E-Invoicing in India: Where FMCG Distribution Stands in 2024

India's e-invoicing mandate has expanded steadily since its introduction in October 2020. As of August 2023, every business with aggregate annual turnover exceeding Rs 5 crore must generate e-invoices for all B2B supplies through the Invoice Registration Portal (IRP) operated by the National Informatics Centre (NIC). This threshold, lowered from Rs 10 crore in August 2023 via CBIC Notification No. 10/2023-Central Tax, brings the vast majority of FMCG distributors under the compliance net.

For FMCG distributors, e-invoicing is not a one-time IT project, it's a continuous operational requirement woven into every sale. A distributor generating 200-500 invoices daily cannot afford manual IRP submissions. This is where distribution management software becomes essential. This guide covers every aspect of e-invoicing compliance for Indian FMCG distribution, from technical requirements to penalty implications, and explains how modern distribution software automates the entire process.

Understanding the E-Invoicing Framework

What Is an E-Invoice?

An e-invoice is not a PDF or email. It is a structured JSON document in the prescribed schema that is submitted to the IRP, validated, and returned with a unique Invoice Registration Number (IRN) and a digitally signed QR code. The IRP also pushes invoice data to the GST portal (for return filing) and the e-way bill portal (for logistics), eliminating manual data entry across multiple compliance systems. The GSTN documentation specifies that every e-invoice must include the supplier GSTIN, buyer GSTIN, invoice number, date, HSN codes, taxable values, and tax amounts in the exact schema format.

The IRN (Invoice Registration Number)

The IRN is a 64-character hash generated by the IRP based on the supplier GSTIN, financial year, document type, and document number. It uniquely identifies every invoice in India's tax ecosystem. Once an IRN is generated, the invoice cannot be modified, only cancelled (within 24 hours) or corrected via a credit/debit note. This immutability is what makes e-invoicing a powerful anti-fraud mechanism.

QR Code Requirements

Every e-invoice must carry a QR code containing the supplier GSTIN, buyer GSTIN, invoice number, date, invoice value, number of line items, HSN code of the main item, and a unique IRN. For B2C invoices above Rs 1 lakh (as proposed in various GST Council discussions, though not yet mandated universally), a dynamic QR code is also recommended. Your distribution software must print this QR code on every invoice, both digital and physical copies.

E-Invoicing Thresholds and Applicability

| Effective Date | Turnover Threshold | CBIC Notification |

|---|---|---|

| 1 October 2020 | Rs 500 crore and above | 61/2020-Central Tax |

| 1 January 2021 | Rs 100 crore and above | 88/2020-Central Tax |

| 1 April 2021 | Rs 50 crore and above | 5/2021-Central Tax |

| 1 April 2022 | Rs 20 crore and above | 1/2022-Central Tax |

| 1 October 2022 | Rs 10 crore and above | 17/2022-Central Tax |

| 1 August 2023 | Rs 5 crore and above | 10/2023-Central Tax |

The trend is clear: the threshold is moving downward. Industry analysts expect it to eventually reach Rs 1 crore or even become universal, as recommended by the 50th GST Council meeting. FMCG distributors with turnover between Rs 5-20 crore, who are newly under the mandate, often lack the IT infrastructure to comply smoothly, making this the segment where distribution software adds the most value.

B2B vs B2C E-Invoicing Rules

The current mandate applies primarily to B2B (business-to-business) supplies, including supplies to registered dealers, inter-state supplies, and exports. B2C (business-to-consumer) invoices are not yet mandated for e-invoicing through the IRP, though a dynamic QR code on B2C invoices has been discussed in GST Council proceedings.

For FMCG distributors, this means:

- Distributor to retailer (registered): E-invoice mandatory if retailer has GSTIN

- Distributor to retailer (unregistered): E-invoice not mandatory, but dynamic QR code may be required on invoices above Rs 1 lakh

- Distributor to institutional buyer: E-invoice mandatory

- Credit notes and debit notes: Must also be reported through IRP

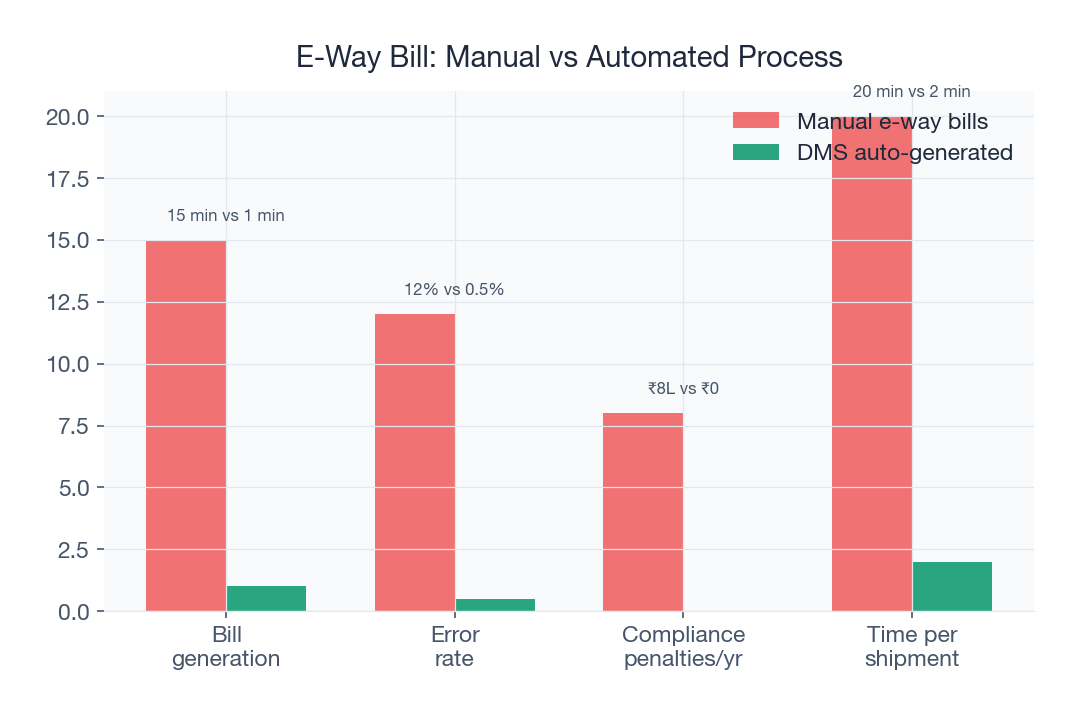

E-Way Bill Integration

One of the most powerful benefits of e-invoicing is automatic e-way bill generation. When an e-invoice is generated through the IRP with valid transport details (vehicle number, transporter ID, distance), the system automatically generates an e-way bill and returns the EWB number along with the IRN. This eliminates the need to separately log into the e-way bill portal for every consignment, a massive time saver for distributors dispatching 100+ vehicles daily.

E-way bills are mandatory for consignment values exceeding Rs 50,000 under GST Rule 138. For FMCG distribution, where a single vehicle often carries goods worth Rs 2-10 lakh, this applies to virtually every dispatch. Learn more about managing high-volume dispatch in our route optimization feature guide.

Penalties for Non-Compliance

The consequences of e-invoicing non-compliance are severe and cumulative:

- Section 122(1)(ii) of CGST Act: Penalty of Rs 25,000 for each instance of issuing an invoice without proper e-invoice registration (per invoice, not per month)

- ITC denial for buyer: If the supplier fails to generate a valid e-invoice, the buyer cannot claim Input Tax Credit (ITC) on that purchase. This creates downstream pressure, your retailers will refuse to buy from you if their ITC is at risk.

- E-way bill rejection: Without a valid IRN, auto-generated e-way bills are invalid. Goods in transit without valid e-way bills attract penalty of Rs 10,000 or tax sought to be evaded, whichever is higher, under Section 129.

- Assessment and audit exposure: Consistent e-invoicing failures draw attention from GST audit teams, potentially triggering detailed scrutiny of all tax filings

For a distributor generating 300 invoices daily, even a 5% error rate means 15 non-compliant invoices per day, translating to potential penalties of Rs 3.75 lakh daily (15 × Rs 25,000). Over a month, that's Rs 1.12 crore in theoretical penalty exposure. While enforcement has been selective so far, the risk is real and growing as the GST machinery becomes more automated.

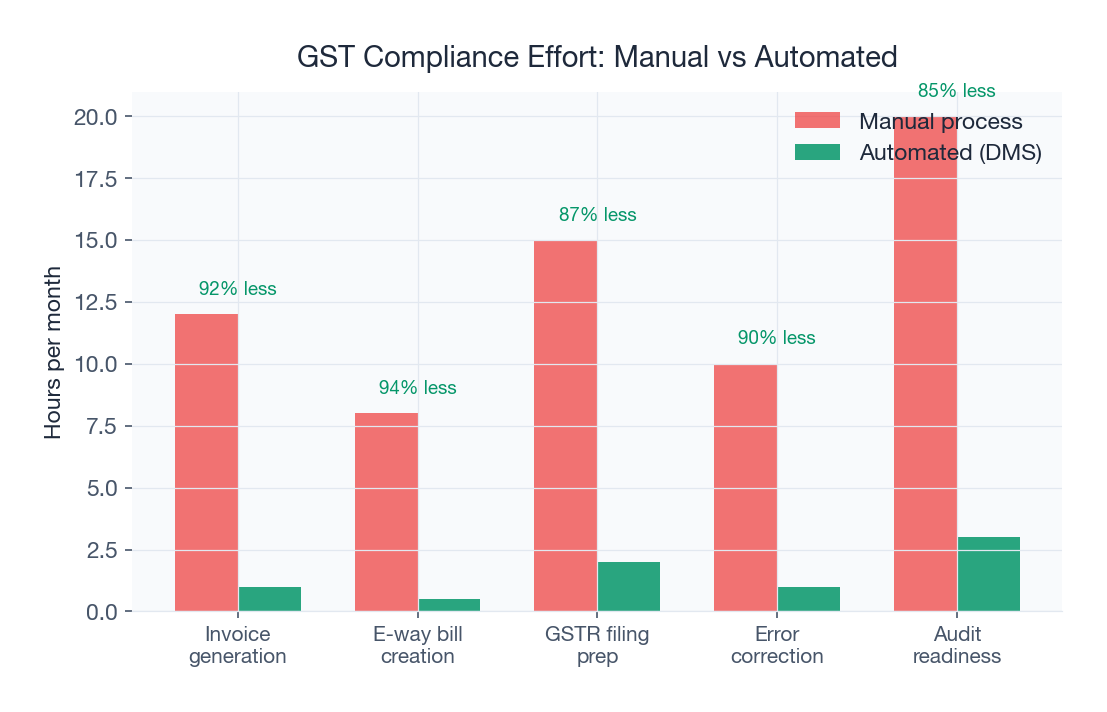

How DMS Software Handles E-Invoicing

Modern distribution management software automates the entire e-invoicing lifecycle within the normal order-to-dispatch workflow. Here's how it works in practice:

- Invoice generation: When an order is confirmed and dispatched, the DMS generates an invoice in the e-invoice JSON schema automatically, no manual data entry

- IRP submission: The invoice JSON is submitted to the IRP via API in real-time. The system handles authentication, rate limiting, and retry logic

- IRN and QR retrieval: The IRP returns the signed IRN and QR code, which the DMS embeds into the invoice document

- E-way bill generation: If transport details are available, the e-way bill is generated simultaneously

- Invoice printing: The complete invoice, with IRN, QR code, and e-way bill number, is printed or shared digitally with the retailer

- GSTR-1 auto-population: E-invoice data flows to the GST portal, pre-populating GSTR-1 returns and reducing filing effort

- Error handling: If the IRP rejects an invoice (schema validation failure, duplicate IRN, etc.), the DMS flags it immediately for correction before dispatch

SpireStock's invoice and billing module handles this entire workflow automatically. Our system processes e-invoices within 2-3 seconds per submission, handles bulk submissions of up to 500 invoices in a single API batch, and maintains a 99.7% first-submission success rate across our customer base. For GST details specific to dairy products, refer to our GST billing guide for dairy distribution.

Common E-Invoicing Errors and How to Avoid Them

| Error Type | Typical Cause | DMS Prevention |

|---|---|---|

| Invalid GSTIN | Retailer GSTIN expired/cancelled | Auto-validation against GST portal at order entry |

| HSN code mismatch | Wrong HSN mapped to product | Product master with validated HSN codes, locked against unauthorized edits |

| Duplicate IRN | Same invoice number resubmitted | Unique invoice numbering with series management |

| Schema validation failure | Missing mandatory fields | Pre-submission validation against IRP schema |

| Stale GSTIN data | Retailer changed registration type | Periodic GSTIN re-validation (monthly recommended) |

| Rate mismatch | Incorrect GST rate applied | HSN-linked tax rate master prevents manual rate entry |

Implementation Checklist for E-Invoicing Compliance

- Verify your aggregate turnover against the Rs 5 crore threshold

- Register on the IRP portal (einvoice1.gst.gov.in) using your GSTIN

- Ensure your DMS/billing software supports IRP API integration

- Validate your entire product master, HSN codes, GST rates, descriptions

- Validate your retailer master, GSTINs, registration types, state codes

- Run a parallel test: generate e-invoices alongside manual invoices for 1 week

- Set up error monitoring and alerts for IRP submission failures

- Train billing staff on the new workflow (typically 2-4 hours)

- Configure e-way bill auto-generation with vehicle and transporter master data

- Set up monthly GSTR-1 reconciliation between DMS and GST portal

Conclusion

E-invoicing compliance is no longer optional for any FMCG distributor with turnover above Rs 5 crore, and the threshold will only continue to drop. Manual compliance is unsustainable at distribution scale. The right distribution management software turns e-invoicing from a compliance burden into an automated background process, reducing errors, eliminating penalties, and actually improving your operational efficiency through auto-populated GST returns and integrated e-way bills. If you're still generating invoices manually or using software that lacks IRP integration, the compliance risk grows with every invoice. Schedule a compliance review with our team to assess your readiness.

Sources & References

- GST Council, Goods and Services Tax Council

- IBEF, India Brand Equity Foundation, FMCG Sector

- FSSAI, Food Safety and Standards Authority of India

Frequently Asked Questions

Yes, e-invoicing is mandatory for all businesses (including FMCG distributors) with aggregate annual turnover exceeding Rs 5 crore, effective from 1 August 2023 (CBIC Notification 10/2023). This covers the vast majority of organized FMCG distributors. The threshold is expected to decrease further.

Under Section 122(1)(ii) of the CGST Act, the penalty is Rs 25,000 per non-compliant invoice. Additionally, the buyer loses Input Tax Credit (ITC) on purchases without valid e-invoices, and goods shipped without valid e-way bills (which depend on e-invoices) attract penalties of Rs 10,000 or the tax amount, whichever is higher.

Modern DMS software generates the e-invoice JSON automatically from the sales invoice, submits it to the IRP via API, retrieves the IRN and QR code, embeds them in the invoice, auto-generates e-way bills, and pre-populates GSTR-1 returns, all without manual intervention. The entire process takes 2-3 seconds per invoice.

An Invoice Registration Number (IRN) is a unique 64-character hash generated by the Invoice Registration Portal (IRP) for every e-invoice. It is created from the supplier GSTIN, financial year, document type, and invoice number. Once generated, the invoice is immutable, it can only be cancelled within 24 hours or corrected via credit/debit notes.

Yes. When an e-invoice is submitted to the IRP with valid transport details (vehicle number, transporter ID, approximate distance), the system auto-generates an e-way bill and returns the EWB number alongside the IRN. This eliminates the need to separately access the e-way bill portal for each consignment.

Currently, e-invoicing through the IRP is mandatory only for B2B supplies. B2C invoices are not required to be submitted to the IRP, though dynamic QR codes on B2C invoices above Rs 1 lakh have been discussed in GST Council proceedings. Distributors selling to unregistered retailers are exempt from IRP e-invoicing but should prepare for future expansion of the mandate.

Related SpireStock Features

Related Industries

Related Solutions

Track distributor and retailer payments. Cash, UPI, cheque collection with reconciliation, ageing reports, and credit limit management.

Manage your entire distributor network digitally. Onboarding, credit limits, outstanding tracking, and performance analytics. Start free trial.

Related Entities

Ready to Streamline Your Distribution?

Start your free 30-day trial and see how SpireStock can transform your dairy, FMCG or consumer-goods distribution operation, from order capture to crate recovery.

SpireStock Team

Distribution Technology Experts

SpireStock Team writes for SpireStock on distribution management, supply-chain optimisation and field operations for Indian dairy and FMCG brands.