The Credit Crisis in Indian FMCG Distribution

Credit is the invisible engine of Indian FMCG distribution. Walk into any distributor's office from Mumbai to Delhi, and you will find the same reality: lakhs of rupees extended to retailers on trust, tracked in tattered ledgers or WhatsApp messages, with no systematic way to assess, monitor, or collect. An estimated Rs 60,000 crore or more is locked in distributor-to-retailer credit at any given point, representing the single largest working capital drain in the Indian consumer goods supply chain.

For an individual distributor handling Rs 20 lakh in monthly sales, even 15 extra days of delayed credit recovery translates to Rs 10-12,000 per month in financing cost, assuming a modest 8% annual cost of capital. Scale that across a network of 200 distributors and the brand is looking at Rs 20-25 lakh per month in invisible costs that never appear in any P&L line item. The breakdown happens because the systems, processes, and discipline required for effective credit management simply do not exist in most Indian FMCG distribution networks.

The consequences ripple outward. When distributors cannot collect from retailers, they delay payments to brands. When brands tighten credit terms, distributors reduce market coverage or exit entirely. This guide covers the complete credit management lifecycle, from understanding why defaults happen to building credit scoring models, implementing automated controls, and optimizing collection. Whether you operate in dairy, beverages, bakery and confectionery, or packaged consumer goods, the strategies here will help you reduce defaults, accelerate collections, and unlock working capital trapped in your distribution channel.

Why Credit Defaults Happen in FMCG Distribution

Before solving credit defaults, you need to understand why they happen. The causes are structural, behavioural, and systemic, and most Indian FMCG companies are fighting all three simultaneously.

Poor Credit Assessment

Most distributors extend credit to retailers based on gut feeling, relationship tenure, or market pressure rather than any objective assessment of creditworthiness. A retailer who has been buying for five years gets Rs 2 lakh in credit simply because they have been around, not because their payment behaviour warrants it. There is no scoring model, no financial analysis, no risk-adjusted limit calculation. The result is that credit limits bear no relationship to the retailer's actual ability and willingness to pay.

No Automated Credit Stops

Even when credit limits exist on paper, they are rarely enforced in practice. The salesperson knows the retailer is over-limit but takes the order anyway because they need to hit their sales target. The distributor processes it because refusing an order feels like losing a customer. Without automated systems that physically prevent order processing when credit limits are breached, limits are suggestions, not controls. This is where automated order management becomes critical, the system must say no when the human will not.

Manual Tracking and Reconciliation

When outstandings are tracked in Excel sheets, paper ledgers, or disconnected accounting software, visibility into the true credit exposure is always delayed and often inaccurate. A distributor with 300 retail accounts cannot possibly maintain real-time visibility into every account's outstanding balance, aging profile, and payment pattern using manual methods. By the time a problem account is identified, the outstanding has ballooned from manageable to critical.

Relationship-Based Lending

Indian distribution runs on relationships. Distributors extend credit to retailers they know personally, often without formal documentation. When a long-standing retailer asks for extended terms, the distributor agrees because saying no feels like a betrayal of the relationship. This is human and understandable, but it is also the single biggest source of bad debt. Relationships should inform credit decisions, not override them.

Market Conditions and Seasonal Pressures

Festive seasons, new product launches, and competitive pressure create spikes in credit extension. During Diwali, distributors may extend 2-3x their normal credit to capture seasonal demand. During monsoon months, rural retailers face genuine cash flow challenges. Economic slowdowns compress retailer margins and slow payment velocity across the entire chain. Without flexible credit policies that adjust for these cycles, defaults spike during exactly the periods when distributors can least afford them.

Lack of Early Warning Systems

Most credit problems build gradually: a payment that was 3 days late becomes 7 days late, then 15, then 30. Without systematic monitoring of payment behaviour trends, these warning signs go unnoticed until the account is deeply overdue and the probability of full recovery is significantly lower.

Types of Credit in FMCG Distribution

Each credit type carries different risk profiles and requires different management approaches.

Trade Credit (Invoice Credit)

This is the most common form of credit in Indian FMCG distribution. The brand or distributor supplies goods to the retailer and allows a specified number of days (typically 7-30 days) to make payment. The credit period is often informal, with no written agreement or interest clause. Trade credit represents 70-80% of total credit exposure in most FMCG distribution networks. Managing it effectively requires robust invoice and billing systems that track every rupee from the moment goods are dispatched to the moment payment is received.

Channel Financing

Larger FMCG companies work with banks and NBFCs to provide channel financing to their distributors. The brand provides a guarantee, the financier extends a credit line, and the distributor uses that credit line to purchase inventory. This shifts credit risk to the financier but introduces complexity around utilization tracking and repayment monitoring. For brands at scale, channel financing can unlock 30-50% more distributor purchasing capacity without increasing the brand's own credit exposure.

Credit Notes

Credit notes arise from returns, damaged goods, expired products, scheme adjustments, and pricing corrections. While not credit in the traditional sense, unresolved credit notes are a major source of disputes and delayed payments. A retailer who believes they are owed Rs 15,000 in credit notes will withhold Rs 15,000 from their next payment, even if the credit note has not been officially processed. Automating credit note issuance and adjustment through your billing system eliminates this friction entirely.

Advance Payments and Deposits

Some high-risk accounts operate on advance payment or security deposit models. The retailer deposits a fixed amount (typically 15-30 days of average purchases) as security. Orders are fulfilled against this deposit. This is the safest model but the hardest to implement in competitive markets where rivals offer full credit terms.

Scheme-Linked Credit

During promotional periods, brands often extend additional credit to support scheme-based purchases. These scheme-linked extensions are frequently the source of confusion because terms are communicated verbally and tracked nowhere. A proper scheme engine integrated with credit management eliminates this category of defaults entirely.

| Credit Type | Typical Exposure | Risk Level | Management Approach |

|---|---|---|---|

| Trade credit | 70-80% of total | Medium-High | Automated limits, aging alerts, credit stops |

| Channel financing | 10-20% of total | Low-Medium | Bank-managed, brand guarantee monitoring |

| Credit notes | 5-10% of total | Low | Automated issuance, real-time adjustment |

| Advance payments | Variable | Minimal | Deposit tracking, auto-deduction |

| Scheme-linked | 5-15% during promos | Medium | Scheme engine integration, clear terms |

The Credit Management Lifecycle

Effective credit management is a continuous lifecycle with five distinct stages. Companies that treat it as an end-to-end process rather than a collection problem consistently achieve lower default rates and faster collections.

Stage 1: Assessment

Before extending credit, conduct a structured assessment: verify business existence, review financial information, check references, assess location potential, and evaluate the owner's track record. For new accounts, assessment should take 2-3 days. For existing accounts, reassess quarterly based on actual payment behaviour. Most Indian FMCG companies skip this stage entirely and then wonder why defaults are high.

Stage 2: Limit Setting

Based on the assessment, assign a credit limit that reflects the account's purchasing capacity and payment reliability. The limit should be tied to the account's average monthly purchase value and payment cycle, not to what the retailer asks for or what the salesperson wants to sell. A common formula: credit limit equals average monthly purchases multiplied by the credit period in days divided by 30, with a safety margin of 80%. So a retailer buying Rs 1 lakh per month on 15-day terms gets a credit limit of Rs 40,000 (1,00,000 x 15/30 x 0.8). This formula ensures the limit is grounded in actual business volume, not wishful thinking.

Stage 3: Monitoring

Once credit is extended, monitor it continuously. This means tracking outstanding balances in real time, generating aging reports daily, flagging accounts that are approaching or exceeding limits, and watching for behavioural changes, a retailer who was always on time and suddenly starts paying 5 days late is sending a signal. Sales analytics dashboards should surface these signals automatically, not wait for someone to run a manual report.

Stage 4: Collection

Proactive collection starts before the due date, not after. Send reminders 3 days before payment is due. Follow up on the due date. Escalate on day 3 after due. Implement credit stops on day 7 or 14 depending on the account's history. Automated reminder sequences via SMS, WhatsApp, and app notifications are 4-5x more effective than manual phone calls because they are consistent and timely.

Stage 5: Recovery

For accounts 30+ days overdue, shift from collection to recovery mode: formal demand notices, field visits by senior management, negotiated repayment plans, and in extreme cases, legal action. An account that required recovery should have its credit limit permanently reduced. Document every recovery action to build institutional memory that prevents repeat defaults.

Software automates each stage of this lifecycle. SpireStock's distributor management solution handles credit assessment workflows, limit configuration, real-time monitoring, automated collection sequences, and recovery tracking in a single integrated platform. The result is not just fewer defaults but a fundamentally different relationship between the company and its channel, one where credit discipline is built into the operating rhythm rather than imposed as an afterthought.

Building a Credit Scoring Model for Distributors

The most sophisticated FMCG companies in India are now applying internal credit scoring models to their distributor and retailer networks. This is not as complex as bank-level credit scoring. It is a practical, data-driven framework that uses information you already have to make better credit decisions.

Input Parameters

A robust distributor credit score draws on five categories of data:

- Payment history (40% weight) -- The single most predictive factor. How often does the account pay on time? What is the average delay in days? Has the delay trend been improving or worsening over the last 6 months? Accounts with 90%+ on-time payment rate score highest. Those below 60% are flagged for review.

- Order consistency (20% weight) -- Regular, predictable ordering patterns indicate a stable business. Erratic ordering, sudden spikes followed by drops, or long gaps between orders suggest underlying instability. Track order frequency, average order value, and month-over-month consistency.

- Territory performance (15% weight) -- The economic health of the territory affects all accounts in it. A retailer in a thriving commercial area of Bangalore carries different risk than one in a struggling market town. Territory-level default rates, growth trends, and competitive intensity all feed into this component.

- Years in business (15% weight) -- Longevity is a proxy for stability. A retailer who has operated for 10+ years has weathered multiple economic cycles and is less likely to default than a new entrant. However, this factor should be combined with recent payment behaviour, not used in isolation, because even long-standing businesses can deteriorate.

- Financial indicators (10% weight) -- Where available, incorporate data on the account's other liabilities, inventory levels, and cash flow patterns. In practice, this data is hard to obtain for small retailers, which is why it carries the lowest weight. For large distributors, financial statements and bank references provide valuable input.

Score Calculation and Limit Assignment

Combine the weighted inputs to produce a score on a 0-100 scale. Map the score to credit tiers:

| Credit Score | Tier | Credit Limit | Payment Terms | Monitoring |

|---|---|---|---|---|

| 85-100 | Platinum | Up to 120% of avg monthly purchase | 21-30 days | Monthly review |

| 70-84 | Gold | Up to 100% of avg monthly purchase | 15-21 days | Fortnightly review |

| 55-69 | Silver | Up to 70% of avg monthly purchase | 7-15 days | Weekly review |

| 40-54 | Bronze | Up to 40% of avg monthly purchase | 7 days | Daily monitoring |

| Below 40 | Cash Only | No credit | Advance payment | N/A |

Dynamic Scoring

Credit scores should not be static. Recalculate monthly based on the latest 6-month rolling data. Accounts that improve payment discipline see scores rise and credit limits increase automatically. Those showing deterioration see limits tighten before a default occurs. This dynamic approach creates a positive incentive loop: retailers who pay well get rewarded with better terms.

Implementing credit scoring does not require a data science team. The inputs are transactional data already in your order management and billing system. SpireStock computes scores automatically, applies them to credit limits, and surfaces the results in a dashboard your finance and sales teams can act on.

Automated Credit Controls That Actually Work

The difference between companies with 3% default rates and companies with 0.5% default rates almost always comes down to automated controls. Manual credit management depends on individual vigilance, which is inherently inconsistent. Automated controls are tireless, consistent, and emotionally neutral, qualities that are essential when money is involved.

Auto Credit Stop

When a distributor or retailer's outstanding exceeds their credit limit, the system should automatically block new order processing. No override by the salesperson. No exception because the month-end target is at risk. This is the single most impactful credit control, and most Indian FMCG companies resist it because it feels like it will hurt sales. The data tells a different story: companies that implement auto credit stops see a temporary 3-5% dip in orders during the first month, followed by permanent improvement in collection velocity that more than compensates within 60 days.

Aging Alerts and Escalation Workflows

Configure aging-based alerts that trigger automatically as accounts move through overdue buckets:

- Day 1-3 overdue: Automated SMS and WhatsApp reminder to the retailer with outstanding amount and payment link

- Day 4-7 overdue: Alert to the assigned salesperson with instruction to follow up during next visit

- Day 8-14 overdue: Escalation to area sales manager with account details and overdue history

- Day 15-21 overdue: Auto credit stop triggered, formal overdue notice sent, regional manager notified

- Day 22-30 overdue: Escalation to branch head or finance controller, account flagged for recovery

- Day 30+ overdue: Account moved to recovery team, credit limit suspended, legal notice template generated

Each escalation step is logged with timestamps, creating a complete audit trail that protects both parties in disputes and creates accountability at every level.

Payment Reminder Automation

Automated reminders are about sending the right message at the right time through the right channel. Three days before the due date, send a friendly reminder with the amount and UPI payment link. On the due date, send a payment-due notification. Three days after, send an overdue alert with a clear consequence statement. The consistency is what makes them effective: a distributor who receives a reminder at 9 AM every time their payment approaches due date internalizes the rhythm within a few cycles.

SpireStock Credit Control Implementation

SpireStock implements these controls as configurable workflows rather than rigid rules. Each brand defines its own credit policies, escalation timelines, and override authorities. The analytics dashboard provides real-time visibility into credit utilization across the entire network, with drill-down from national summary to individual account. Credit limits integrate directly with order processing, so enforcement is automatic, not dependent on someone checking a spreadsheet.

Override Management

No credit control system should be completely rigid. There are legitimate reasons to override a credit stop: a key account during a critical promotion, a seasonal spike for a reliable distributor, or a one-time large order from a strong retailer. The key is to make overrides deliberate, traceable, and limited. SpireStock allows designated authority levels to approve temporary overrides with mandatory reason codes, time limits, and automatic expiry. Every override is logged so patterns of excessive overriding can be identified.

Collection Optimization Strategies

Credit controls prevent new defaults. Collection strategies recover existing outstandings and establish the payment discipline that keeps defaults low over time. The most effective FMCG companies in India treat collection as a distinct operational capability, not an extension of sales.

Payment Collection Routes

Just as you plan delivery routes, plan collection routes to maximize payment recovery per trip. Map overdue accounts geographically, prioritize by amount and aging, and assign collection visits on optimized routes. A dedicated collection person covering 15-20 accounts per day will collect 3x more than a salesperson making ad-hoc calls between visits. Use distribution tracking to monitor collection route compliance.

UPI Adoption and Digital Payments

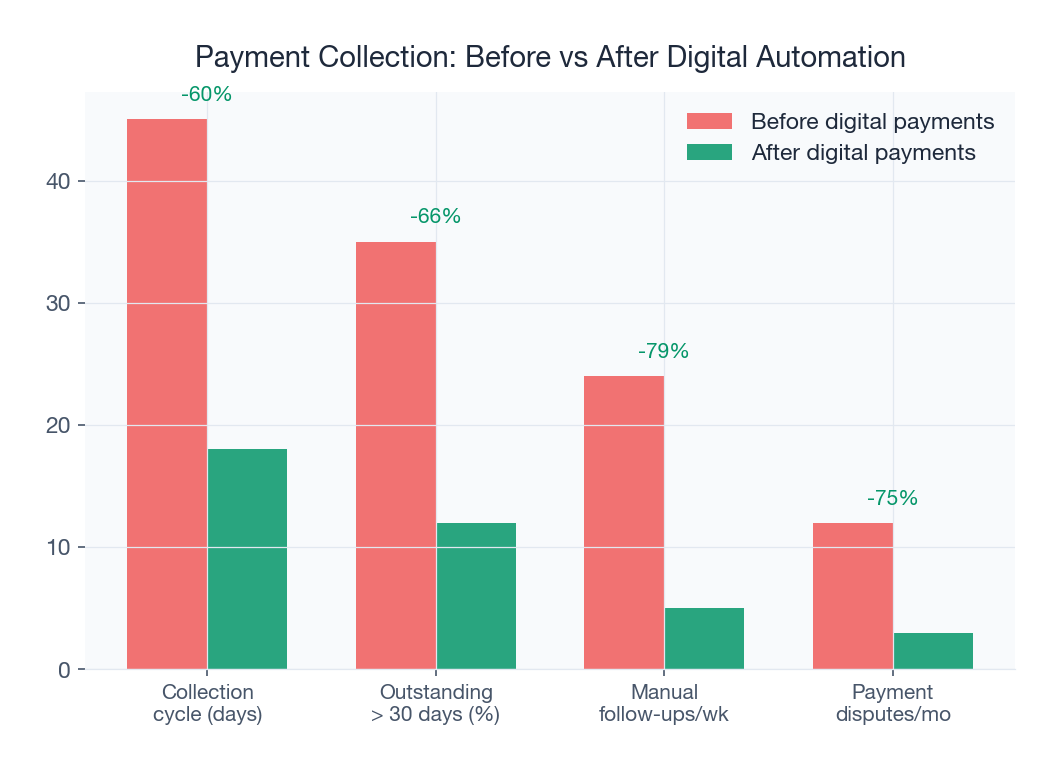

India's UPI infrastructure has transformed payment collection. Instead of waiting for cheques to clear or cash to be counted, distributors share a UPI payment link directly from the invoice and receive instant confirmation. Retailers who pay via UPI clear invoices 4-6 days faster than those using cheque or cash. Make UPI the default payment option in every invoice and reminder generated through your billing system.

Partial Payment Tracking

In Indian FMCG distribution, partial payments are the norm. A retailer owing Rs 50,000 will pay Rs 30,000 now and promise the rest next week. Without a system tracking partial payments against specific invoices, reconciliation becomes a nightmare. SpireStock's payment module automatically allocates partial payments using configurable rules (oldest first, largest first, or manual allocation), maintaining accurate aging and credit positions at all times.

Collection Incentives

Positive incentives accelerate collection more sustainably than punitive measures:

- Early payment discounts: Offer 0.5-1% discount for payment within 7 days against standard 15-day terms. On Rs 1 lakh monthly purchases, this costs Rs 500-1,000 but saves Rs 1,500-2,000 in financing costs.

- Prompt payment rewards: Retailers maintaining 90%+ on-time payment for 6 months earn additional scheme benefits or priority allocation during shortages.

- Collection staff incentives: Tie field staff compensation to collection metrics: percentage of overdue collected, accounts brought current, and reduction in total outstanding.

- Distributor collection bonuses: Offer quarterly bonuses tied to DSO performance. A distributor maintaining DSO under 12 days earns an additional 0.25% margin.

Seasonal Collection Planning

Credit defaults spike post-Diwali (retailers overstocked), during monsoon months (rural demand drops), and in Q4 (year-end cash crunches). Tighten credit terms 30 days before historically high-default periods and schedule intensive collection drives during recovery periods. Data from 2-3 years of sales analytics will reveal your network's specific seasonal patterns.

Case Studies: Reducing Credit Defaults in Practice

Theory is valuable, but Indian FMCG operators want to see what works in practice. The following three case studies represent real-world transformations achieved through systematic credit management.

Case Study 1: Dairy Brand Reduces DSO from 25 to 12 Days

A Rs 320-crore dairy brand operating across Pune, Kolhapur, and Satara with 180 distributors and 4,200 retail accounts had an average DSO of 25 days. Bad debt write-offs were running at 1.8% of revenue (Rs 57 lakh annually), and salespeople routinely accepted orders from over-limit accounts to meet targets.

After implementing SpireStock's credit management module, the brand scored every retail account on 12 months of payment history (moving 15% to cash-only terms), activated automated credit stops with no salesperson override, configured SMS and WhatsApp reminders at day -3, 0, +3, and +7 with UPI payment links, and planned dedicated collection visits for the top 50 overdue accounts weekly.

Results after 6 months: DSO dropped from 25 to 12 days. Bad debt fell from 1.8% to 0.3%. Reconciliation time dropped from 60 to 8 hours per month. Working capital released: Rs 7.1 crore. Net revenue increased 4% as freed capital funded expansion into 35 new retail accounts.

Case Study 2: FMCG Company Cuts Defaults by 70%

A packaged foods company distributing through 420 distributors across Maharashtra, Gujarat, and Rajasthan had a 2.4% default rate, well above the 1.5% industry average. Analysis revealed 80% of defaults came from just 12% of accounts, chronic late payers never systematically addressed because they contributed meaningful volume.

The company implemented a phased transformation: data cleanup and credit scoring for all 8,400 retail accounts (which alone revealed Rs 34 lakh in unidentified overdue amounts), tiered credit limits with automated escalation workflows, and finally auto credit stops with UPI payment links on all invoices. Chronic defaulters received a 60-day improvement window; 38 accounts that failed were moved to advance payment terms.

Results after 6 months: default rate dropped from 2.4% to 0.7% (70% reduction). Annual bad debt savings: Rs 85 lakh. DSO improved from 22 to 14 days. The savings funded a new product launch generating Rs 4.2 crore in incremental first-year revenue.

Case Study 3: Beverage Distributor Improves Working Capital

A regional beverage distributor in Ahmedabad with Rs 8 crore annual turnover and 650 retail accounts was borrowing Rs 45 lakh at 11.5% APR to fund the gap between paying the brand (15-day terms) and collecting from retailers (28-day average).

After implementing systematic credit management, average collection dropped from 28 to 14 days, eliminating the funding gap. Working capital borrowing fell from Rs 45 lakh to Rs 12 lakh, saving Rs 3.8 lakh annually in interest. Bad debt fell from Rs 4.2 lakh to Rs 1.1 lakh. The freed capital funded expansion into 120 new retail accounts, and overall profitability improved by 1.8 percentage points.

The distributor credits two changes: auto credit stops that prevented over-limit orders and UPI payment links that made it easy to pay instantly. The combination of friction removal and consequence introduction created a virtuous cycle within 90 days.

Impact on Working Capital

Every rupee locked in overdue receivables is a rupee that cannot fund inventory, market expansion, or operational improvement. In FMCG distribution, receivables typically represent 40-60% of current assets. Reducing receivables by even 5 days of sales has an outsized impact on working capital availability.

Quantifying the Impact

Consider these scenarios for a Rs 100-crore annual turnover FMCG company:

| DSO Reduction | Working Capital Released | Interest Saved (at 10% APR) | Equivalent Margin Improvement |

|---|---|---|---|

| 5 days | Rs 1.37 crore | Rs 13.7 lakh/year | 0.14% |

| 10 days | Rs 2.74 crore | Rs 27.4 lakh/year | 0.27% |

| 15 days | Rs 4.11 crore | Rs 41.1 lakh/year | 0.41% |

| 20 days | Rs 5.48 crore | Rs 54.8 lakh/year | 0.55% |

For a Rs 100-crore business, a 15-day DSO reduction releases Rs 4.11 crore in working capital and saves Rs 41.1 lakh annually in interest, equivalent to generating Rs 8 crore in additional revenue at 5% net margin. Few operational improvements deliver this kind of leverage.

ROI Calculation for Credit Management Software

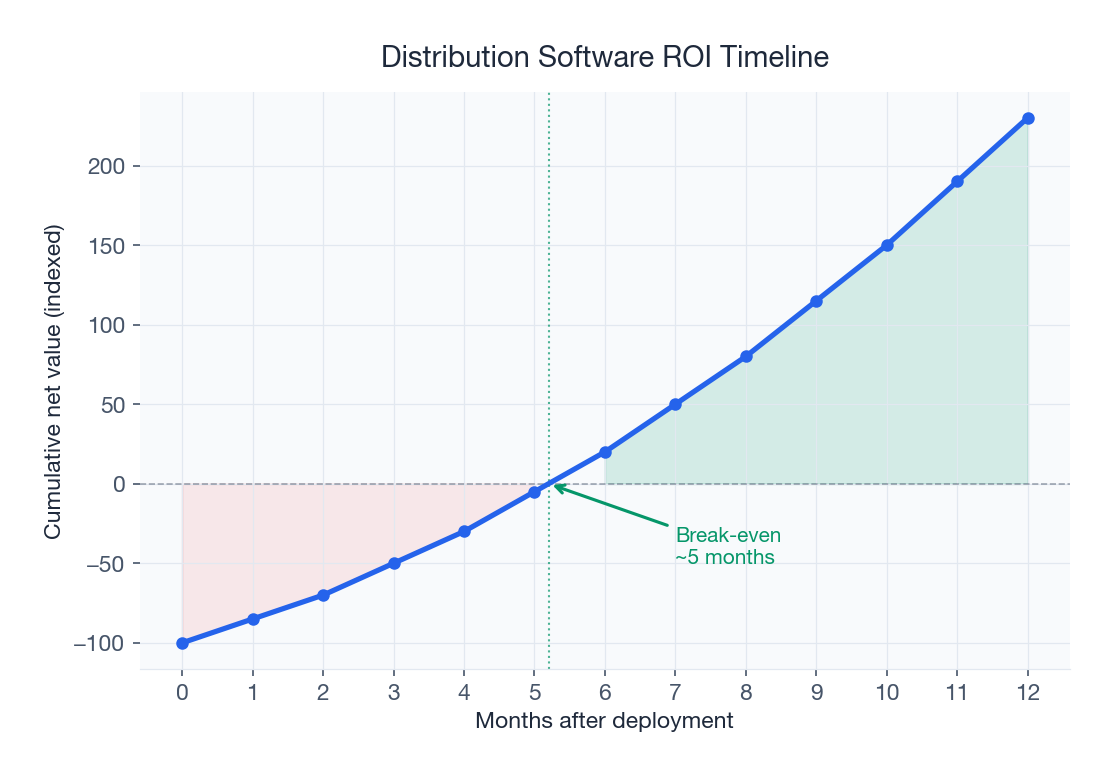

A conservative ROI model for a 200-400 distributor network: software cost of Rs 10-18 lakh/year plus Rs 2-4 lakh implementation, against benefits of Rs 2-5 crore in released working capital, Rs 20-50 lakh/year in interest savings, Rs 15-40 lakh/year in reduced bad debt, and Rs 6-12 lakh/year in staff time savings. Total annual benefit: Rs 41 lakh to Rs 1.02 crore. ROI: 300-600%. Payback period: 6-12 weeks. Even the most conservative assumptions show payback within a single quarter. Check SpireStock pricing for exact numbers for your network size.

Beyond Financial Returns

The non-financial benefits are equally significant: transparent credit policies eliminate favouritism that breeds resentment, payment behaviour serves as an early indicator of territory health (deteriorating patterns signal demand issues before they appear in sales data), automated credit management frees senior management to focus on growth, and companies with tight credit discipline can offer better terms to good distributors while competitors apply blanket policies that penalize everyone.

Technology Solutions for Credit Management

The right technology stack transforms credit management from a manual, reactive process into an automated, proactive one. Here is what to look for in a distribution management system's credit module.

DMS Credit Modules

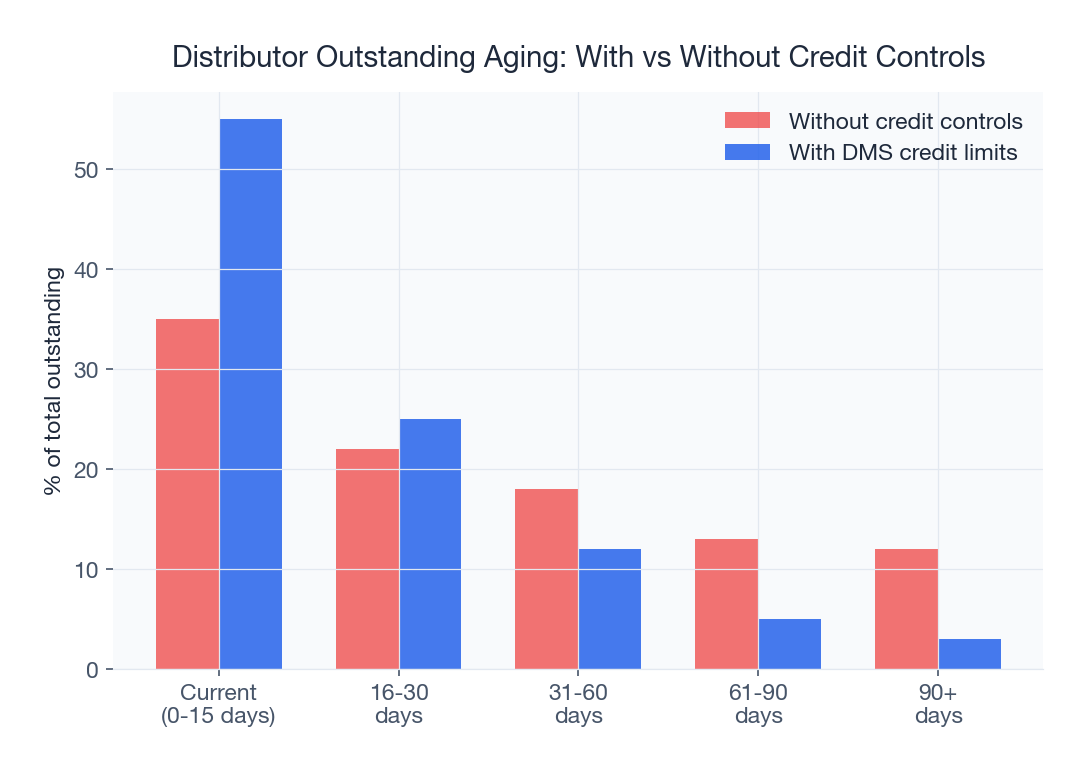

A modern distribution management system should include integrated credit management as a core module, not an add-on. Key capabilities: credit limit configuration per account, territory, or tier with approval workflows; real-time outstanding tracking with aging breakdown; automated order blocking when limits are exceeded with configurable override authorities; payment recording by any mode (UPI, cash, cheque, NEFT) with automatic invoice allocation; aging analysis across current, 1-15, 16-30, 31-60, and 60+ day buckets; and automated credit scoring with dynamic limit adjustment.

Integration with Accounting Software

Every payment recorded in the field should automatically reflect in Tally, Busy, SAP, or whatever accounting platform your finance team uses. This eliminates the double-entry problem: operations records payments in the DMS, finance records the same in Tally, and the two rarely match. SpireStock provides API-based integration with all major Indian accounting platforms, ensuring single-source-of-truth data.

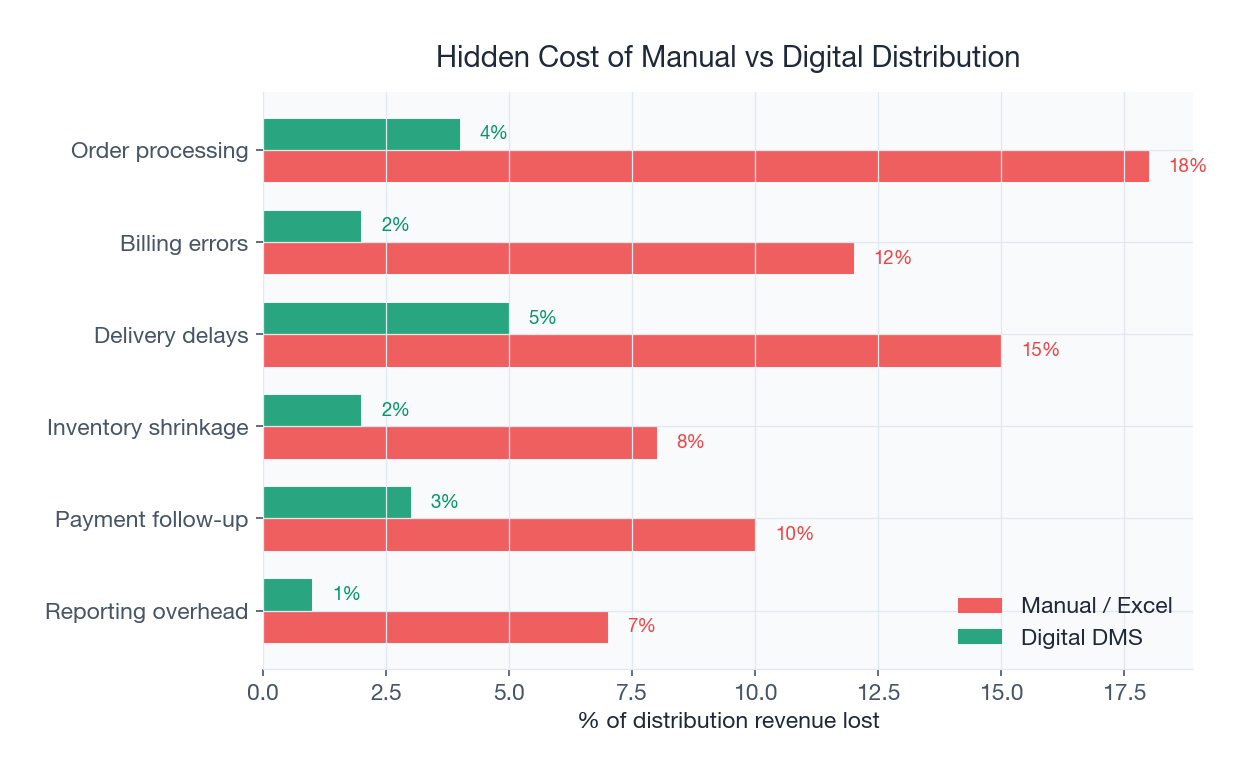

Automated Reconciliation

When both parties work from the same digital platform, reconciliation shifts from a monthly exercise to a continuous, automated process. Discrepancies are flagged in real time rather than discovered 30 days later. For companies managing 200+ distributors, this alone saves 100-200 hours of accounting effort per month.

Mobile-First Collection

Your field staff are on the road, not at a desk. The SpireStock mobile app lets field staff view outstanding balances, record payments, generate receipts, share payment links, and log collection notes from their smartphone. Offline capability ensures these functions work even with poor connectivity, syncing automatically when the network is available.

Reporting and Dashboards

Effective credit management requires the right reports at the right frequency: daily overdue and breach alerts, weekly aging trends and collection efficiency by territory, monthly DSO trends and working capital impact, and quarterly credit score recalibration with policy effectiveness review. SpireStock's analytics engine generates all of these automatically, pushing the right information to the right people at scheduled intervals.

Implementation Roadmap

Implementing credit management across an FMCG distribution network is a change management exercise as much as a technology deployment. A proven 12-week roadmap:

- Weeks 1-3 (Foundation): Migrate ledgers to SpireStock, clean up historical data, define credit policies (limit methodology, payment terms by tier, escalation timelines, override authorities), and configure the system

- Weeks 4-6 (Soft Launch): Activate monitoring without hard enforcement, run credit scoring for validation, train teams, and communicate policy changes to distributors

- Weeks 7-9 (Enforcement): Activate auto credit stops, turn on automated reminders, begin planned collection routes, and hold weekly credit review meetings

- Weeks 10-12 (Optimization): Analyze data, fine-tune credit scores, address edge cases, and validate ROI projections

Most companies see measurable improvement by week 6 and full ROI by week 12. The key success factor is executive commitment: the finance head or MD must personally champion the initiative and resist pressure to relax enforcement during the adjustment period.

Getting Started

Reducing credit defaults in FMCG distribution is not about finding a silver bullet. It is about implementing a systematic approach that addresses every stage of the credit lifecycle: assessment, limit setting, monitoring, collection, and recovery. The technology to do this exists today and pays for itself within a single quarter. The only question is whether your organization has the discipline to implement it consistently.

The math is clear: for every Rs 100 crore in annual distribution revenue, systematic credit management unlocks Rs 2-5 crore in working capital, saves Rs 20-50 lakh in interest costs, and prevents Rs 15-40 lakh in bad debt. Companies that build this discipline now will emerge with stronger balance sheets and the working capital to fund growth. Those that continue with manual, relationship-driven credit management will face escalating defaults and declining competitiveness.

Start by understanding your current credit exposure. Pull your aging report. Calculate your DSO. Identify your chronic defaulters. Then talk to our team about building a credit management framework that fits your specific distribution model. Or review our payment collection solution and distributor management platform to see how other Indian FMCG companies have solved this problem. Read our related guides on payment collection for dairy distributors and distribution management software in India for additional perspective. If you are ready to move forward, check our pricing or book a demo to see the credit management dashboard working against real distributor data.

Sources & References

Frequently Asked Questions

An estimated Rs 60,000 crore or more is locked in distributor-to-retailer credit across the Indian FMCG distribution network at any point. This represents the single largest working capital drain in the consumer goods supply chain, affecting brands, distributors, and retailers alike.

Automated credit limit enforcement (auto credit stop) is the single most impactful control. When the system automatically blocks new orders for accounts exceeding their credit limit, collection velocity improves within 60 days. Combine this with credit scoring, automated reminders, and UPI payment links for maximum impact.

Credit scoring uses five weighted parameters: payment history (40%), order consistency (20%), territory performance (15%), years in business (15%), and financial indicators (10%). The resulting score on a 0-100 scale determines the credit tier (Platinum/Gold/Silver/Bronze/Cash Only), which drives automatic credit limit and payment term assignment.

Most Indian FMCG companies see 300-600% ROI from credit management software, with payback within 6-12 weeks. Benefits include Rs 2-5 crore in released working capital per Rs 100 crore turnover, Rs 20-50 lakh in annual interest savings, and Rs 15-40 lakh in reduced bad debt.

A typical implementation follows a 12-week roadmap: weeks 1-3 for data migration and policy configuration, weeks 4-6 for soft launch with monitoring, weeks 7-9 for enforcement activation, and weeks 10-12 for optimization. Most companies see measurable improvement by week 6 and full ROI by week 12.

Yes. Data shows a temporary 3-5% dip in orders during the first month of auto credit stop implementation, followed by a permanent improvement in collection velocity that more than compensates within 60 days. Net revenue typically increases as freed working capital funds expansion into new accounts.

UPI payment links attached to invoices and reminders allow retailers to pay instantly from their smartphones. Retailers who pay via UPI clear invoices 4-6 days faster than those using cheque or cash. The elimination of banking friction is the single biggest accelerator of collection velocity in Indian FMCG distribution.

Industry average DSO in Indian FMCG distribution is 18-25 days. Well-managed networks with automated credit controls achieve 10-14 days. The best-in-class operations run at 7-10 days. Every day of DSO reduction releases approximately Rs 2.74 lakh in working capital per Rs 100 crore in annual turnover.

Related SpireStock Features

GST-compliant invoicing with HSN codes, gate passes, and financial ledger.

Powerful dashboards with sales trends, MIS reports, and distribution analytics.

End-to-end order lifecycle from placement to delivery with multi-level approval workflows.

Related Industries

Streamline FMCG distribution with order management, beat planning, retailer tracking, and GST billing. Built for Indian FMCG supply chains.

End-to-end dairy distribution software for milk, curd, paneer, and ghee brands. Manage orders, crates, cold chain, and GST billing in one platform.

Related Solutions

Track distributor and retailer payments. Cash, UPI, cheque collection with reconciliation, ageing reports, and credit limit management.

Manage your entire distributor network digitally. Onboarding, credit limits, outstanding tracking, and performance analytics. Start free trial.

Related Entities

Ready to Streamline Your Distribution?

Start your free 30-day trial and see how SpireStock can transform your dairy, FMCG or consumer-goods distribution operation, from order capture to crate recovery.

SpireStock Team

Product & Industry Insights

SpireStock Team leads product at SpireStock, where the team ships distribution management software for India's dairy, FMCG and consumer-goods brands.