The Working Capital Challenge for FMCG Distributors

Every FMCG distributor in India lives a financial paradox: the business is profitable on paper but perpetually short of cash. Walk into any distributor's office in Ahmedabad, Pune, or Lucknow, and you will find an owner who can show you margins of 4-8% on his product portfolio but cannot tell you why his bank account balance never seems to reflect those margins. The answer is working capital -- the money trapped between the moment a distributor pays for stock and the moment he collects from retailers.

For a typical FMCG distributor handling Rs 50-80 lakh in monthly sales, Rs 8-15 lakh is locked in receivables at any given time. This is not an anomaly or a sign of poor management -- it is the structural reality of the FMCG distribution model in India. The distributor buys stock from the brand or CFA on day zero, often paying within 7-15 days. He sells to retailers on credit terms of 7-21 days. Retailers, in turn, pay when they can, stretching collection cycles to 15-45 days in practice. The result is a permanent cash gap that must be funded from somewhere. This structural challenge is one of the reasons why the FMCG distribution industry in India remains capital-intensive despite relatively predictable demand.

The cost of this gap is not abstract. At even modest interest rates of 12-15%, financing Rs 10 lakh of working capital costs Rs 1.2-1.5 lakh per year. For a distributor earning 5% net margin on Rs 80 lakh monthly sales (Rs 4.8 lakh annual net profit after all expenses), that interest bill represents 25-30% of net earnings. Scale this up to a larger distributor doing Rs 2 crore monthly, and the interest cost on Rs 30-40 lakh of receivables can reach Rs 4-6 lakh annually -- enough to hire two additional salesmen or invest in a delivery vehicle.

The working capital challenge intensifies during peak seasons. Festival periods like Diwali, Navratri, and Ramadan can spike inventory requirements by 40-80% as brands push schemes and retailers stock up. Summer months drive 3-5x demand for beverages, ice cream, and cooling products. During these peaks, a distributor who normally needs Rs 12 lakh of working capital may suddenly need Rs 20-25 lakh -- and the financing must be available within days, not weeks. For a comprehensive understanding of how distribution businesses work in India, see our guide on how to start an FMCG distribution business.

Interest is the silent margin killer. Consider this breakdown for a distributor with Rs 60 lakh monthly sales:

| Revenue Component | Annual Amount (Rs) | % of Revenue |

|---|---|---|

| Gross revenue | 7,20,00,000 | 100% |

| Gross margin (trade + scheme) | 57,60,000 | 8.0% |

| Operating expenses (staff, rent, transport) | 30,00,000 | 4.2% |

| Interest on working capital (Rs 12L at 14%) | 1,68,000 | 0.23% |

| Interest on vehicle/infra loans | 1,80,000 | 0.25% |

| Bad debt / write-offs | 2,16,000 | 0.30% |

| Net profit before tax | 21,96,000 | 3.05% |

That Rs 1.68 lakh in working capital interest may look small as a percentage of revenue, but it represents 7.6% of net profit. And this calculation assumes the distributor is borrowing at 14% -- many distributors, especially those relying on informal credit or personal loans, pay 18-24%. At those rates, interest can consume 2-6% of annual revenue, turning a decent distribution business into a break-even proposition.

Understanding Your Cash Conversion Cycle

Before exploring financing options, every distributor must understand their cash conversion cycle (CCC) -- the number of days between paying for inventory and collecting cash from sales. The CCC is the most important number in distribution finance, yet fewer than 10% of Indian FMCG distributors track it explicitly. Most operate on instinct, knowing they are always short of cash without understanding exactly why or how to fix it.

The cash conversion cycle has three components:

- Days Inventory Outstanding (DIO): How many days, on average, stock sits in your godown before it is sold. For a well-managed FMCG distributor, this should be 8-15 days. If your DIO is above 20, you are either over-ordering or carrying too many slow-moving SKUs.

- Days Sales Outstanding (DSO): How many days, on average, it takes to collect payment after a sale. For FMCG retail credit, this is typically 15-30 days, though it can stretch to 45+ days for larger institutional buyers or during downturns.

- Days Payable Outstanding (DPO): How many days you take to pay your supplier (brand or CFA). Most brands expect payment within 7-15 days, with some offering 21-30 day terms for high-volume distributors.

The formula is simple: CCC = DIO + DSO - DPO

For a typical distributor with DIO of 12 days, DSO of 25 days, and DPO of 10 days, the CCC is 12 + 25 - 10 = 27 days. This means the distributor needs to fund 27 days of working capital from other sources. On monthly sales of Rs 60 lakh, that translates to Rs 54 lakh (60 x 27/30) locked in the operating cycle at any point. Even after accounting for margins, this distributor needs approximately Rs 49-50 lakh of external working capital to sustain operations.

Why Most Distributors Are Financing Retailers

Here is the uncomfortable truth: when a distributor sells on credit to a retailer, the distributor is effectively acting as the retailer's bank. The retailer gets goods worth Rs 10,000 today and pays Rs 10,000 in 21 days. If the distributor is funding this credit at 14% annual interest, the cost of extending Rs 10,000 for 21 days is approximately Rs 81. On a typical margin of Rs 800-1,000 per Rs 10,000 of goods, the financing cost eats 8-10% of the margin on that transaction.

Multiply this across hundreds of retailers and thousands of invoices per month, and the aggregate financing cost becomes substantial. Yet most distributors do not think of it this way -- they see credit as a competitive necessity (which it is) without calculating its precise cost. The retailers, meanwhile, are getting interest-free financing from the distributor while often sitting on adequate cash in their shop drawers.

This is why tools like automated payment collection and credit limit enforcement are not just operational conveniences -- they are direct profit levers. Reducing your DSO from 25 days to 18 days on Rs 60 lakh monthly sales frees up Rs 14 lakh of working capital and saves Rs 1.6 lakh per year in interest at 14%. For more on reducing credit defaults and improving collections, see our detailed guide on reducing distributor credit defaults.

Calculating Your Real Cost of Capital

Many distributors underestimate their cost of capital because they only count the interest rate on their primary loan or overdraft. The real cost includes:

- Primary borrowing cost: Interest on bank OD, NBFC loan, or other formal credit facility.

- Processing fees: Upfront fees of 1-3% charged by lenders at disbursement or renewal.

- Opportunity cost of collateral: If you have pledged property worth Rs 50 lakh for a Rs 15 lakh OD limit, the unrealized potential of that collateral has a cost.

- Informal borrowing cost: Many distributors top up with personal loans, credit card cash advances (24-36% annualized), or borrowing from friends and family.

- Early payment discounts lost: Some brands offer 1-2% cash discount for immediate payment. If you are borrowing at 14% to pay in 15 days instead of taking the 2% discount for paying in 3 days, calculate whether the discount exceeds the interest saved.

A distributor who borrows Rs 10 lakh at 14% from a bank OD, Rs 5 lakh at 18% from an NBFC, and Rs 3 lakh informally at 24% has a blended cost of capital of approximately 17%. This is the number to use when evaluating financing options and calculating the ROI of operational improvements.

Financing Option 1: Bank Overdraft (OD)

The bank overdraft facility is the oldest and most widely used working capital instrument for Indian distributors. An OD is a revolving credit line attached to your current account -- you can withdraw up to the sanctioned limit, repay, and redraw as needed. Interest is charged only on the amount actually used, not the full sanctioned limit, making it efficient for businesses with fluctuating cash needs.

How It Works

The bank sanctions an OD limit based on your business turnover, collateral value, and creditworthiness. A typical FMCG distributor with Rs 60-80 lakh monthly turnover and property collateral can expect an OD limit of Rs 15-30 lakh. The limit is reviewed annually, and the bank may increase or decrease it based on your account conduct and business performance.

You draw from the OD as needed -- paying suppliers, covering payroll, or funding seasonal inventory buildup. As collections come in from retailers, you deposit into the same account, reducing the outstanding balance and the interest charge. The flexibility is the OD's greatest advantage: you pay interest only for the days and amounts you actually use.

Eligibility and Requirements

- Business vintage: Minimum 2-3 years of operation with audited financials.

- Turnover: Most banks require minimum Rs 40-50 lakh annual turnover for an OD facility.

- Collateral: Property mortgage is the standard collateral requirement. Banks typically lend 50-70% of the property's market value. Some banks accept fixed deposits, gold, or mutual funds as collateral.

- ITR and financials: Last 2-3 years of Income Tax Returns with profit. Balance sheets showing positive net worth.

- Bank statements: Last 12 months of current account statements showing regular business transactions and healthy average balances.

- CIBIL score: Minimum 700+ for most banks; 750+ for best rates.

Interest Rates and Costs

Bank OD interest rates for FMCG distributors in 2026 range from 10-14% per annum, depending on the bank, collateral quality, and borrower profile. Public sector banks (SBI, Bank of Baroda, PNB) typically offer 10-12%, while private banks (HDFC Bank, ICICI Bank, Axis Bank) charge 11-14%. Processing fees range from 0.5-1.5% of the sanctioned limit, payable at each annual renewal.

| Parameter | Public Sector Banks | Private Sector Banks |

|---|---|---|

| Interest rate range | 10-12% p.a. | 11-14% p.a. |

| Processing fee | 0.5-1.0% | 0.75-1.5% |

| Collateral required | Yes (property preferred) | Yes (property preferred) |

| Minimum turnover | Rs 40 lakh/year | Rs 50 lakh/year |

| Approval time | 15-30 days | 10-21 days |

| Annual renewal | Yes | Yes |

| Maximum limit | Up to Rs 2 crore | Up to Rs 5 crore |

Pros and Cons

Advantages: Lowest interest rate among all financing options. Pay interest only on utilized amount. Revolving facility with no fixed EMI burden. Builds banking relationship and credit history for future needs.

Disadvantages: Requires property collateral, which many young or renting distributors do not have. Slow approval process (15-30 days). Annual renewal involves re-documentation and potential limit reduction. Banks may demand personal guarantees from family members. Not suitable for first-time distributors without established financials.

The bank OD is best for established distributors with 3+ years of operations, audited financials, and property to offer as collateral. If you fit this profile, the OD should be your primary working capital source because of its cost advantage -- the 10-14% rate is 4-10 percentage points cheaper than alternatives.

Financing Option 2: NBFC Business Loans

Non-Banking Financial Companies (NBFCs) have emerged as a critical financing channel for FMCG distributors who cannot access bank credit or need faster, more flexible funding. NBFCs fill the gap between formal banking and informal credit, offering quicker disbursement, less stringent documentation, and more flexible eligibility criteria -- at the cost of higher interest rates.

How It Works

NBFC business loans for distributors are typically structured as term loans with fixed monthly EMIs over 12-36 months, or as revolving credit lines similar to bank ODs but with digital-first application processes. The application can be initiated online, documentation is lighter than banks, and disbursement can happen within 2-7 days for pre-approved profiles. Many NBFCs use GST return data and bank statement analysis algorithms to assess creditworthiness, reducing reliance on traditional financial statements.

Key NBFCs for FMCG Distributors

- Bajaj Finance: One of India's largest NBFCs, offering business loans from Rs 2 lakh to Rs 50 lakh for SMEs. Known for quick processing (as fast as 48 hours for existing customers). Interest rates 14-18%. Requires 2+ years of business vintage and minimum Rs 25 lakh annual turnover.

- IIFL Finance: Offers secured and unsecured business loans up to Rs 30 lakh. Accepts gold and property as collateral for lower rates. Interest rates 15-20%. Good option for distributors in tier-2 and tier-3 cities where IIFL has strong branch presence.

- Lendingkart: Digital-first NBFC specializing in small business loans. Loans from Rs 50,000 to Rs 2 crore. Approval in as little as 72 hours based on GST and bank statement analysis. Interest rates 16-24%. No collateral for loans below Rs 10 lakh. Particularly popular among smaller distributors and those in their first 2-3 years of operation.

- Tata Capital: Business loans up to Rs 75 lakh with interest rates of 14-19%. Strong in Maharashtra, Gujarat, and southern India. Offers both term loans and working capital loans with overdraft-style drawdown.

- Poonawalla Fincorp: Growing rapidly in the SME lending space. Business loans up to Rs 50 lakh with digital processing. Interest rates 14-20%. Competitive for distributors in western India.

Interest Rates and Terms

NBFC interest rates for FMCG distributor loans range from 14-20% per annum in 2026, with some NBFCs charging up to 24% for unsecured loans to newer businesses. The rate depends on four factors: (1) whether the loan is secured or unsecured, (2) the distributor's credit score and business vintage, (3) the loan amount and tenure, and (4) the NBFC's own cost of funds.

Processing fees are typically 2-3% of the loan amount -- higher than banks. Prepayment penalties of 2-5% apply for early closure in the first 6-12 months. Some NBFCs charge annual maintenance fees or documentation charges that add 0.5-1% to the effective cost.

Pros and Cons

Advantages: Faster approval and disbursement (2-7 days vs 15-30 days for banks). Less stringent documentation requirements. Available to newer businesses (1-2 year vintage). Unsecured options available for smaller amounts. Digital application process from mobile or laptop.

Disadvantages: Higher interest rates (14-20% vs 10-14% for banks). Processing fees of 2-3% increase effective cost. Fixed EMI structure reduces flexibility compared to OD. Prepayment penalties lock you in. Aggressive recovery practices at some NBFCs.

NBFC loans are best for growing distributors who need Rs 5-25 lakh quickly, cannot provide property collateral, or have business vintage below 3 years. Use them as a bridge while building the track record needed for a bank OD, or as supplementary funding during peak seasons when your bank OD limit is exhausted.

Financing Option 3: Invoice Discounting and Factoring

Invoice discounting is a financing method where a distributor sells his outstanding receivables (unpaid invoices) to a financier at a discount in exchange for immediate cash. Instead of waiting 21-45 days for retailers to pay, the distributor gets 80-90% of the invoice value within 24-48 hours. The financier collects the full amount from the retailer at maturity and earns the discount as his return.

How It Works

The process is straightforward. The distributor generates invoices for goods sold to retailers on credit, as tracked through his billing system. He uploads these invoices to an invoice discounting platform. The platform verifies the invoices (checking for duplicates, confirming the buyer's creditworthiness, and validating the invoice details). Once approved, the platform advances 80-90% of the invoice value to the distributor's bank account within 24-48 hours. When the retailer pays the invoice at maturity, the platform deducts its fee and releases the remaining 10-20% to the distributor.

Factoring is a related but distinct product. In factoring, the financier takes over the entire collections process -- the retailer pays the factor directly, not the distributor. Factoring typically involves longer-term relationships and higher volumes than one-off invoice discounting. For most FMCG distributors, invoice discounting on a platform is more accessible and practical than full factoring arrangements.

Key Platforms

- KredX: India's largest invoice discounting platform. Connects businesses with institutional investors willing to buy invoices. Supports invoices from Rs 1 lakh upward. Rates range from 12-16% annualized depending on the buyer's credit quality. Approval for new sellers takes 3-5 business days; subsequent transactions settle in 24-48 hours.

- Vayana Network: Supply chain finance platform backed by strong institutional partnerships. Specializes in trade finance for SMEs in manufacturing and distribution. Offers both invoice discounting and vendor financing. Competitive rates of 11-15% for invoices backed by strong corporate buyers.

- RXIL (Receivables Exchange of India): India's first TReDS (Trade Receivables Discounting System) platform, regulated by RBI. Allows MSMEs to discount invoices from corporate buyers through an auction process. Rates are typically 8-12% because banks and institutional investors bid competitively. However, RXIL primarily serves MSME suppliers to large corporates -- FMCG distributors can use it if their buyers are registered corporate entities.

- M1xchange: Another TReDS platform approved by RBI. Similar to RXIL in structure and rates. Growing network of corporate buyers and MSME sellers.

Costs and Considerations

Invoice discounting rates for FMCG distributors range from 12-18% annualized in 2026. The effective cost depends on the tenor (shorter tenors have higher annualized rates even if the absolute fee is lower), the buyer's creditworthiness (invoices from well-known retailers or chains get better rates), and the platform's fee structure (some charge a flat fee per transaction plus an annual subscription).

The major advantage of invoice discounting is that it requires no collateral -- the invoice itself is the security. This makes it accessible to distributors who lack property or other assets to pledge. However, there are limitations: the platform will only discount invoices from creditworthy buyers, the advance rate is 80-90% (not 100%), and the process requires proper invoicing with GST compliance and documented credit terms.

Pros and Cons

Advantages: No collateral required -- invoices are the security. Immediate cash against receivables within 24-48 hours. Does not appear as debt on the balance sheet (it is a sale of receivables). Available to distributors of any vintage if invoices are from creditworthy buyers. Scales with your business -- more sales means more invoices to discount.

Disadvantages: Higher effective cost (12-18% annualized) than bank OD. Only 80-90% advance against invoice value. Requires proper invoicing with documented credit terms. Platform onboarding takes 3-5 days. Not suitable for cash sales or sales without proper invoices. Retailer must be creditworthy in the platform's assessment.

Invoice discounting is best for distributors who sell to established retailers or chains on documented credit terms and need to accelerate cash flow without adding traditional debt. It is particularly useful during peak seasons when receivables swell but bank OD limits are already stretched. For distributors looking to improve their invoicing quality and documentation, SpireStock's invoice and billing features ensure every transaction is properly recorded and ready for discounting.

Financing Option 4: Supply Chain Finance

Supply chain finance (SCF) is a financing arrangement where a brand (the anchor or buyer) facilitates cheaper credit for its distributors by leveraging the brand's own creditworthiness. In essence, the brand tells a bank or financier: "This distributor buys Rs 50 lakh of goods from me every month. I confirm these purchases. Please extend credit to the distributor at a lower rate because I am guaranteeing the underlying trade relationship."

How It Works

In a typical SCF arrangement, the brand partners with a bank or SCF platform. When the distributor places an order, the SCF provider pays the brand on behalf of the distributor. The distributor then repays the SCF provider over an agreed period (typically 30-90 days). The interest rate is lower than what the distributor could get independently because the brand's credit rating backstops the transaction.

The economics are compelling. A mid-sized FMCG distributor might borrow independently at 16-18% from an NBFC. But if the brand -- say, a Rs 5,000 crore FMCG company with a AAA credit rating -- anchors the SCF program, the distributor might access credit at 10-13%. The 3-8 percentage point saving can be transformational for a distributor operating on thin margins.

Key Platforms and Programs

- Credlix: A dedicated supply chain finance platform for FMCG and manufacturing. Works with brands to extend distributor financing at competitive rates. Distributor onboarding is driven by the brand, reducing documentation friction. Rates of 10-14% depending on the anchor brand's rating.

- Axis Bank SCF: One of the largest bank-led SCF programs in India. Partners with major FMCG companies to offer distributor financing. Offers both pre-shipment (before goods are dispatched to the distributor) and post-shipment (after the distributor receives goods) financing. Competitive rates of 9-12% for distributors of investment-grade brands.

- HDFC Bank Supply Chain Finance: Comprehensive SCF suite including dealer financing, vendor financing, and channel financing. Strong presence with large FMCG brands. Rates of 10-13%. Digital platform with real-time disbursement against confirmed purchase orders.

- Kotak Mahindra Bank SCF: Growing SCF program with a focus on mid-market FMCG brands. Offers flexible tenors of 30-120 days. Rates of 10-14%. Good option for distributors of brands that do not have SCF programs with larger banks.

Eligibility and Access

The critical difference with supply chain finance is that access is driven by the brand, not the distributor. The distributor cannot independently approach an SCF platform and say "finance my purchases." The brand must first establish an SCF program with a bank or platform, and then nominate its distributors for onboarding. This means SCF availability depends on whether your brand partner has set up such a program.

As of 2026, most large FMCG companies in India (Hindustan Unilever, ITC, Nestle, P&G, Britannia) have SCF programs with at least one bank. However, coverage is uneven -- a brand may have SCF available for its top 200 distributors but not for the remaining 3,000. Mid-sized and regional FMCG brands are increasingly adopting SCF through fintech platforms like Credlix and Vayana, but many still do not offer SCF to their distribution channels.

Pros and Cons

Advantages: Lowest rates among non-bank options (9-14% because of brand backing). Minimal collateral requirements. Disbursement aligned with purchase orders, so financing matches actual business needs. Strengthens brand-distributor relationship. No separate loan application -- onboarding is driven by the brand.

Disadvantages: Not available unless your brand partner has an SCF program. Distributor has no control over program availability or terms. Financing is tied to specific brand purchases -- cannot be used for other brands or general expenses. Brand may use SCF access as a leverage tool (threatening to remove distributors from the program). Limited to the sanctioned limit per distributor, which may not cover full requirements.

Supply chain finance is the best option when available -- it combines bank-like rates with digital convenience. If your brand offers SCF, use it as your primary financing tool for that brand's purchases and supplement with bank OD or NBFC loans for other needs.

Financing Option 5: Stock Now Pay Later Fintech

A new category of fintech platforms has emerged specifically targeting the FMCG distribution chain with "stock now, pay later" (SNPL) models. These platforms essentially offer short-term credit (15-30 days) at the point of purchase, allowing distributors to order stock and defer payment. Think of it as a B2B version of consumer "buy now, pay later" apps -- adapted for the realities of FMCG distribution.

How It Works

The distributor signs up on the platform, completes KYC, and gets a credit limit (typically Rs 1-10 lakh based on business size and history). When ordering stock -- either through the brand's system or through the platform's marketplace -- the distributor selects the SNPL option. The platform pays the brand or stockist immediately, and the distributor gets a repayment window of 15-30 days. If the distributor repays within the interest-free period (typically 7-15 days), there may be zero or minimal charges. Beyond that, interest accrues at rates that can be 18-30% annualized.

Key Platforms

- Rupifi: B2B BNPL platform focused on SME distributors and retailers. Integrates with B2B commerce platforms and brand ordering systems. Credit limits from Rs 50,000 to Rs 25 lakh. Offers 7-30 day payment terms. Interest-free period of 7-14 days for qualifying transactions. Has processed significant volume in FMCG and pharma distribution channels.

- OkCredit Business: Started as a digital ledger (khata) for small businesses and expanded into business credit. Leverages transaction history on the OkCredit ledger to assess creditworthiness. Offers small-ticket credit (Rs 25,000 to Rs 5 lakh) with quick approval. Particularly popular among smaller distributors and retailers in tier-2 and tier-3 cities.

- Zetwerk Capital / Arzooo Credit: B2B commerce platforms that have embedded credit into their ordering workflows. Distributors ordering through these platforms can opt for deferred payment. Credit limits based on purchase history on the platform.

Interest Rates and Hidden Costs

SNPL platforms often market themselves as "interest-free" or "zero cost" for short tenors, but the economics tell a different story. A typical SNPL transaction looks like this:

- Order value: Rs 2,00,000

- Interest-free period: 7 days

- If paid in 7 days: Zero interest (but the platform may charge 0.5-1% processing fee)

- If paid in 15 days: 1.5% fee (equivalent to 36% annualized)

- If paid in 30 days: 2.5% fee (equivalent to 30% annualized)

- Late payment penalty: 2-4% per month additional

The annualized rates are significantly higher than bank ODs or even NBFC loans. However, the SNPL model is not designed to be a year-round financing solution -- it is a short-term bridge for specific purchases, particularly useful during supply constraints or scheme-driven bulk orders where the profit from the deal exceeds the financing cost.

Pros and Cons

Advantages: Extremely easy onboarding (10-15 minutes on mobile). No collateral or documentation beyond KYC and bank statements. Instant credit decisions using AI-based underwriting. Flexible -- use it transaction by transaction, no long-term commitment. Interest-free window for quick repayment. Good for first-time distributors building credit history.

Disadvantages: High effective interest rates (18-36% annualized) if payment extends beyond interest-free period. Small credit limits (Rs 1-10 lakh) insufficient for larger distributors. Late payment penalties are severe. Platform may share default data with credit bureaus, impacting future borrowing. Limited to purchases through partner platforms. Not a substitute for structured working capital financing.

SNPL fintech is best for smaller distributors (monthly turnover below Rs 20 lakh) who need quick, small-ticket financing for specific deals and can repay within the interest-free window. It is also useful as a supplementary tool for established distributors during peak seasons when other credit lines are maxed out. Do not use it as your primary financing source -- the effective rates make it the most expensive option on this list.

Comparison Table: All Financing Options

The following table provides a side-by-side comparison of all five financing options available to FMCG distributors in India as of 2026. Use this to identify which options match your business profile and financing needs.

| Parameter | Bank OD | NBFC Loan | Invoice Discounting | Supply Chain Finance | SNPL Fintech |

|---|---|---|---|---|---|

| Interest rate (annualized) | 10-14% | 14-20% | 12-18% | 9-14% | 18-36% |

| Collateral required | Yes (property) | Optional (varies) | No (invoices as security) | Minimal (brand backing) | No |

| Approval time | 15-30 days | 2-7 days | 3-5 days (first time); 24-48 hrs (repeat) | 7-14 days (first time); instant (repeat) | 10-15 minutes |

| Maximum amount | Rs 15L - 5 crore | Rs 2L - 75 lakh | Based on receivables | Based on brand purchases | Rs 1-25 lakh |

| Business vintage needed | 2-3 years | 1-2 years | Any (if invoices are valid) | Any (brand-driven) | 6 months+ |

| Best for | Established distributors with property | Growing distributors needing speed | Distributors with strong retail buyers | Distributors of large FMCG brands | Small distributors, specific deals |

| Repayment flexibility | High (revolving, pay interest on usage) | Low (fixed EMI) | Moderate (aligned with invoice maturity) | Moderate (30-90 day window) | Low (fixed window, penalties for delay) |

| Impact on balance sheet | Shows as borrowing | Shows as borrowing | Off-balance-sheet | Shows as borrowing | Shows as borrowing |

| Documentation burden | Heavy | Moderate | Light (invoices + KYC) | Light (brand-driven) | Minimal (KYC only) |

Which Option Is Right for You?

The right financing mix depends on your business stage and profile:

- New distributor (0-2 years): Start with SNPL fintech for initial transactions, move to NBFC loans as you build track record. Use invoice discounting if you serve creditworthy retail chains. Target: establish bank OD eligibility within 2-3 years.

- Growing distributor (2-5 years, Rs 30-80 lakh monthly): Bank OD as primary source. NBFC loan as supplementary for peak seasons. Explore invoice discounting for large retail accounts. Ask your brand about SCF programs.

- Established distributor (5+ years, Rs 1 crore+ monthly): Bank OD at negotiated rates as primary source. SCF for brand purchases where available. Invoice discounting for largest retail accounts. Use the sales analytics from your DMS to negotiate better terms with lenders.

How DMS Data Improves Your Borrowing Power

One of the most underappreciated advantages of using a Distribution Management System is the data it generates -- and how that data can dramatically improve your access to and cost of financing. Lenders are information businesses at their core. They charge higher rates and demand more collateral when they have less information about the borrower. A distributor who walks into a bank with handwritten ledgers and approximate numbers will always get worse terms than one who presents clean, digital, real-time business data.

Real-Time Sales Data as Underwriting Input

Modern lenders -- particularly NBFCs and fintech platforms -- are increasingly accepting DMS data as part of their underwriting process. When a distributor can provide:

- Daily sales volume and value: Proves consistent business activity and revenue trends. Lenders can see if sales are growing, stable, or declining -- far more useful than a 12-month-old ITR.

- Customer-wise sales distribution: Shows concentration risk. A distributor selling to 200 retailers is lower risk than one dependent on 5 large buyers.

- Product-wise margins: Demonstrates understanding of portfolio economics and ability to maintain profitability.

- Seasonal patterns: Helps lenders anticipate cash flow cycles and structure appropriate repayment schedules.

SpireStock's sales analytics dashboard generates exactly these reports in formats that lenders can interpret. Several of our distributor clients have reported that sharing SpireStock data with their bank managers resulted in faster approvals and, in some cases, higher OD limits.

Inventory Visibility for Secured Lending

Inventory is an asset, but most lenders discount it heavily because they cannot verify its existence, condition, or saleability. A bank considering a Rs 20 lakh loan against Rs 30 lakh of claimed inventory has no way to confirm the inventory is actually there, is not expired, and can be sold at its stated value -- unless the distributor provides verifiable inventory data.

A DMS with real-time inventory tracking changes this dynamic. When the system shows current stock of Rs 28 lakh with batch-level detail, expiry dates, and aging analysis, the lender has confidence that the collateral is real and valuable. Some progressive lenders are beginning to accept DMS-generated inventory reports as part of stock audit requirements, reducing the cost and friction of physical inventory verification.

Receivables Aging as Credit Quality Proof

Perhaps the most powerful DMS data for financing purposes is the receivables aging report. This report shows exactly how much money is owed by each retailer, for how long, and whether payments are being collected within agreed terms. A clean receivables aging report -- where 80%+ of receivables are within 30 days and less than 5% are beyond 60 days -- tells a lender that the distributor has disciplined credit management and reliable cash flow.

Conversely, a receivables aging report showing 30% of receivables beyond 60 days signals collection problems and higher risk. Either way, having the data is better than not having it -- because without data, the lender assumes the worst and prices accordingly. With SpireStock's distribution tracking and credit management features, distributors can generate receivables aging reports at any time, demonstrating their collection efficiency to lenders.

Reducing Working Capital Needs Through Better Operations

The best financing is the financing you do not need. As we covered in our distribution management software guide, technology-driven operations directly reduce the cash gap. Before optimizing which lender to use, the smartest distributors focus on reducing the amount of working capital required in the first place. Every day shaved off the cash conversion cycle frees up real cash -- and the tools to achieve this are operational, not financial.

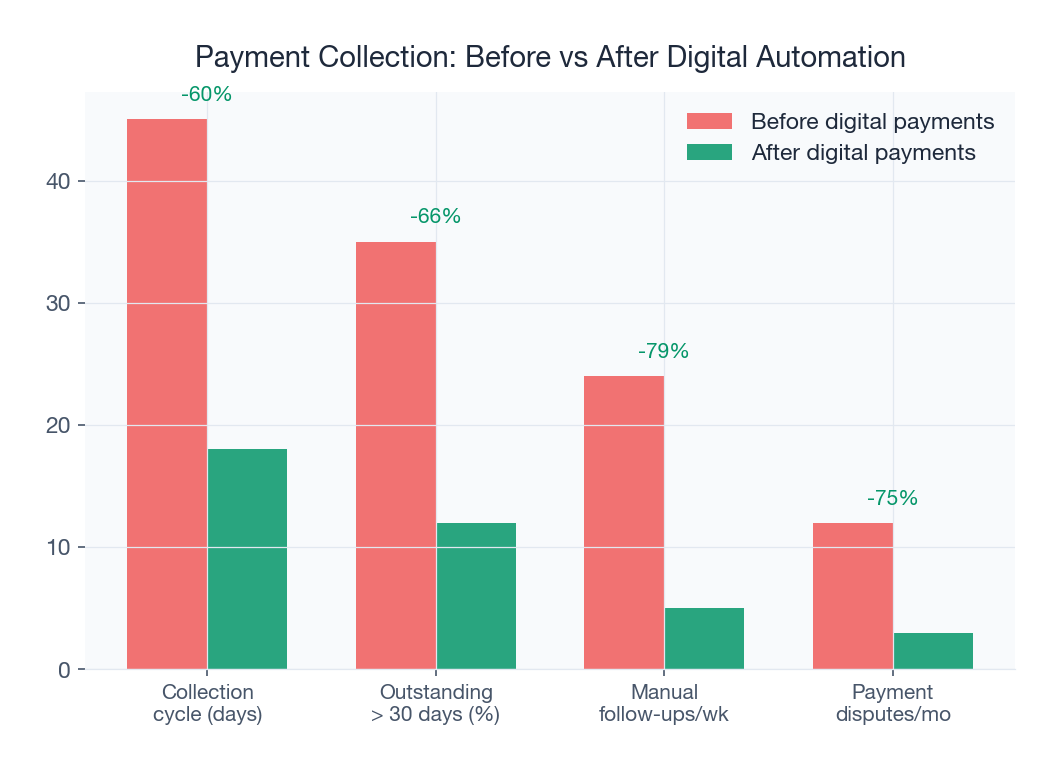

Faster Collections with Auto-Reminders

The single biggest lever for reducing working capital is collecting from retailers faster. A 5-day reduction in DSO on Rs 60 lakh monthly sales frees up Rs 10 lakh of working capital permanently. The challenge is that manual collection follow-up -- calling or visiting each retailer who is overdue -- is time-consuming and inconsistent. Salesmen avoid uncomfortable payment conversations, overdue amounts accumulate, and the distributor's cash stays locked.

Automated payment reminders through a DMS change this dynamic. When the system sends an SMS or WhatsApp message to a retailer 3 days before the payment due date, on the due date, and 3 days after, collection rates improve by 15-25% on average. The reminder is systematic (every retailer, every time), non-confrontational (a system message, not a personal call), and documented (creating an audit trail). SpireStock's payment collection module automates this entire workflow, including escalation to the salesman when reminders go unheeded.

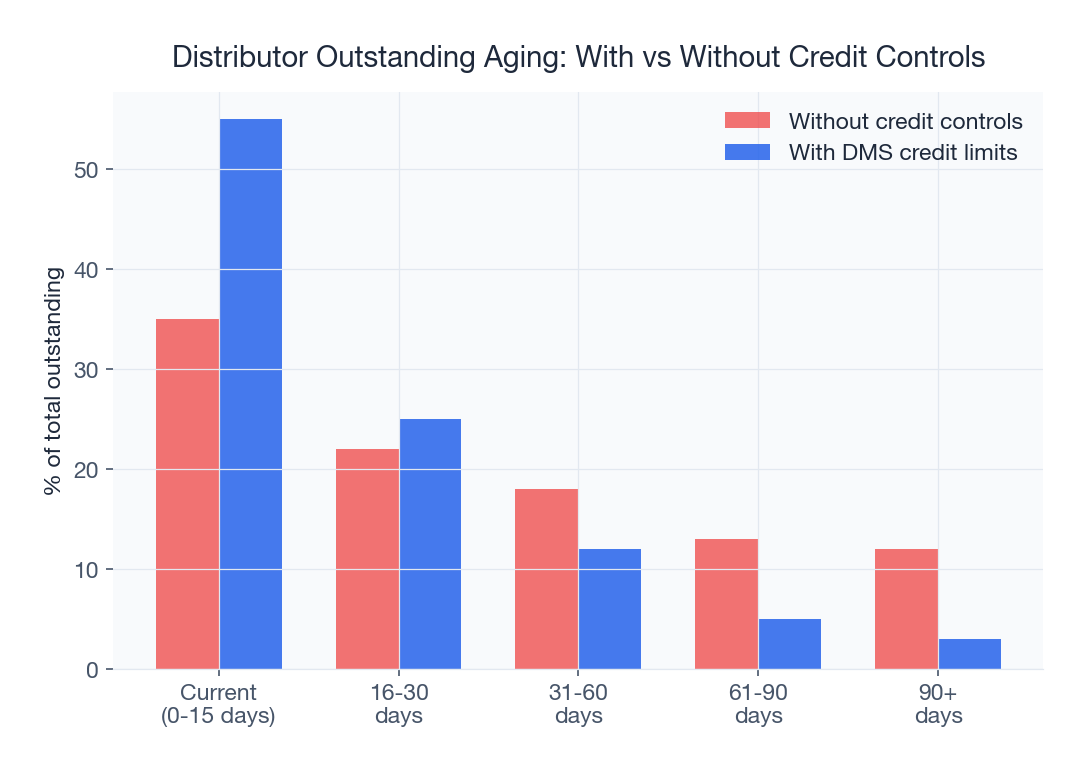

Credit Limit Enforcement

Many distributors set credit limits for retailers on paper but fail to enforce them in practice. A retailer with a Rs 50,000 credit limit might have Rs 80,000 outstanding because the salesman approved additional orders to meet his targets, or because the distributor wanted to push stock during a scheme period. This credit overextension is a direct working capital drain.

DMS-enforced credit limits prevent this. When the system blocks new orders for a retailer who has exceeded their credit limit or has overdue payments beyond a threshold, the distributor's exposure is automatically controlled. The system does not negotiate or make exceptions based on relationships -- it enforces the policy consistently. This is uncomfortable initially (some retailers push back), but distributors who implement strict credit limit enforcement typically see receivables reduce by 15-20% within 3 months.

Scheme Settlement Speed

FMCG distributors routinely advance scheme benefits (discounts, free goods, display allowances) to retailers on behalf of the brand, with the understanding that the brand will reimburse these amounts. In practice, scheme settlements from brands take 30-90 days -- sometimes longer. During peak scheme periods (festival seasons, new product launches), a distributor might have Rs 3-8 lakh locked in unsettled scheme claims. This is working capital that the distributor is financing at his borrowing cost while waiting for the brand to process reimbursements.

A DMS with proper scheme tracking accelerates settlement by providing brands with clean, auditable scheme utilization data. When the distributor can show exactly which retailers received which scheme benefits, with invoice-level documentation, the brand's finance team can process settlements faster. SpireStock's scheme management module tracks every scheme transaction and generates settlement reports that brands can verify and approve without lengthy reconciliation.

Inventory Optimization

Every rupee of excess inventory is a rupee of working capital locked unnecessarily. A distributor carrying 20 days of inventory when 12 days would suffice is holding Rs 16 lakh in excess stock (on Rs 60 lakh monthly sales) at a carrying cost of Rs 2.24 lakh per year (at 14% interest). The excess inventory also carries the risk of expiry, damage, and obsolescence.

DMS-driven inventory optimization uses sales velocity data to set optimal reorder points and quantities for each SKU. Instead of ordering based on gut feel or brand pressure, the distributor orders based on actual sell-through rates, adjusting for seasonal patterns and promotional activities. SpireStock's order management system generates recommended orders based on current stock levels, sales velocity, and lead times, helping distributors maintain optimal inventory without over-stocking.

The combined impact of these operational improvements can be transformative. A distributor who reduces DSO by 7 days, enforces credit limits (reducing receivables by 15%), cuts inventory days by 5, and accelerates scheme settlements by 20 days can free up Rs 15-25 lakh of working capital -- equivalent to eliminating the need for an NBFC loan entirely.

Case Studies: Distributors Who Optimized Their Financing

The following case studies illustrate how distributors at different stages have combined financing optimization with operational improvements to strengthen their working capital position.

Case Study 1: A Snacks Distributor in Indore Reduces Interest Cost by 40%

A snacks and beverages distributor in Indore with monthly sales of Rs 45 lakh was funding his entire working capital through an NBFC term loan at 18% interest. His annual interest cost was Rs 2.7 lakh on a Rs 15 lakh facility. The distributor had been operating for 4 years but had never approached a bank for an OD because he assumed the documentation would be too complex and the approval too slow.

After implementing SpireStock, the distributor had 8 months of clean digital sales data, inventory reports, and receivables aging reports. His SpireStock dashboard showed consistent monthly sales growth of 3-4%, healthy inventory turnover of 14 days, and a DSO of 22 days -- all indicators of a well-managed business. Armed with this data, he approached SBI for an OD facility.

The bank sanctioned a Rs 12 lakh OD at 11.5% against his residential property. The distributor retained Rs 5 lakh of the NBFC loan for peak season flexibility and used the bank OD as his primary facility. His blended interest cost dropped from 18% to approximately 13.4%, saving Rs 69,000 annually. Additionally, SpireStock's auto-reminder feature reduced his DSO from 22 to 17 days, freeing up Rs 7.5 lakh of working capital and further reducing borrowing needs. Net annual savings from both financing optimization and operational improvement: Rs 1.24 lakh -- a 5.5% increase in net profit.

Case Study 2: A Dairy Distributor in Jaipur Uses Invoice Discounting for Seasonal Peaks

A dairy products distributor in Jaipur handling Rs 1.2 crore monthly sales had a Rs 25 lakh bank OD at 12% that covered his regular working capital needs. However, during summer months (April-July), demand for dairy beverages, lassi, and ice cream surged by 60-80%, requiring an additional Rs 15-20 lakh of working capital for 4 months. The distributor had been managing this gap with a combination of personal savings and high-cost borrowing from a local money lender at 24% annualized.

After exploring options, the distributor onboarded onto KredX for invoice discounting. His invoices to 12 institutional buyers (hotel chains, catering companies, and modern trade outlets) were eligible for discounting at 14% annualized. During the summer peak, he discounted Rs 8-12 lakh of receivables per month, getting immediate cash to fund additional inventory purchases from his dairy brand principals.

The shift from informal borrowing at 24% to invoice discounting at 14% saved Rs 40,000 over the 4-month peak season. More importantly, the distributor no longer had to deplete personal savings or negotiate uncomfortable loans. The KredX facility scaled automatically with his sales volume -- higher summer sales generated more invoices to discount, providing self-adjusting financing exactly when needed.

Case Study 3: A Multi-Brand Distributor in Chennai Leverages Supply Chain Finance

A multi-brand FMCG distributor in Chennai handling 4 major brands with combined monthly sales of Rs 2.5 crore was maintaining Rs 40 lakh in working capital through a combination of bank OD (Rs 25 lakh at 12%), NBFC loan (Rs 10 lakh at 17%), and personal funds (Rs 5 lakh). His blended cost of capital was approximately 13.5%.

Two of his four brand principals -- a leading personal care company and a packaged foods major -- launched supply chain finance programs through HDFC Bank and Credlix respectively. The distributor was nominated for both programs and onboarded within 10 days. The SCF limits were Rs 12 lakh with the personal care brand (at 10.5%) and Rs 8 lakh with the packaged foods brand (at 11%), covering Rs 20 lakh of his working capital needs at an average rate of 10.7%.

With Rs 20 lakh covered by SCF at 10.7%, the distributor reduced his bank OD utilization to Rs 15 lakh and closed the NBFC loan entirely, saving Rs 1.7 lakh in annual interest. He also used SpireStock's credit management module to enforce stricter credit limits on his retail accounts, reducing receivables by 18% (Rs 7.2 lakh freed) over 4 months. The combined effect -- cheaper financing plus reduced financing needs -- improved his net profit by Rs 2.8 lakh annually. He reinvested the savings into a second delivery vehicle, expanding his retail coverage by 120 outlets. For more on how distributor management solutions can help optimize your operations, explore SpireStock's comprehensive toolkit.

Ready to strengthen your working capital position? SpireStock helps FMCG distributors reduce working capital needs through faster collections, credit limit enforcement, scheme settlement tracking, and inventory optimization -- while generating the digital data that improves your borrowing power with banks and NBFCs. Book a free demo or explore our pricing plans to see how much working capital you could free up in your first 90 days.

Sources & References

- RBI, Reserve Bank of India: Priority Sector Lending Guidelines for MSMEs

- SIDBI, Small Industries Development Bank of India: MSME Financing Report

- TReDS, Trade Receivables Discounting System: RBI Framework

- IBEF, FMCG Sector Overview: India Brand Equity Foundation

- NielsenIQ, India FMCG Distribution Channel Trends

Frequently Asked Questions

A typical FMCG distributor with Rs 50-80 lakh monthly sales needs Rs 8-15 lakh of working capital at any given time. The exact amount depends on your cash conversion cycle -- the gap between paying suppliers and collecting from retailers. Distributors with faster collections (DSO below 20 days) and efficient inventory management (DIO below 12 days) need less working capital than those with longer cycles.

Supply chain finance (SCF) backed by your brand principal offers the lowest rates at 9-14% annualized, because the brand's credit rating reduces lender risk. If SCF is not available from your brand, a bank overdraft (OD) at 10-14% is the next cheapest option, though it requires property collateral and 2-3 years of business vintage. The most expensive option is fintech SNPL (stock now pay later) at 18-36% annualized.

Yes. New distributors (under 2 years) can access unsecured financing through NBFC business loans (Rs 2-10 lakh at 16-24%), invoice discounting platforms (if selling to creditworthy buyers), and fintech SNPL platforms (Rs 1-10 lakh with 15-30 day repayment). These options cost more than secured bank loans but do not require property collateral. Building 6-12 months of clean DMS data can help you qualify for better terms.

Invoice discounting lets you sell your outstanding invoices (unpaid bills from retailers) to a financier at a small discount for immediate cash. Instead of waiting 21-45 days for retailer payment, you get 80-90% of the invoice value within 24-48 hours. Platforms like KredX, Vayana, and RXIL facilitate this. It requires no collateral (the invoice is the security) and is particularly useful during peak seasons when receivables swell.

A DMS like SpireStock helps with financing in two ways. First, it generates clean digital data -- sales reports, inventory levels, receivables aging -- that lenders increasingly accept as underwriting input, leading to faster approvals and better terms. Second, it reduces the amount of financing you need by automating collections (reducing DSO), enforcing credit limits (reducing receivables), optimizing inventory (reducing excess stock), and accelerating scheme settlements.

Supply chain finance is a brand-backed financing arrangement where a bank or fintech extends credit to distributors at lower rates because the FMCG brand guarantees the trade relationship. Rates are typically 9-14% compared to 14-20% for independent NBFC loans. Access is driven by the brand, not the distributor -- your brand must have an SCF program and nominate you for onboarding. Most large FMCG brands in India have SCF programs as of 2026, but coverage varies.

Four operational levers reduce working capital needs: (1) Faster collections through auto-reminders and systematic follow-up can cut DSO by 5-10 days. (2) Credit limit enforcement prevents receivable overextension and can reduce outstanding by 15-20%. (3) Inventory optimization using DMS data eliminates excess stock. (4) Faster scheme settlements with proper documentation accelerate brand reimbursements. Together, these can free up Rs 15-25 lakh for a mid-sized distributor.

Banks typically require: last 2-3 years of audited financials (profit and loss, balance sheet), last 2-3 years of Income Tax Returns showing profit, last 12 months of current account bank statements, property documents for collateral (sale deed, tax receipts, valuation report), GST registration and returns, business registration (partnership deed, company incorporation), and KYC documents. A CIBIL score of 700+ is required, with 750+ needed for the best rates.

Related SpireStock Features

GST-compliant invoicing with HSN codes, gate passes, and financial ledger.

Powerful dashboards with sales trends, MIS reports, and distribution analytics.

End-to-end order lifecycle from placement to delivery with multi-level approval workflows.

Real-time GPS tracking of vehicles and drivers with route optimization for faster deliveries.

Related Industries

Streamline FMCG distribution with order management, beat planning, retailer tracking, and GST billing. Built for Indian FMCG supply chains.

End-to-end dairy distribution software for milk, curd, paneer, and ghee brands. Manage orders, crates, cold chain, and GST billing in one platform.

Related Solutions

Track distributor and retailer payments. Cash, UPI, cheque collection with reconciliation, ageing reports, and credit limit management.

Manage your entire distributor network digitally. Onboarding, credit limits, outstanding tracking, and performance analytics. Start free trial.

Related Entities

Ready to Streamline Your Distribution?

Start your free 30-day trial and see how SpireStock can transform your dairy, FMCG or consumer-goods distribution operation, from order capture to crate recovery.

SpireStock Team

Product & Industry Insights

SpireStock Team leads product at SpireStock, where the team ships distribution management software for India's dairy, FMCG and consumer-goods brands.