Why E-Way Bills Are Uniquely Complex for Dairy and FMCG Distributors

Dairy and FMCG distributors across Pune, Ahmedabad, Mumbai, and every major Indian city face an e-way bill challenge that other industries simply do not encounter. Their delivery vehicles carry a mix of GST-exempt products (fresh milk at 0%), low-GST products (packaged dairy at 5%), and standard-GST products (butter and cheese at 12%, ice cream at 18%). A single delivery van leaving the godown at 5 AM might carry products spanning four different GST rates, some requiring e-way bills and some fully exempt. Figuring out which consignments need e-way bills, calculating thresholds correctly for mixed loads, and generating 40-80 bills daily before vehicles depart is a compliance nightmare that costs distributors lakhs in staff time, penalties, and spoiled goods every year.

Add to this the volume problem: a mid-sized dairy distributor dispatches 40-80 consignments per day across multiple routes. Generating individual e-way bills for each consignment while accounting for exemptions and mixed loads becomes a full-time job for one or more dedicated staff members. This is where automation through a distribution management system becomes not just convenient but essential for survival.

What Is an E-Way Bill and When Is It Required?

An e-way bill (Electronic Way Bill) is a digital document mandated under India's GST framework for the movement of goods valued above Rs 50,000. Generated on the NIC (National Informatics Centre) portal at ewaybillgst.gov.in, it contains details of the goods being transported, the consignor (sender), consignee (receiver), and transporter. The e-way bill must accompany goods during transit and can be verified by GST authorities at any checkpost, highway inspection point, or during a random vehicle check.

Key threshold rules every dairy and FMCG distributor must know:

- Inter-state movement: Mandatory for goods valued above Rs 50,000 (calculated on invoice value including tax)

- Intra-state movement: Mandatory above Rs 50,000 in most states, though some states have different thresholds

- Validity: 1 day for every 200 km of transit distance (100 km for over-dimensional cargo)

- Generation responsibility: Can be generated by the consignor, consignee, or registered transporter

- Part A and Part B: Part A contains goods and party details (from invoice data). Part B contains vehicle number and transport details. Both parts must be complete before goods move.

For FMCG distributors handling hundreds of SKUs across multiple GST slabs, the complexity is not in understanding these rules but in applying them correctly across thousands of monthly consignments without error.

Complete Dairy Product Exemption Table

Not all dairy products require e-way bills. Products classified under 0% GST (nil-rated) are exempt from e-way bill requirements regardless of consignment value. This exemption is critical for dairy distributors because a significant portion of daily dispatches may consist entirely of exempt products. Here is the complete classification:

| Product | HSN Code | GST Rate | E-Way Bill Required? | Key Condition |

|---|---|---|---|---|

| Fresh milk (unprocessed) | 0401 | 0% | No (exempt) | Must be unbranded, unpackaged |

| Pasteurized milk (loose) | 0401 | 0% | No (exempt) | Sold without brand name |

| Curd (unbranded) | 0403 | 0% | No (exempt) | Not pre-packaged or labelled |

| Lassi (unbranded) | 0403 | 0% | No (exempt) | Not pre-packaged or labelled |

| Buttermilk (unbranded) | 0403 | 0% | No (exempt) | Not pre-packaged or labelled |

| Paneer (unbranded) | 0406 | 0% | No (exempt) | Not pre-packaged or labelled |

| UHT milk (branded/packaged) | 0401 | 5% | Yes, if above Rs 50,000 | Pre-packaged and labelled |

| Packaged curd (branded) | 0403 | 5% | Yes, if above Rs 50,000 | Pre-packaged and labelled |

| Milk powder (branded) | 0402 | 5% | Yes, if above Rs 50,000 | Pre-packaged and labelled |

| Flavoured milk | 0402 | 12% | Yes, if above Rs 50,000 | All variants taxable |

| Cheese | 0406 | 12% | Yes, if above Rs 50,000 | All variants taxable |

| Butter | 0405 | 12% | Yes, if above Rs 50,000 | All variants taxable |

| Ghee | 0405 | 12% | Yes, if above Rs 50,000 | All variants taxable |

| Condensed milk | 0402 | 12% | Yes, if above Rs 50,000 | All variants taxable |

| Ice cream | 2105 | 18% | Yes, if above Rs 50,000 | All variants taxable |

The 2022 GST Council decision to tax pre-packaged and labelled dairy products (curd, lassi, buttermilk, paneer) at 5% significantly increased the e-way bill burden for dairy distributors. Products that were previously all exempt now require careful classification based on packaging and branding. For full GST rate guidance, read our GST billing guide for dairy distribution.

The Mixed Load Problem: Calculating Thresholds Correctly

The real compliance complexity arises when a single delivery vehicle carries both exempt and taxable products, which is the default scenario for most dairy distributors. Consider a typical delivery van dispatched from a godown in Pune:

- Fresh milk pouches (0% GST, exempt): Rs 80,000

- Branded UHT milk (5% GST): Rs 25,000

- Butter and cheese (12% GST): Rs 35,000

- Ice cream (18% GST): Rs 20,000

Total consignment value: Rs 1,60,000. But the exempt portion (Rs 80,000) should not be counted toward the Rs 50,000 e-way bill threshold. The taxable portion (Rs 80,000) exceeds the threshold, so an e-way bill is required, but only because the taxable goods cross Rs 50,000.

Now consider another van carrying Rs 1,20,000 of fresh milk (exempt) and Rs 40,000 of branded curd (5% GST). Total value is Rs 1,60,000, but the taxable portion is only Rs 40,000, which is below the Rs 50,000 threshold. No e-way bill is required despite the high total value. Getting this calculation wrong in either direction creates problems: unnecessary e-way bills waste time, while missing required e-way bills invite penalties.

Consolidated E-Way Bills for Multi-Drop Routes

A dairy delivery van making 40-60 drops per route does not need individual e-way bills for each retailer delivery. Instead, a consolidated e-way bill can cover multiple consignments loaded on the same vehicle. The consolidated bill references individual e-way bills (one per consignment above the threshold) and serves as the master document for the vehicle. This dramatically reduces the documentation burden while maintaining full compliance. The billing module in a DMS auto-generates consolidated bills as part of the dispatch workflow.

Part-B Updates: Handling Vehicle Changes Mid-Route

One of the most frequently violated e-way bill requirements is the Part-B update when a vehicle changes. In dairy distribution, vehicle changes happen regularly: a van breaks down and goods are transferred to another vehicle, a route is split between two vans due to volume, or goods are transshipped at a hub. Every such change requires updating Part B of the e-way bill with the new vehicle number before the goods continue moving.

Manual operations miss this update routinely because the driver and dispatcher are focused on getting perishable products delivered, not on compliance paperwork. A DMS with distribution tracking detects vehicle reassignments automatically and triggers Part-B updates via the NIC API, ensuring compliance without manual intervention.

State-Specific E-Way Bill Rules for Dairy Distributors

While the central e-way bill framework is uniform, several states have implemented variations that affect dairy and FMCG distributors:

| State | Intra-State Threshold | Special Rules for Dairy/FMCG | Enforcement Level |

|---|---|---|---|

| Maharashtra | Rs 50,000 | Standard rules; high checkpost density on Mumbai-Pune corridor | High |

| Gujarat | Rs 50,000 | Additional cooperative sector exemptions for milk movements | Medium-High |

| Karnataka | Rs 50,000 | Standard rules; active enforcement on NH-44 and NH-48 | High |

| Kerala | Rs 50,000 | Stricter enforcement; highest checkpost density in South India | Very High |

| Tamil Nadu | Rs 50,000 | Standard rules; e-way bill verification at toll plazas | High |

| Uttar Pradesh | Rs 50,000 | Active highway verification; common detention on NH-2 and NH-24 | High |

| Rajasthan | Rs 50,000 | Standard rules; lower enforcement in rural routes | Medium |

| Madhya Pradesh | Rs 50,000 | Standard rules | Medium |

| West Bengal | Rs 50,000 | State-level e-way bill portal integration for intra-state | Medium-High |

| Telangana | Rs 50,000 | Standard rules; enforcement focused on inter-state routes | Medium |

Distributors operating in Chennai, Kolkata, or Hyderabad with inter-state supply chains face compounded complexity as goods cross state borders. A DMS that auto-applies state-specific rules eliminates the risk of compliance errors when dispatching to different states.

Penalties for E-Way Bill Violations: The Real Cost

E-way bill violations carry penalties that are particularly devastating for perishable product distributors:

- Missing e-way bill: Penalty of Rs 10,000 or the applicable tax amount, whichever is higher. For a consignment of Rs 1 lakh at 12% GST, this means Rs 12,000 minimum.

- Expired e-way bill: Same penalty as missing e-way bill. E-way bills that expire during transit (common during monsoon delays or traffic jams in cities like Mumbai) are treated as violations.

- Vehicle detention: Vehicle and goods are detained at the checkpost until the penalty is paid and the violation is rectified. Release can take 4-24 hours depending on the state and the officer.

- Perishable product spoilage: For dairy products, even a 6-12 hour detention at a checkpost during summer can result in spoilage of the entire consignment. A Rs 10,000 penalty can escalate to Rs 1-2 lakh in total loss when you factor in spoiled goods.

- Repeated violations: Trigger GST scrutiny, audit notices, and potential investigation of the distributor's overall compliance. Three or more violations in a quarter raise red flags in the GST system.

For a dairy distributor carrying Rs 1-2 lakh worth of perishable products, a single e-way bill violation can cost Rs 10,000 in penalty plus Rs 1-2 lakh in spoiled goods, plus the lost sales from undelivered orders. The total loss from one incident can exceed the annual cost of DMS automation.

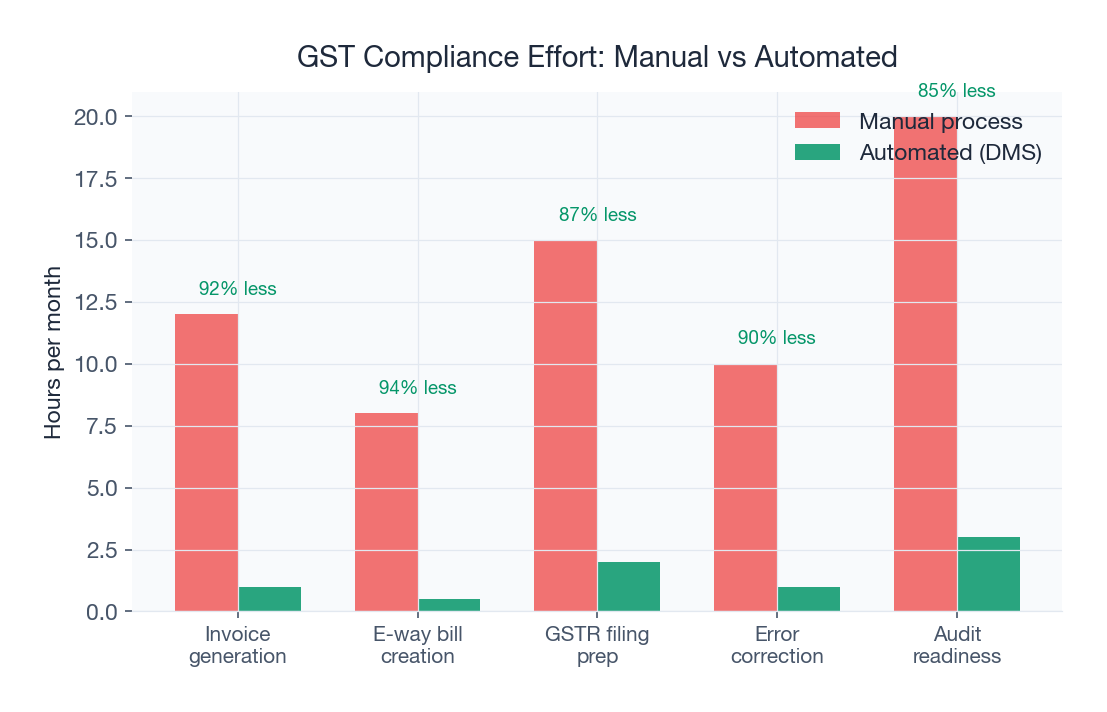

Automating E-Way Bills Through Distribution Software

Here is how a modern billing and invoicing system automates the complete e-way bill workflow:

- Invoice generation and classification: As invoices are created for each delivery, the system auto-classifies every line item by HSN code, GST rate, and exemption status. Mixed-load invoices are handled seamlessly.

- Automatic threshold calculation: The system calculates the taxable consignment value per vehicle, excluding exempt items, and determines whether an e-way bill is required. No manual calculation, no errors.

- API-based auto-generation: For consignments requiring e-way bills, the system generates them via direct NIC API integration. Part A is populated from invoice data; Part B is populated from the vehicle assignment in route optimization.

- Consolidated bill creation: For vehicles with multiple consignments above threshold, consolidated e-way bills are auto-generated, referencing individual bills for each consignment.

- Driver notification: E-way bill number, QR code, and printable PDF are pushed to the driver's mobile app before vehicle departure. The driver can show the digital copy at any checkpost.

- Validity monitoring and extension: The system tracks e-way bill validity periods and alerts dispatchers if a bill is about to expire during transit. Extension can be triggered directly from the app.

- Part-B updates on vehicle change: If a vehicle is swapped mid-route, the system detects the change via GPS tracking and auto-generates the Part-B update through the NIC API.

The entire process happens in the background with zero manual intervention. For a distributor dispatching 50 vehicles daily, this saves 3-4 hours of staff time and eliminates compliance risk completely.

Integration with E-Invoicing

For businesses above the e-invoicing threshold (currently Rs 5 crore annual turnover), the IRN (Invoice Reference Number) generated during e-invoicing can auto-populate Part A of the e-way bill. This means Part A data flows directly from the IRP (Invoice Registration Portal) to the e-way bill system without re-entry. The distributor only needs to add Part B (vehicle and transport details) to complete the e-way bill. A DMS that integrates both e-invoicing and e-way bill generation ensures seamless compliance from a single workflow, eliminating redundant data entry and ensuring consistency between invoices and e-way bills. Read more in our distributor billing software guide.

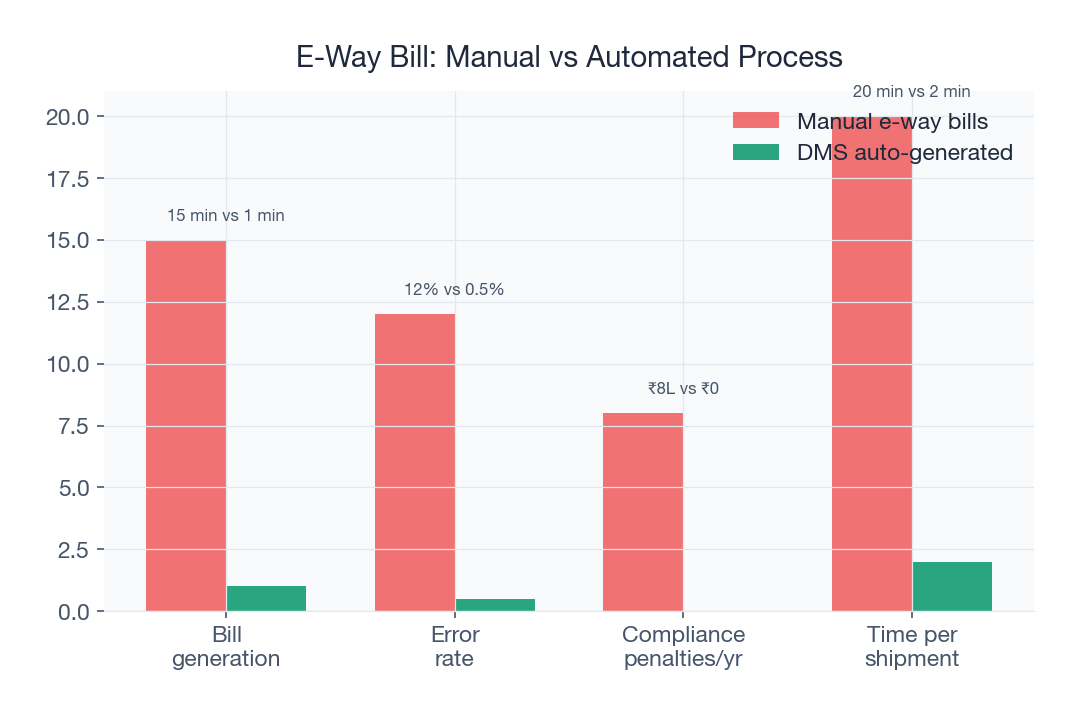

Case Study: Pune Dairy Distributor Eliminates Compliance Risk

A dairy distributor in Pune handling multiple dairy brands across 35-40 daily dispatches was spending 3 hours daily on manual e-way bill generation. Two staff members were dedicated to the task, logging into the NIC portal, entering consignment details from paper invoices, calculating exempt vs taxable values, and generating bills one by one. Despite this effort, 2-3 vehicle detentions per month were common due to errors, expired bills, or missed consignments. After implementing SpireStock's automated e-way bill module integrated with the billing system:

- E-way bill generation time: 3 hours daily reduced to 4 minutes (automated as part of invoicing)

- Vehicle detentions: 2-3 per month reduced to zero over 8 months

- Compliance rate: 100% achieved, as the system prevents dispatch without e-way bill when required

- Staff reallocation: Both staff members previously handling e-way bills now focus on customer service and order management

- Annual savings: Rs 4.5 lakh in staff time, penalty avoidance, and spoilage prevention

- Audit readiness: Complete e-way bill history searchable and exportable for any date range, vehicle, or consignment

Common E-Way Bill Mistakes Dairy Distributors Make

- Not excluding exempt goods from threshold: Generating unnecessary e-way bills for consignments where the taxable portion is below Rs 50,000. Wastes time but does not create legal issues.

- Failing to generate when required: The opposite error, assuming the entire load is exempt when it contains taxable products above threshold. Creates serious penalty risk.

- Not updating vehicle number (Part B): When a delivery vehicle breaks down or is swapped mid-route, the e-way bill must be updated. Manual processes miss this almost every time.

- Expired e-way bills: Forgetting to extend validity when delivery is delayed due to monsoon flooding, vehicle breakdown, or traffic congestion. Particularly common during July-September in cities like Mumbai and Kolkata.

- Wrong HSN codes: Using incorrect HSN codes leads to misclassification of products and potential penalties during GST audit. The difference between HSN 0401 (milk, 0/5% GST) and HSN 0402 (concentrated milk, 5/12% GST) matters.

- Not using consolidated bills: Creating individual e-way bills for each retailer drop instead of one consolidated bill per vehicle. Generates unnecessary paperwork and confusion.

E-Way Bill Compliance Checklist for Daily Operations

Use this checklist to ensure your daily dispatch operations are fully compliant:

- All invoices generated and classified by GST rate before vehicle loading

- Taxable consignment value calculated per vehicle (excluding exempt goods)

- E-way bills generated for all consignments above Rs 50,000 taxable value

- Consolidated e-way bill generated for multi-consignment vehicles

- Part B (vehicle number) updated and matching actual delivery vehicle

- E-way bill number and QR code available with the driver (digital or print)

- Validity period sufficient for expected transit time plus buffer

- Return trip documentation prepared if goods are being brought back

Spending hours on e-way bills daily? SpireStock automates e-way bill generation as part of the invoicing workflow, handling exemptions, mixed loads, consolidated bills, and Part-B updates automatically via NIC API integration. Distributors across dairy, FMCG, and beverage distribution have eliminated manual e-way bill work entirely. Start your free trial or view pricing to see how automation can transform your compliance operations.

Sources & References

- NIC, National Informatics Centre, E-Way Bill Portal

- CBIC, Central Board of Indirect Taxes and Customs

- GST Council, GST Council Official Portal

Frequently Asked Questions

No. Fresh milk (HSN 0401) is GST-exempt (0% rate) and therefore exempt from e-way bill requirements regardless of consignment value. Similarly, unbranded curd, lassi, buttermilk, and paneer are exempt. However, branded/packaged dairy products like UHT milk, flavoured milk, cheese, butter, and ice cream are taxable and require e-way bills if the consignment value exceeds Rs 50,000.

For mixed loads, calculate the e-way bill threshold based on the taxable portion only. If your vehicle carries Rs 80,000 of fresh milk (exempt) and Rs 60,000 of butter and cheese (taxable), you need an e-way bill because the taxable portion exceeds Rs 50,000. The e-way bill should list all goods on the vehicle including exempt items.

Yes, there are four bulk generation methods: JSON file upload on the NIC portal, direct API integration from your DMS, GSP (GST Suvidha Provider) services, and consolidated e-way bills for multiple consignments on one vehicle. API integration through your DMS is the most efficient for daily operations.

The minimum penalty is Rs 10,000 or the applicable tax amount, whichever is higher. The vehicle and goods are detained until the penalty is paid. For dairy distributors, this is catastrophic because perishable products can spoil during detention. A single violation can cost Rs 1-2 lakh when you factor in spoilage of the entire consignment.

Not necessarily. If one vehicle is making multiple deliveries, you can use a consolidated e-way bill that covers all consignments on that vehicle. This is more practical for dairy distributors making 40-80 drops per day. The consolidated e-way bill references individual e-way bills for each consignment.

For businesses above the e-invoicing threshold, the IRN generated during e-invoicing auto-populates Part A of the e-way bill. You only need to add Part B (transport details). This integration eliminates duplicate data entry and ensures consistency between your invoice and e-way bill. A DMS that handles both creates a seamless compliance workflow.

Related SpireStock Features

Related Industries

End-to-end dairy distribution software for milk, curd, paneer, and ghee brands. Manage orders, crates, cold chain, and GST billing in one platform.

Streamline FMCG distribution with order management, beat planning, retailer tracking, and GST billing. Built for Indian FMCG supply chains.

Manage beverage distribution with cold chain tracking, crate management, route optimization, and real-time delivery monitoring. Try SpireStock free.

Related Solutions

GPS fleet tracking, driver management, and route optimization for dairy and FMCG delivery vehicles. Reduce fuel costs by 25%. Try SpireStock.

Manage your entire distributor network digitally. Onboarding, credit limits, outstanding tracking, and performance analytics. Start free trial.

Related Entities

Ready to Streamline Your Distribution?

Start your free 30-day trial and see how SpireStock can transform your dairy, FMCG or consumer-goods distribution operation, from order capture to crate recovery.

SpireStock Team

Distribution Technology Experts

SpireStock Team writes for SpireStock on distribution management, supply-chain optimisation and field operations for Indian dairy and FMCG brands.