. API द्वारे या सिस्टीमशी एकत्रीकरण केल्याने ब्रँडना वितरक बिलांमधून थेट दुय्यम विक्री डेटा खेचण्यास परवानगी मिळते. हा दृष्टिकोन बिलिंग-स्तरीय अचूकता प्रदान करतो परंतु वितरक सहकार्य आणि सिस्टीम सुसंगततेवर अवलंबून असतो. SpireStock चे वितरण ट्रॅकिंग मॉड्यूल सर्व प्रमुख भारतीय बिलिंग प्लॅटफॉर्मसह API-आधारित एकत्रीकरणाला समर्थन देते.

3. किरकोळ विक्रेता बिलिंग कॅप्चर

काही ब्रँड उच्च-मूल्याच्या किरकोळ विक्रेत्यांना थेट टॅब्लेट किंवा बिलिंग अॅप्स प्रदान करतात, व्यवहाराच्या ठिकाणी खरेदी डेटा कॅप्चर करतात. हे संघटित किरकोळ विक्री आणि प्रीमियम आउटलेट्ससाठी चांगले कार्य करते परंतु लहान किराणा दुकानांच्या लांब शेपटीसाठी अव्यवहार्य आहे.

4. संकरित दृष्टिकोन

बहुतेक यशस्वी भारतीय FMCG ब्रँड पद्धतींचे संयोजन वापरतात, सामान्य व्यापारासाठी फील्ड फोर्स अॅप्स, मोठ्या वितरकांसाठी DMS एकत्रीकरण आणि आधुनिक व्यापारासाठी किरकोळ विक्रेता अॅप्स, सर्व एकत्रित अॅनालिटिक्स डॅशबोर्ड मध्ये फीड होतात जे एकत्रित दुय्यम विक्री चित्र प्रदान करते.

SpireStock दुय्यम विक्री ट्रॅकिंग कसे सोडवते

SpireStock भारतीय बाजारासाठी विशेष डिझाइन केलेल्या बहु-स्तरीय दृष्टिकोनातून दुय्यम विक्री कॅप्चर करते:

- मोबाइल-फर्स्ट ऑर्डर कॅप्चर, वितरक सेल्समन किरकोळ आउटलेट्सवर ऑर्डर बुक करण्यासाठी SpireStock अॅप वापरतात, व्यवहाराच्या ठिकाणी दुय्यम विक्री डेटा कॅप्चर करतात

- GPS-टॅग केलेल्या भेटी, प्रत्येक किरकोळ भेट जिओ-टॅग केली जाते, भेटीचा पुरावा प्रदान करते आणि किरकोळ विक्रेता ट्रॅकिंग द्वारे क्षेत्र कव्हरेज विश्लेषण सक्षम करते

- ऑफलाइन-फर्स्ट आर्किटेक्चर, अॅप इंटरनेट कनेक्टिव्हिटीशिवाय कार्य करते, डिव्हाइस पुन्हा कनेक्ट झाल्यावर डेटा सिंक करते, टियर-3 आणि ग्रामीण क्षेत्रांसाठी महत्त्वपूर्ण

- स्वयंचलित योजना अनुप्रयोग, दुय्यम विक्री डेटा थेट स्कीम इंजिन मध्ये प्रवाहित होतो, प्रत्यक्ष सेल-थ्रूवर आधारित अचूक प्रोत्साहन गणनेची खात्री देतो

- रिअल-टाइम डॅशबोर्ड, ब्रँड मॅनेजर्स महिन्याच्या शेवटी नाही तर रिअल टाइममध्ये क्षेत्र, वितरक आणि SKU मधील दुय्यम विक्री डेटा पाहतात

परिणाम म्हणजे तैनातीनंतर 4-6 आठवड्यांत वितरण नेटवर्कमध्ये 85-95% दुय्यम विक्री दृश्यमानता. तुमच्या विशिष्ट वितरण सेटअपसाठी ते कसे कार्य करते हे पाहण्यासाठी डेमोची विनंती करा.

प्राथमिक विरुद्ध दुय्यम विक्री: मुख्य फरक

प्राथमिक आणि दुय्यम विक्रीच्या संकल्पना सरळ वाटू शकतात, परंतु ऑपरेशनल परिणाम वितरण व्यवस्थापनाच्या प्रत्येक पैलूवर पसरतात. खालील सारणी 12 गंभीर परिमाणांमधील मुख्य फरकांचा सारांश देते जे भारतीय FMCG ब्रँडसने प्रत्येक प्रकारच्या विक्रीबद्दल कसा विचार करावा यावर परिणाम करतात.

| परिमाण | प्राथमिक विक्री | दुय्यम विक्री |

|---|---|---|

| कोण विकते | उत्पादक / ब्रँड | वितरक / सुपर स्टॉकिस्ट |

| कोण खरेदी करते | वितरक / C&F एजंट | किरकोळ विक्रेता / किराणा दुकान |

| डेटा उपलब्धता | 100% कॅप्चर केलेला (ब्रँड बिले) | DMS शिवाय सामान्यतः 20-40% |

| महसूल ओळख | ब्रँडद्वारे ओळखलेला | ब्रँड महसूल नाही (वितरक मार्जिन) |

| मागणी सिग्नल अचूकता | कमी (वितरक खरेदी प्रतिबिंबित करते, ग्राहक मागणी नाही) | उच्च (किरकोळ-स्तरीय पुल प्रतिबिंबित करते) |

| योजनांवर प्रभाव | वितरक लोडिंगला प्रोत्साहित करते | किरकोळ सेल-थ्रूला प्रोत्साहित करते |

| नियोजन प्रासंगिकता | उत्पादन नियोजन (काय उत्पादन करावे) | मागणी नियोजन (ग्राहकांना काय हवे आहे) |

| क्षेत्र अंतर्दृष्टी | वितरक-स्तरीय डेटापुरते मर्यादित | दाणेदार किरकोळ विक्रेता आणि बीट-स्तरीय डेटा |

| इन्व्हेंटरी दृश्यमानता | फक्त कारखाना आणि ट्रान्झिट स्टॉक | वितरक स्तरावर चॅनेल इन्व्हेंटरी |

| हंगाम शोध | लॅगिंग निर्देशक (2-4 आठवडे विलंबित) | लीडिंग निर्देशक (रिअल-टाइम मागणी बदल) |

| नवीन उत्पादन ट्रॅकिंग | फक्त प्रारंभिक पाइपलाइन भरणे दर्शविते | प्रत्यक्ष किरकोळ स्वीकृती आणि पुनरावृत्ती ऑर्डर दर्शविते |

| फसवणूक शोध | वळणाची मर्यादित दृश्यमानता | क्षेत्र उल्लंघन आणि स्टॉक वळवण्याचा शोध सक्षम करते |

मुख्य अंतर्दृष्टी अशी आहे की प्राथमिक विक्री डेटा आर्थिक अहवाल आणि पुरवठा साखळी लॉजिस्टिक्ससाठी आवश्यक आहे, परंतु बाजारातील वास्तव समजून घेण्यासाठी दुय्यम विक्री डेटा आवश्यक आहे. केवळ प्राथमिक डेटावर अवलंबून राहणारे ब्रँड एका कंपाससह नेव्हिगेट करत आहेत जो वितरक कुठे आहेत हे दर्शवितो, ग्राहक कुठे आहेत हे नाही. वितरण ट्रॅकिंग एंड-टू-एंड कसे कार्य करते याची सखोल समज मिळवण्यासाठी, SpireStock च्या वितरण ट्रॅकिंग वैशिष्ट्ये एक्सप्लोर करा.

चांगल्या निर्णय घेण्यासाठी दुय्यम विक्री डेटा वापरणे

एकदा तुमच्याकडे विश्वसनीय दुय्यम विक्री डेटा तुमच्या सिस्टीममध्ये प्रवाहित होऊ लागल्यानंतर, तो वितरण व्यवस्थापनाच्या प्रत्येक पैलूचे रूपांतर करतो. भारतीय FMCG ब्रँडसाठी सहा सर्वात प्रभावशाली अनुप्रयोग येथे आहेत.

1. मागणी अंदाज आणि उत्पादन नियोजन

दुय्यम विक्री डेटा FMCG उत्पादकांना उपलब्ध सर्वात अचूक मागणी सिग्नल प्रदान करतो. प्राथमिक ऑर्डरवर (ज्यात वितरक स्टॉकिंग वर्तन आणि प्रचारात्मक लोडिंग समाविष्ट आहे) उत्पादनाचा अंदाज लावण्याऐवजी, ब्रँड प्रत्यक्ष किरकोळ ऑफटेकवर आधारित अंदाज लावू शकतात. गुजरातमधील एका प्रादेशिक डेअरी ब्रँडने प्राथमिक-आधारित ते दुय्यम-आधारित मागणी नियोजनात बदल करून अंदाज त्रुटी 28% वरून 11% पर्यंत कमी केली, स्टॉकआउट्स आणि अतिउत्पादन दोन्ही कमी केले. SpireStock ची ऑर्डर व्यवस्थापन प्रणाली हंगाम, जाहिराती आणि क्षेत्र-विशिष्ट ट्रेंडसाठी जबाबदार असणारे मागणी अंदाज तयार करण्यासाठी दुय्यम विक्री पॅटर्न एकत्र करते.

2. क्षेत्र नियोजन आणि विस्तार

दुय्यम विक्री डेटा तुमची उत्पादने प्रत्यक्षात किरकोळ स्तरावर कुठे विकली जात आहेत हे प्रकट करतो, अचूक क्षेत्र नियोजन सक्षम करतो. तुम्ही पांढरे स्थान (वितरक उपस्थिती असूनही कमी किरकोळ प्रवेश असलेले क्षेत्र), ओव्हरलॅपिंग क्षेत्रे (समान किरकोळ विक्रेत्यांना सेवा देणारे अनेक वितरक) आणि उच्च-संभाव्य क्षेत्रे ओळखू शकता जे अतिरिक्त गुंतवणुकीचे समर्थन करतात. एका स्नॅक फूड्स कंपनीने दुय्यम विक्री मॅपिंगचा वापर करून शोधले की दिल्ली NCR मधील त्यांच्या 35% वितरकांचे ओव्हरलॅपिंग किरकोळ कव्हरेज होते, तर 20% बाजार पूर्णपणे अनकव्हर्ड होता.

3. योजना डिझाइन आणि ऑप्टिमायझेशन

दुय्यम विक्री डेटा ब्रँडना ट्रेड योजना डिझाइन करण्यास सक्षम करतो जे वितरक लोडिंगऐवजी प्रत्यक्ष सेल-थ्रूचे बक्षीस देतात. जेव्हा तुम्ही पाहू शकता की कोणते किरकोळ विक्रेते कोणते SKU कोणत्या वारंवारतेने खरेदी करत आहेत, तेव्हा तुम्ही लक्ष्यित योजना डिझाइन करू शकता जे केवळ इन्व्हेंटरी वेळ बदलण्याऐवजी वाढीव विक्री चालवतात. हा एक मूलभूत बदल आहे ज्याची आम्ही पुढील विभागात तपशीलवार चर्चा करतो.

4. वितरक कामगिरी मूल्यांकन

केवळ प्राथमिक विक्री मोठ्या ऑर्डर देणाऱ्या प्रत्येक वितरकाला टॉप परफॉर्मर म्हणून दाखवते. दुय्यम विक्री डेटा सत्य प्रकट करतो. 50 लाख रुपयांच्या मासिक ऑर्डर देणारा परंतु केवळ 35 लाख रुपयांची दुय्यम विक्री साध्य करणारा वितरक हा चॅनेल स्टफिंग जोखीम आहे. 30 लाख रुपये देणारा परंतु 32 लाख रुपयांची दुय्यम विक्री साध्य करणारा वितरक (सुरक्षा स्टॉक खाली खेचणारा) हा खरोखरच अधिक चांगली कामगिरी करत आहे आणि अधिक वाटप मिळण्यास पात्र आहे. SpireStock चे वितरक व्यवस्थापन प्लॅटफॉर्म संमिश्र कामगिरी स्कोअरकार्ड प्रदान करते जे दुय्यम विक्री, किरकोळ कव्हरेज, बीट पालन आणि वसुली कार्यक्षमतेला वजन देते.

5. नवीन उत्पादन लाँच ट्रॅकिंग

उत्पादन लाँच ही अशी जागा आहे जिथे प्राथमिक आणि दुय्यम डेटामधील अंतर सर्वात धोकादायक आहे. नवीन उत्पादन लाँच नेहमीच मजबूत प्राथमिक विक्री निर्माण करते कारण वितरक पाइपलाइन भरतात. हे प्रारंभिक लोडिंग किरकोळ स्तरावर संपूर्ण अपयश लपवू शकते. दुय्यम विक्री ट्रॅकिंगशिवाय, एका ब्रँडला 60-90 दिवसांनंतर वितरकांनी संपलेला स्टॉक परत करण्यास सुरुवात केल्याशिवाय त्यांचे नवीन उत्पादन ग्राहकांना विकले जात नाही हे शोधता येणार नाही. दुय्यम विक्री दृश्यमानतेसह, तुम्ही लाँचच्या पहिल्या 2-3 आठवड्यांत चाचणी दर, पुनरावृत्ती खरेदी पॅटर्न आणि क्षेत्र-स्तरीय स्वीकृती ट्रॅक करू शकता, तुम्हाला किंमत समायोजन, प्रचारात्मक समर्थन किंवा वितरण बदलांसह कोर्स-दुरुस्त करण्यासाठी वेळ देऊन.

6. क्रेडिट आणि संकलन ऑप्टिमायझेशन

वितरकाची ब्रँडला वेळेवर पैसे देण्याची क्षमता थेट किती लवकर ते किरकोळ विक्रेत्यांना माल विकू शकतात आणि पैसे गोळा करू शकतात याच्याशी जोडलेली आहे. दुय्यम विक्री वेग हा पेमेंट वर्तनाचा सर्वोत्तम अंदाज आहे. मजबूत दुय्यम विक्री आणि वेगवान किरकोळ संकलन असलेले वितरक कमी क्रेडिट जोखीम आहेत आणि त्यांना दीर्घ अटी दिल्या जाऊ शकतात. उच्च प्राथमिक खरेदी असूनही स्थिर दुय्यम विक्री असलेले वितरक हे संकलन जोखीम आहेत ज्यांचे सक्रियपणे व्यवस्थापन केले पाहिजे.

योजना जोडणी: दुय्यम विक्री डेटा सर्वकाही का बदलते

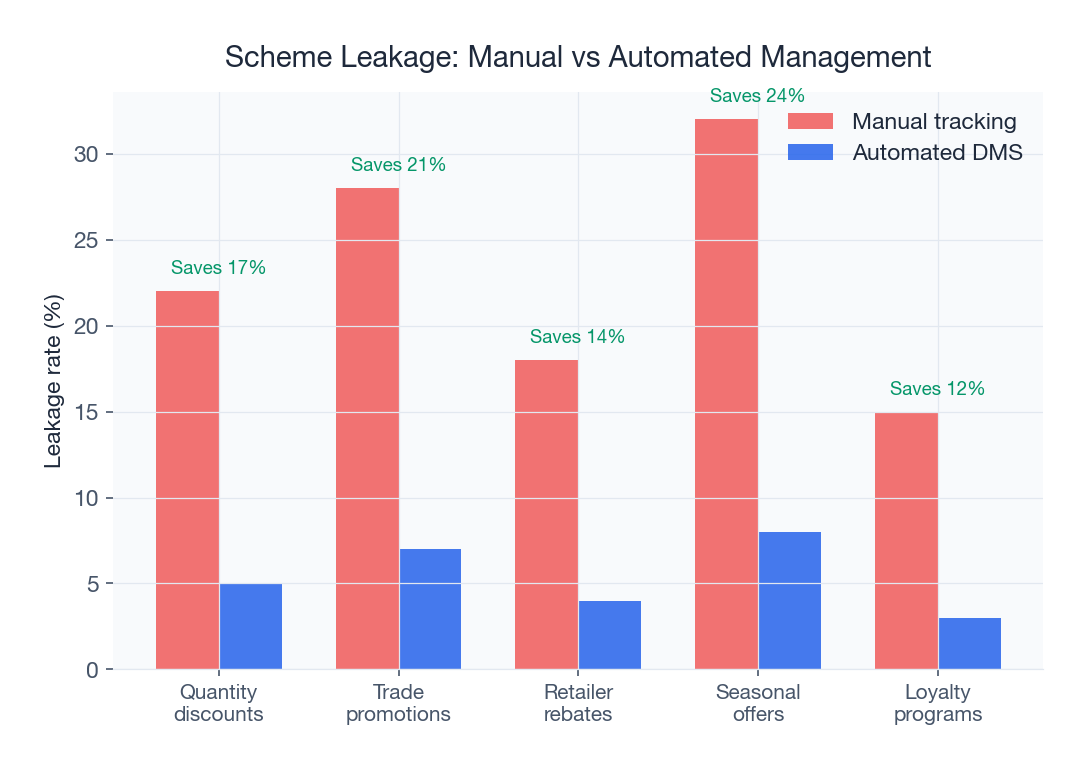

ट्रेड योजना ही भारतीय FMCG वितरणाचे इंधन आहेत. ब्रँड विविध योजना रचनांद्वारे ट्रेड प्रमोशनवर महसुलाच्या 8-15% खर्च करतात: प्रमाण सवलती, स्लॅब-आधारित प्रोत्साहन, हंगामी ऑफर, डिस्प्ले भत्ते आणि लक्ष्य-संबंधित बोनस. मूलभूत प्रश्न आहे: या योजना प्राथमिक विक्रीशी जोडल्या पाहिजेत की दुय्यम विक्रीशी?

प्राथमिक-संबंधित योजनांची समस्या

जेव्हा योजना प्राथमिक विक्रीशी (वितरकाची ब्रँडकडून खरेदी) जोडल्या जातात, तेव्हा प्रोत्साहन रचना खरेदी वर्तनाचे बक्षीस देते, विक्री वर्तनाचे नाही. 10 लाख रुपयांपेक्षा जास्त खरेदीवर 5% अतिरिक्त मार्जिन देणारी स्लॅब-आधारित योजना वितरकाला 10 लाख रुपयांची ऑर्डर देण्यास प्रवृत्त करते, किरकोळ मागणी त्या व्हॉल्यूमचे समर्थन करते की नाही याची पर्वा न करता. वितरक योजना लाभ कॅप्चर करतो, परंतु अतिरिक्त स्टॉक गोदामात बसतो आणि ब्रँड ग्राहक विक्रीत रूपांतरित न होणाऱ्या व्हॉल्यूमसाठी पैसे देतो.

प्राथमिक-संबंधित योजना दुष्ट चक्र निर्माण करतात: ब्रँड योजनांद्वारे व्हॉल्यूम ढकलतात, वितरक लाभ कॅप्चर करण्यासाठी लोड करतात, अतिरिक्त स्टॉकमुळे रस्त्यावरील किंमती घसरतात कारण वितरक इन्व्हेंटरी डंप करतात आणि ब्रँडला समान व्हॉल्यूम साध्य करण्यासाठी पुढील तिमाहीत आणखी खोल योजना आवश्यक असतात. या मॉडेलमधील योजना गळतीचा प्रत्येक रुपया हा भविष्यातील समस्या निर्माण करण्यावर खर्च केलेला रुपया आहे.

दुय्यम-संबंधित योजनांचा फायदा

जेव्हा योजना दुय्यम विक्रीशी जोडल्या जातात, तेव्हा प्रोत्साहन रचना प्रत्यक्ष किरकोळ सेल-थ्रूचे बक्षीस देते. वितरकाच्या किरकोळ विक्रेत्यांना केलेल्या विक्रीवर (ब्रँडकडून खरेदीवर नाही) आधारित अतिरिक्त मार्जिन देणारी स्लॅब-आधारित योजना वितरकाला किरकोळ कव्हरेज सुधारण्यासाठी, भेट वारंवारता वाढवण्यासाठी, स्टोअर स्तरावर मर्चेंडायझिंग ढकलण्यासाठी आणि शेल्फवर उपलब्धता सुनिश्चित करण्यासाठी प्रवृत्त करते. हे ब्रँडची प्रत्यक्षात वाढ करणारे वर्तन आहे.

दुय्यम-संबंधित योजनांनी सातत्याने दर्शविले आहे:

- योजना गळतीत 30-50% घट (लाभ कामगिरीकडे जातात, लोडिंगकडे नाही)

- किरकोळ संख्यात्मक वितरणात 15-20% सुधारणा (वितरक दुय्यम लक्ष्य गाठण्यासाठी आउटलेट कव्हरेज वाढवतात)

- परतावा आणि एक्सपायरी क्लेम्समध्ये 40-60% घट (अतिसाठा करण्यास प्रोत्साहन नाही)

- उच्च वितरक समाधान (बूम-बस्ट लोडिंग चक्र विरुद्ध शाश्वत कमाई)

प्राथमिक ते दुय्यम-संबंधित योजनांमध्ये कसे संक्रमण करावे

योजना जोडणी संक्रमण हा एक स्विच नाही जो तुम्ही रात्रभर फ्लिप करता. बहुतेक ब्रँड एक टप्प्याटप्प्याने दृष्टिकोन अनुसरण करतात:

- टप्पा 1 (महिने 1-3): वितरण नेटवर्कमध्ये दुय्यम विक्री ट्रॅकिंग तैनात करा. योजना बदल करण्यापूर्वी 80%+ डेटा कॅप्चर सुनिश्चित करा. SpireStock हे तैनातीच्या 4-6 आठवड्यांत साध्य करू शकते.

- टप्पा 2 (महिने 3-6): मिश्रित योजना सादर करा जिथे 50% लाभ प्राथमिक आणि 50% दुय्यम विक्रीशी जोडलेला आहे. हे वितरकांना प्रेरणा राखत वर्तन समायोजित करण्यास वेळ देते.

- टप्पा 3 (महिने 6-12): 70-80% दुय्यम जोडणीकडे स्थलांतर करा. टॉप-परफॉर्मिंग वितरक आधीच त्यांच्या केवळ-प्राथमिक स्तरांपेक्षा जास्त कमाई करत असतील. कमी कामगिरी करणाऱ्यांना समर्थन आणि प्रशिक्षण आवश्यक असेल.

- टप्पा 4 (महिना 12+): सर्व व्हेरिएबल योजनांसाठी पूर्ण दुय्यम जोडणीकडे जा. केवळ निश्चित ट्रेड मार्जिन आणि लॉजिस्टिक्स परतफेडीसाठी प्राथमिक-आधारित अटी राखा.

SpireStock चे स्कीम इंजिन रिअल-टाइम गणना आणि वितरकांसाठी पारदर्शक अहवालासह प्राथमिक आणि दुय्यम-संबंधित योजना कॉन्फिगरेशन दोन्हीला समर्थन देते. ही पारदर्शकता महत्त्वपूर्ण आहे, वितरक डेटावर विश्वास ठेवल्यासच दुय्यम-संबंधित योजना स्वीकारतील. योजना व्यवस्थापन क्षमतांसाठी आमचे किंमत योजना पहा.

दुय्यम विक्री दृश्यमानता: तंत्रज्ञान उपाय

दुय्यम विक्री दृश्यमानता साध्य करण्यासाठी योग्य तंत्रज्ञान स्टॅक आवश्यक आहे. भारतीय बाजार वेगाने विकसित झाला आहे, आणि दुय्यम विक्री डेटा कॅप्चर, प्रक्रिया आणि विश्लेषण करण्यासाठी अनेक श्रेणीतील साधने आता अस्तित्वात आहेत.

वितरण व्यवस्थापन प्रणाली (DMS)

DMS प्लॅटफॉर्म बहुतेक भारतीय FMCG कंपन्यांसाठी दुय्यम विक्री ट्रॅकिंगचा कणा बनवतात. DMS वितरक स्तरावर ऑर्डर, बिलिंग, इन्व्हेंटरी आणि पेमेंट कॅप्चर करते, वितरक आणि किरकोळ विक्रेता यांच्यातील प्रत्येक व्यवहाराचा डिजिटल रेकॉर्ड प्रदान करते. SpireStock सारखे सर्वोत्तम DMS प्लॅटफॉर्म, ऑर्डर व्यवस्थापन, वितरण ट्रॅकिंग आणि सेल्स अॅनालिटिक्स एका एकत्रित प्लॅटफॉर्ममध्ये एकत्र करतात जे भारतीय वितरण वास्तविकतेसाठी विशेष बनवले आहे. भारतातील वितरण व्यवस्थापन सॉफ्टवेअरचे संपूर्ण मार्गदर्शक मध्ये आमची सर्वसमावेशक तुलना वाचा.

सेल्स फोर्स ऑटोमेशन (SFA) साधने

SFA साधने फील्ड सेल्स प्रतिनिधींना मोबाइल अॅप्ससह सुसज्ज करतात जे किरकोळ भेटी, ऑर्डर आणि बाजार बुद्धिमत्ता कॅप्चर करतात. दुय्यम विक्री ट्रॅकिंगसाठी, SFA महत्त्वपूर्ण फर्स्ट-माईल डेटा कॅप्चर प्रदान करते. SpireStock चे मोबाइल अॅप DMS एकत्रीकरणासह SFA क्षमता एकत्र करते, डेटा सायलो तयार करणाऱ्या स्वतंत्र सिस्टीमची गरज दूर करते. फील्ड स्टाफ ऑर्डर कॅप्चर करू शकतो, हजेरी रेकॉर्ड करू शकतो, बीट योजना अनुसरण करू शकतो आणि बाजार फोटो अपलोड करू शकतो, सर्व एका अॅपवरून.

किरकोळ विक्रेता अॅप्स आणि स्व-ऑर्डरिंग पोर्टल

किरकोळ विक्रेत्यांना अॅप किंवा पोर्टलद्वारे थेट ऑर्डर देण्यास परवानगी देणे अतिरिक्त दुय्यम विक्री डेटा चॅनेल प्रदान करते आणि किरकोळ विक्रेता समाधान सुधारते. पारंपारिक व्यापारात प्रवेश कमी (8% पेक्षा कमी) असला तरी, तो शहरी बाजारात आणि तरुण किरकोळ विक्रेता डेमोग्राफिक्समध्ये वेगाने वाढत आहे. SpireStock सेल्समन-चालित ऑर्डर कॅप्चरसोबत पर्यायी चॅनेल म्हणून किरकोळ विक्रेता स्व-ऑर्डरिंगला समर्थन देते.

दुय्यम विक्रीसाठी एकत्रीकरण आर्किटेक्चर

दुय्यम विक्री दृश्यमानतेसाठी आदर्श तंत्रज्ञान स्टॅकमध्ये हे समाविष्ट आहे:

- किरकोळ आउटलेट्सवर सेल्समन-स्तरीय ऑर्डर कॅप्चरसाठी फील्ड फोर्स मोबाइल अॅप

- वितरक-स्तरीय बिलिंग आणि इन्व्हेंटरी व्यवस्थापनासाठी DMS प्लॅटफॉर्म

- रिअल-टाइम डॅशबोर्ड, प्राथमिक-ते-दुय्यम गुणोत्तर ट्रॅकिंग आणि क्षेत्र विश्लेषणासाठी अॅनालिटिक्स इंजिन

- दुय्यम विक्री डेटावर आधारित स्वयंचलित प्रोत्साहन गणनेसाठी स्कीम इंजिन

- ब्रँडच्या आर्थिक आणि उत्पादन नियोजन प्रणालींसह दुय्यम डेटा सिंक करण्यासाठी ERP एकत्रीकरण

SpireStock एका प्लॅटफॉर्ममध्ये पाचही घटक प्रदान करते, एकत्रीकरण समस्या दूर करते आणि संपूर्ण वितरण साखळीत डेटा सुसंगतता सुनिश्चित करते. अनेक श्रेणी किंवा प्रदेश व्यवस्थापित करणाऱ्या ब्रँडसाठी, वितरक व्यवस्थापन उपाय सर्व क्षेत्रांमध्ये एकत्रित दृश्य प्रदान करतो.

केस स्टडीज: दुय्यम विक्री ट्रॅकिंगद्वारे रूपांतरित झालेले ब्रँड

खालील केस स्टडीज विविध स्केलवरील भारतीय FMCG ब्रँडसना मजबूत दुय्यम विक्री ट्रॅकिंग सिस्टीम लागू करण्याचा कसा फायदा झाला आहे हे स्पष्ट करतात.

केस स्टडी 1: महाराष्ट्रातील प्रादेशिक डेअरी ब्रँड (180 कोटी रुपये महसूल)

महाराष्ट्रात 320 वितरक चालवणारी एक डेअरी कंपनी वार्षिक 12% प्राथमिक विक्री वाढीत होती, परंतु Nielsen कडील मार्केट शेअर डेटाने 8 पैकी 6 जिल्ह्यांमध्ये स्थिर किंवा घटणारा हिस्सा दर्शविला. हे विसंगती चिंताजनक होती: ब्रँड वितरकांना अधिक वस्तू पाठवत होता, परंतु त्या वस्तू ग्राहकांपर्यंत वेगाने पोहोचत नव्हत्या.

SpireStock चे मोबाइल अॅप त्यांच्या 450 सेल्समनच्या फील्ड फोर्सवर तैनात केल्यानंतर, ब्रँडने 5 आठवड्यांत 91% दुय्यम विक्री दृश्यमानता प्राप्त केली. डेटाने उघड केले की त्यांच्या वितरक नेटवर्कच्या 28% मध्ये प्राथमिक-ते-दुय्यम गुणोत्तर 1.4 पेक्षा जास्त होते, गंभीर चॅनेल स्टफिंग दर्शविते. तीन विशिष्ट समस्या उद्भवल्या: (a) योजना लाभ प्रमाणानुसार किरकोळ प्रयत्नांशिवाय कॅप्चर केले जात होते, (b) सक्रिय म्हणून सूचीबद्ध 15% किरकोळ विक्रेत्यांनी 60+ दिवसांत ऑर्डर दिलेली नव्हती, आणि (c) नवीन उत्पादन वितरण अहवालापेक्षा 40% कमी होते कारण सेल्समन नवीन उघडण्याऐवजी विद्यमान आउटलेट्सवर ऑर्डर बुक करत होते.

दुय्यम-संबंधित योजना आणि किरकोळ विक्रेता-स्तरीय ट्रॅकिंग लागू केल्याच्या दोन तिमाहींमध्ये, ब्रँडने DOI 28 दिवसांवरून 16 दिवसांपर्यंत कमी केले, परतावा 62% ने कमी केले आणि प्रभावी संख्यात्मक वितरण 23% ने वाढवले. 6 मागे पडलेल्या जिल्ह्यांमधील मार्केट शेअर सकारात्मक वाढ मार्गावर पुनर्प्राप्त झाला.

केस स्टडी 2: दक्षिण भारतातील बहु-श्रेणी FMCG वितरक (8 ब्रँड, 15,000 किरकोळ आउटलेट्स)

एका मोठ्या पुनर्वितरण स्टॉकिस्टने बंगळुरू, चेन्नई आणि हैदराबादमध्ये अन्न, वैयक्तिक काळजी आणि घरगुती काळजी श्रेणींमध्ये 8 FMCG ब्रँडसाठी वितरण व्यवस्थापित केले. प्रत्येक ब्रँडने वेगवेगळ्या स्वरूपात, वेगवेगळ्या वारंवारतेने आणि वेगवेगळ्या अहवाल प्रणालींद्वारे दुय्यम विक्री डेटाची मागणी केली. वितरकाच्या 12 लोकांच्या टीमने ब्रँड मुख्याध्यापकांसाठी दुय्यम विक्री अहवाल मॅन्युअली संकलित करण्यात त्यांचा 35% वेळ घालवला.

SpireStock च्या वितरक व्यवस्थापन प्लॅटफॉर्म वर एकत्रित केल्यानंतर, सर्व दुय्यम विक्री डेटा सेल्समन अॅपद्वारे स्वयंचलितपणे कॅप्चर केला गेला. स्वयंचलित अहवालाने 80% मॅन्युअल संकलन कार्य काढून टाकले, टीम सदस्यांना महसूल-निर्माण क्रियाकलापांसाठी मुक्त केले. अधिक महत्त्वाचे म्हणजे, वितरक आता ब्रँड मुख्याध्यापकांना कठीण डेटासह त्यांचे मूल्य दाखवू शकत होते, केवळ खरेदी व्हॉल्यूमऐवजी सिद्ध किरकोळ कामगिरीवर आधारित चांगले मार्जिन वाटाघाटी करू शकत होते. एका वर्षात, वितरकाने 8 वरून 12 ब्रँड भागीदारीमध्ये विस्तार केला, त्यांच्या डेटा-चालित दृष्टिकोनाला थेट वाढीचे श्रेय दिले.

केस स्टडी 3: नवीन क्षेत्रांमध्ये लाँच होणारा राष्ट्रीय स्नॅक फूड्स ब्रँड

5 नवीन राज्यांमध्ये त्याचा स्नॅक फूड्स पोर्टफोलिओ विस्तारित करणाऱ्या एका राष्ट्रीय FMCG ब्रँडला प्रारंभिक वितरक पाइपलाइन भरणे खरी किरकोळ ट्रॅक्शनमध्ये रूपांतरित होत आहे की नाही हे ट्रॅक करण्याची आवश्यकता होती. मागील लाँचमध्ये, ब्रँडने 2-3 महिने मजबूत प्राथमिक संख्या साजरी केली होती, त्यानंतर हे शोधले की किरकोळ सेल-थ्रू अपेक्षेपेक्षा 60% कमी होता, ज्या वेळी 4 कोटी रुपयांचा स्टॉक वितरक गोदामांमध्ये एक्सपायरीच्या जवळ येत होता.

नवीन लाँचसाठी, ब्रँडने एक कार्टन पाठवण्यापूर्वी सर्व लाँच वितरकांवर SpireStock तैनाती अनिवार्य केली. दुय्यम विक्री ट्रॅकिंग लाँचच्या दिवस 1 पासून सुरू झाली, चाचणी दर, पुनरावृत्ती ऑर्डर आणि किरकोळ विक्रेता स्तरावर श्रेणी-निहाय कामगिरीचे साप्ताहिक कोहोर्ट विश्लेषण प्रदान केले. आठवडा 3 पर्यंत, डेटाने दर्शविले की 5 पैकी 2 राज्यांमध्ये पुनरावृत्ती ऑर्डर दर 15% पेक्षा कमी होते (शाश्वत कामगिरीसाठी थ्रेशोल्ड), समस्या असह्य होण्यापूर्वी त्या बाजारात लक्ष्यित ग्राहक प्रचार आणि किरकोळ विक्रेता प्रोत्साहन तैनात करण्यास ब्रँडला सक्षम केले. हस्तक्षेपाने अंदाजे 2.8 कोटी रुपयांची संभाव्य परतावा वाचवली आणि ब्रँडवरील वितरक विश्वास जपला.

महत्त्वाचे मेट्रिक्स: वितरण आरोग्य मोजणे

दुय्यम विक्री डेटा कामगिरी मेट्रिक्सचा एक संच अनलॉक करतो जो FMCG ब्रँडना वितरण आरोग्यात दाणेदार दृश्यमानता देतो. प्रत्येक भारतीय ब्रँडने ट्रॅक करावयाचे दहा सर्वात महत्त्वाचे मेट्रिक्स येथे आहेत.

1. प्राथमिक-ते-दुय्यम विक्री गुणोत्तर

एकमेव सर्वात महत्त्वाचे वितरण आरोग्य मेट्रिक. गणना केली जाते: रोलिंग कालावधीवर प्राथमिक विक्री मूल्य / दुय्यम विक्री मूल्य (सामान्यतः 30 किंवा 90 दिवस). निरोगी श्रेणी 0.95-1.15 आहे. 1.3 च्या वर चॅनेल स्टफिंग सूचित करते. 0.9 च्या खाली संभाव्य पुरवठा कमतरता सूचित करते.

2. वितरकाकडे दिवस इन्व्हेंटरी (DOI)

वितरकाचा सध्याचा स्टॉक किती दिवसांची किरकोळ मागणी पूर्ण करू शकतो हे मोजते. गणना: (सध्याचे वितरक इन्व्हेंटरी मूल्य / सरासरी दैनिक दुय्यम विक्री मूल्य). इष्टतम DOI श्रेणीनुसार बदलते: डेअरी सारख्या नाशवंत वस्तूंसाठी 10-15 दिवस, सभोवतालच्या FMCG साठी 15-25 दिवस आणि हळू-हलणाऱ्या SKU साठी 25-40 दिवस.

3. फिल रेट

पहिल्या प्रयत्नात पूर्णपणे पूर्ण झालेल्या किरकोळ विक्रेता ऑर्डरची टक्केवारी. गणना: (पूर्ण वितरीत केलेल्या ओळी / एकूण ऑर्डर केलेल्या ओळी) x 100. सर्वोत्तम-इन-क्लास भारतीय FMCG ब्रँड 92-96% फिल रेट साध्य करतात. 85% च्या खाली महत्त्वपूर्ण पुरवठा साखळी किंवा इन्व्हेंटरी व्यवस्थापन समस्या दर्शविते.

4. प्रभावी स्टॉक-आउट सेकंद (ESOS)

स्टोअर महत्त्वानुसार वजन केलेले, ऑपरेटिंग तासांदरम्यान किरकोळ आउटलेट्सवर उत्पादन अनुपलब्ध असण्याचा एकूण कालावधी मोजते. पारंपारिक ESOS मापनासाठी इन-स्टोअर ऑडिटची आवश्यकता असली तरी, दुय्यम विक्री डेटा ऑर्डर अंतरांवर आधारित प्रॉक्सी गणना सक्षम करतो, जर दर 3 दिवसांनी ऑर्डर देणारा किरकोळ विक्रेता अचानक 9-दिवसांचे अंतर दर्शवत असेल, तर तो संभाव्य स्टॉक-आउट सूचित करतो.

5. वजनयुक्त वितरण

तुमचे उत्पादन साठवणाऱ्या आउटलेट्सद्वारे कव्हर केलेल्या एकूण बाजार विक्री व्हॉल्यूमची टक्केवारी मोजते, संख्यात्मक वितरणाच्या (आउटलेट्सची कच्ची संख्या) विरुद्ध. 40% वजनयुक्त वितरणासह 1,000 आउटलेट्समध्ये उपलब्ध असलेला ब्रँड 25% वजनयुक्त वितरणासह 2,000 आउटलेट्समधील ब्रँडपेक्षा अधिक चांगली कामगिरी करतो कारण तो अधिक मौल्यवान किरकोळ ठिकाणी उपस्थित आहे.

6. किरकोळ कॉल उत्पादकता

तुमच्या फील्ड फोर्सद्वारे प्रति किरकोळ भेट निर्माण होणारे सरासरी दुय्यम विक्री मूल्य. हजेरी आणि बीट ट्रॅकिंग मॉड्यूलद्वारे ट्रॅक केले जाते. स्थिर भेट संख्या असूनही घटणारी कॉल उत्पादकता मेट्रिक सूचित करते की सेल्समन आउटलेट्सना भेट देत आहेत परंतु भेटी ऑर्डरमध्ये प्रभावीपणे रूपांतरित करत नाहीत.

7. प्रति कॉल ओळी (LPC)

प्रति किरकोळ भेट ऑर्डर केलेल्या वेगळ्या SKU ची सरासरी संख्या. उच्च LPC फील्ड फोर्सद्वारे चांगली रेंज विक्री आणि क्रॉस-सेलिंग दर्शवते. 30 SKU असलेल्या ब्रँडसाठी, सामान्य व्यापारासाठी 4-6 चे LPC सामान्य आहे. 3 च्या खाली LPC सूचित करते की सेल्समन फक्त हीरो SKU ढकलत आहे आणि शेपटीकडे दुर्लक्ष करत आहे.

8. मस्ट-सेल लिस्ट (MSL) अनुपालन

ब्रँडच्या नियुक्त मस्ट-सेल SKU साठवणाऱ्या आउटलेट्सची टक्केवारी. जर तुमच्या MSL मध्ये 8 SKU असतील आणि सरासरी आउटलेट 5 साठवते, तर तुमचे MSL अनुपालन 62.5% आहे. हे मेट्रिक नवीन उत्पादने आणि धोरणात्मक SKU प्रस्थापित उच्च-विक्रेत्यांद्वारे बाहेर ढकलले जाण्याऐवजी पुरेसे वितरण साध्य करतात याची खात्री करण्यासाठी महत्त्वपूर्ण आहे.

9. सक्रिय आउटलेट टक्केवारी

गेल्या 30 दिवसांत (किंवा हळू-हलणाऱ्या श्रेणींसाठी 60 दिवस) किमान एक ऑर्डर दिलेल्या सूचीबद्ध किरकोळ आउटलेट्सची टक्केवारी. घटणारी सक्रिय आउटलेट टक्केवारी वितरण क्षरण सूचित करते जे केवळ प्राथमिक विक्री डेटा प्रकट करणार नाही. वैयक्तिक स्टोअर स्तरावर आउटलेट क्रियाकलापाचे निरीक्षण करण्यासाठी किरकोळ विक्रेता ट्रॅकिंग वापरा.

10. क्लेम-ते-विक्री गुणोत्तर

दुय्यम विक्रीच्या टक्केवारीनुसार वितरक क्लेम्सचे मूल्य (परतावा, एक्सपायरी, नुकसान, कमी वितरण). निरोगी गुणोत्तर 1.5% पेक्षा कमी आहे. 3% च्या वर विशिष्ट कारणांची चौकशी आवश्यक आहे. हे मेट्रिक चॅनेल स्टफिंग आणि इन्व्हेंटरी व्यवस्थापन समस्यांचा डाउनस्ट्रीम निर्देशक आहे.

SpireStock चे अॅनालिटिक्स डॅशबोर्ड कॉन्फिगर करण्यायोग्य अलर्ट्स आणि राष्ट्रीय स्तरापासून वैयक्तिक किरकोळ विक्रेता स्तरापर्यंत ड्रिल-डाउन क्षमतेसह रिअल टाइममध्ये सर्व दहा मेट्रिक्स ट्रॅक करते. फील्ड फोर्स उत्पादकता व्यवस्थापित करणाऱ्या ब्रँडसाठी, हे मेट्रिक्स जबाबदारी चालविण्यासाठी आवश्यक KPI प्रदान करतात.

दुय्यम विक्री संस्कृती तयार करणे

केवळ तंत्रज्ञान दुय्यम विक्री दृश्यमानता समस्या सोडवत नाही. ब्रँडसने एक संघटनात्मक संस्कृती तयार केली पाहिजे जी प्राथमिक विक्री व्हॅनिटी मेट्रिक्सपेक्षा दुय्यम विक्री डेटाला महत्त्व देते. यासाठी अनेक स्तरांवर बदल आवश्यक आहेत:

- नेतृत्व संरेखन: वरिष्ठ नेतृत्वाने दुय्यम विक्री मेट्रिक्सवर कामगिरी पुनरावलोकने आणि प्रोत्साहन रचना अँकर करणे आवश्यक आहे. जर CEO अजूनही प्राथमिक विक्री मैलाचा दगड साजरा करत असेल, तर संस्था लोडिंगसाठी ऑप्टिमाइझ करत राहील.

- ASM आणि RSM प्रोत्साहन: क्षेत्र आणि प्रादेशिक सेल्स मॅनेजर प्रोत्साहनांचे किमान 50% दुय्यम विक्री उपलब्धी, प्राथमिक-ते-दुय्यम गुणोत्तर आणि वितरण गुणवत्ता मेट्रिक्सशी जोडलेले असावे.

- वितरक भागीदारी: वितरकांना केवळ प्राथमिक ऑफटेकसाठी ग्राहक नव्हे तर दुय्यम विक्री उपलब्धीतील भागीदार म्हणून वागवले पाहिजे. दुय्यम विक्री डेटा पारदर्शकपणे सामायिक करा आणि किरकोळ सेल-थ्रू लक्ष्यांभोवती संयुक्त व्यवसाय योजना डिझाइन करा.

- क्रॉस-फंक्शनल वापर: दुय्यम विक्री डेटा मार्केटिंग (मोहीम ROI), वित्त (प्राप्ती अंदाज), पुरवठा साखळी (मागणी नियोजन) आणि R&D (उत्पादन कामगिरी ट्रॅकिंग) मध्ये फीड व्हावा, केवळ विक्री कार्यात सायलोड राहू नये.

हे संक्रमण यशस्वीरित्या करणारे ब्रँड केवळ चांगले वितरण मेट्रिक्स नव्हे तर मजबूत वितरक संबंध, कमी कार्यरत भांडवल आवश्यकता आणि अधिक अंदाजे महसूल वाढ नोंदवतात. संक्रमण दृश्यमानतेपासून सुरू होते, आणि दृश्यमानता योग्य तंत्रज्ञान प्लॅटफॉर्मपासून सुरू होते. तुमच्या ब्रँडसाठी दुय्यम विक्री दृश्यमानता तयार करण्याबद्दल SpireStock शी बोला.

निष्कर्ष: भविष्य दुय्यम विक्री-चालित ब्रँडचे आहे

प्राथमिक आणि दुय्यम विक्रीतील फरक हा केवळ व्याख्यात्मक व्यायाम नाही. ही त्यांच्या बाजाराची समज असणारे ब्रँड आणि आंधळेपणाने उडणारे ब्रँड यांच्यातील विभाजक रेषा आहे. भारताच्या अनन्यसाधारणपणे जटिल FMCG लँडस्केपमध्ये, त्याच्या 12 दशलक्ष किराणा दुकाने, खंडित वितरण नेटवर्क आणि वेगाने विकसित होणाऱ्या चॅनेल मिक्ससह, दुय्यम विक्री दृश्यमानता ही एक ब्रँड गुंतवणूक करू शकणारी सर्वात प्रभावशाली क्षमता आहे.

दुय्यम विक्री ट्रॅक करणारे ब्रँड मागणीचा अचूक अंदाज लावू शकतात, खऱ्या कामगिरीला बक्षीस देणाऱ्या योजना डिझाइन करू शकतात, चॅनेल समस्या लवकर शोधू शकतात, वितरकांचे न्याय्यपणे मूल्यांकन करू शकतात आणि आत्मविश्वासाने उत्पादने लाँच करू शकतात. केवळ प्राथमिक डेटावर अवलंबून असलेले ब्रँड 10 कोटी रुपयांच्या माहितीवर आधारित 100 कोटी रुपयांचे निर्णय घेत आहेत.

भारतात दुय्यम विक्री डेटा कॅप्चर करण्याचे तंत्रज्ञान आता परिपक्व, परवडणारे आणि स्केलवर सिद्ध झालेले आहे. SpireStock सारखे प्लॅटफॉर्म कारखाना डिस्पॅचपासून ते किरकोळ शेल्फपर्यंत एंड-टू-एंड दृश्यमानता प्रदान करतात, भारतीय बाजाराला आवश्यक असलेल्या मोबाइल-फर्स्ट, ऑफलाइन-सक्षम, योजना-जागरूक आर्किटेक्चरसह. तुम्ही 50 कोटी रुपयांचा प्रादेशिक ब्रँड असाल किंवा 5,000 कोटी रुपयांचा राष्ट्रीय खेळाडू, दुय्यम विक्री दृश्यमानतेचा ROI तैनातीच्या पहिल्या तिमाहीत मोजता येतो.

तुमचे वितरण नेटवर्क प्रत्यक्षात कसे दिसते हे पाहण्यासाठी तयार आहात का? SpireStock ची तुमची मोफत 30-दिवसांची चाचणी सुरू करा आणि तुमच्या वितरण नेटवर्कमध्ये संपूर्ण दुय्यम विक्री दृश्यमानता मिळवा. आमची सेल्स अॅनालिटिक्स, ऑर्डर व्यवस्थापन आणि वितरण ट्रॅकिंग क्षमता एक्सप्लोर करा किंवा तुमच्या ब्रँडसाठी योग्य फिट शोधण्यासाठी आमच्या किंमत योजना तपासा.

तुमचा चॅनेल काय करत आहे याचा अंदाज लावणे थांबवा. SpireStock तुम्हाला प्रत्येक वितरक, प्रत्येक क्षेत्र आणि प्रत्येक SKU मध्ये रिअल-टाइम दुय्यम विक्री डेटा देते, जेणेकरून तुम्ही वितरक काय ऑर्डर करत आहेत यावर नव्हे तर ग्राहक प्रत्यक्षात काय खरेदी करत आहेत यावर आधारित निर्णय घेऊ शकता. आज तुमचा मोफत डेमो बुक करा.

स्रोत आणि संदर्भ

- Nielsen India, Retail Intelligence and FMCG Distribution Report

- RedSeer Consulting, India FMCG Channel Economics Report 2025

- IBEF, India Brand Equity Foundation, FMCG Sector Overview

- FICCI, Federation of Indian Chambers of Commerce and Industry, FMCG Distribution

वारंवार विचारले जाणारे प्रश्न

प्राथमिक विक्री म्हणजे उत्पादक किंवा ब्रँडकडून वितरकाकडे होणारे व्यवहार. दुय्यम विक्री म्हणजे वितरकाकडून किरकोळ विक्रेत्याकडे होणारे व्यवहार. प्राथमिक विक्री वितरकांनी ब्रँडकडून काय खरेदी केले हे प्रतिबिंबित करते, तर दुय्यम विक्री किरकोळ स्तरावर प्रत्यक्षात काय विकले जात आहे हे प्रतिबिंबित करते. ग्राहक मागणीचे दुय्यम विक्री हे अधिक अचूक निर्देशक आहे.

दुय्यम विक्री ट्रॅकिंग प्रत्यक्ष किरकोळ मागणी प्रकट करते, चॅनेल स्टफिंग प्रतिबंधित करते, अचूक मागणी अंदाज सक्षम करते आणि ब्रँडना खऱ्या सेल-थ्रूला बक्षीस देणाऱ्या योजना डिझाइन करण्याची परवानगी देते. त्याशिवाय, ब्रँड प्राथमिक विक्री डेटावर अवलंबून असतात जे घटणारा मार्केट शेअर लपवू शकतो आणि वितरण नेटवर्कमध्ये महाग इन्व्हेंटरी समस्या निर्माण करू शकतो.

चॅनेल स्टफिंग म्हणजे किरकोळ मागणीच्या पलीकडे वितरकांना अतिरिक्त इन्व्हेंटरी ढकलण्याची प्रथा, सामान्यतः अल्प-मुदतीची प्राथमिक विक्री लक्ष्ये पूर्ण करण्यासाठी. हे प्राथमिक-ते-दुय्यम विक्री गुणोत्तराचे निरीक्षण करून शोधले जाते. सातत्याने 1.3 च्या वर असलेले गुणोत्तर हे रेड फ्लॅग आहे, तर 1.5 च्या वर तातडीच्या हस्तक्षेपाची आवश्यकता असलेली गंभीर समस्या दर्शवते.

सर्वात प्रभावी पद्धतींमध्ये किरकोळ आउटलेट्सवर ऑर्डर कॅप्चर करणारे फील्ड फोर्स मोबाइल अॅप्स, वितरक बिलिंग सॉफ्टवेअरसह DMS एकत्रीकरण आणि किरकोळ विक्रेता स्व-ऑर्डरिंग पोर्टल समाविष्ट आहेत. SpireStock ऑफलाइन क्षमता, GPS-टॅग केलेल्या भेटी आणि रिअल-टाइम अॅनालिटिक्ससह एका प्लॅटफॉर्मवर तीनही दृष्टिकोन एकत्र करते.

योजना आदर्शपणे दुय्यम विक्रीशी जोडल्या पाहिजेत. प्राथमिक-संबंधित योजना वितरक लोडिंग आणि चॅनेल स्टफिंगला प्रोत्साहन देतात. दुय्यम-संबंधित योजना प्रत्यक्ष किरकोळ सेल-थ्रूला प्रोत्साहन देतात, योजना गळती 30-50% ने कमी करतात आणि परतावा 40-60% ने कमी करतात. बहुतेक ब्रँड 6-12 महिन्यांत हळूहळू संक्रमण करतात.

बहुतेक FMCG श्रेणींसाठी निरोगी प्राथमिक-ते-दुय्यम गुणोत्तर 0.95 आणि 1.15 दरम्यान असते. याचा अर्थ वितरकांना विकल्या जाणाऱ्या प्रत्येक 100 रुपयांच्या वस्तूंसाठी, त्याच कालावधीत 87-105 रुपये किरकोळ विक्रेत्यांना पुढे विकले जातात. 1.3 च्या वर गुणोत्तर चॅनेल स्टफिंग सूचित करते, तर 0.9 च्या खाली पुरवठा कमतरता सूचित करू शकते.

तृतीयक विक्री म्हणजे किरकोळ विक्रेता आणि अंतिम ग्राहक यांच्यातील अंतिम व्यवहार. हा प्रत्यक्ष उपभोगाचा क्षण आहे. तृतीयक विक्री डेटा हा सर्वात अचूक मागणी सिग्नल असला तरी, POS सिस्टीमशिवाय असंघटित किराणा किरकोळ विक्रीच्या वर्चस्वामुळे भारतात कॅप्चर करणे सर्वात कठीण आहे.

SpireStock ऑफलाइन क्षमतेसह मोबाइल-फर्स्ट फील्ड फोर्स अॅप, प्रमुख बिलिंग प्लॅटफॉर्मसह DMS एकत्रीकरण, GPS-टॅग केलेल्या किरकोळ भेटी, दुय्यम डेटावर आधारित स्वयंचलित योजना गणना आणि रिअल-टाइम अॅनालिटिक्स डॅशबोर्डद्वारे दुय्यम विक्री कॅप्चर करते. ब्रँड सामान्यतः तैनातीच्या 4-6 आठवड्यांत 85-95% दुय्यम विक्री दृश्यमानता प्राप्त करतात.

संबंधित SpireStock वैशिष्ट्ये

संबंधित उद्योग

संबंधित उपाय

तुमचे संपूर्ण distributor नेटवर्क डिजिटली व्यवस्थापित करा. ऑनबोर्डिंग, क्रेडिट मर्यादा, थकबाकी ट्रॅकिंग आणि कामगिरी विश्लेषण.

तुमचे रिटेल नेटवर्क ट्रॅक आणि व्यवस्थापित करा. आउटलेट जिओ-टॅग करा, दुय्यम विक्री कॅप्चर करा, बीट व्यवस्थापित करा.

बीट नियोजन, GPS उपस्थिती, ऑर्डर कॅप्चर आणि कामगिरी विश्लेषणासह मैदान विक्री टीमची उत्पादकता वाढवा.

संबंधित संस्था

तुमचे वितरण सुव्यवस्थित करण्यास तयार आहात?

तुमची 30 दिवसांची मोफत चाचणी सुरू करा आणि पहा की SpireStock तुमचे डेअरी, FMCG किंवा ग्राहक वस्तू वितरण ऑर्डरपासून क्रेट रिकव्हरीपर्यंत कसे बदलू शकते.

SpireStock Team

डिस्ट्रिब्युशन टेक्नॉलॉजी तज्ज्ञ

SpireStock Team SpireStock साठी डिस्ट्रिब्युशन मॅनेजमेंट, सप्लाय-चेन ऑप्टिमायझेशन आणि भारतीय डेअरी व FMCG ब्रँड्ससाठीच्या फील्ड ऑपरेशन्सवर लिहिते.